International

Telecommunication

Union

Place des Nations

CH-1211 Geneva 20

Switzerland

Published in Switzerland

Geneva, 2020

Photo credits: Shutterstock

ITUPublications

Measuring digital

development

ICT Price Trends

2019

ISBN: 978-92-61-30901-5

9 7 8 9 2 6 1 3 0 9 0 1 5

Measuring Digital

Development

ICT Price Trends

2019

Acknowledgements

This publication was prepared by the ICT Data and Analytics Division (IDA) within the Digital

Knowledge Hub Department (DKH) of the Telecommunication Development Bureau of the

International Telecommunication Union (ITU). The main author was Martin Schaaper, with substantial

input from Philippa Biggs. The data were prepared by Daniela Pokorna. Helpful comments were

received from Susan Teltscher and Daniel Vertesy.

The report was edited by Tim Eldridge. Desktop publishing and cover design was carried by the ITU

Publication Production Service (PUBL).

ISBN:

978-92-61-30891-9 (Paper version)

978-92-61-30901-5 (Electronic version)

978-92-61-30911-4 (EPUB version)

978-92-61-30921-3 (Mobi version)

© ITU 2020

International Telecommunication Union

Place des Nations

CH-1211 Geneva, Switzerland

Some rights reserved. This work is licensed to the public through a Creative Commons Attribution-Non-

Commercial-Share Alike 3.0 IGO license (CC BY-NC-SA 3.0 IGO).

Under the terms of this licence, you may copy, redistribute and adapt the work for non-commercial purposes,

provided the work is appropriately cited. In any use of this work, there should be no suggestion that ITU

endorse any specific organization, products or services. The unauthorized use of the ITU names or logos is

not permitted. If you adapt the work, then you must license your work under the same or equivalent Creative

Commons licence. If you create a translation of this work, you should add the following disclaimer along with

the suggested citation: “This translation was not created by the International Telecommunication Union (ITU).

ITU is not responsible for the content or accuracy of this translation. The original English edition shall be the

binding and authentic edition”. For more information,

please visit https://creativecommons.org/licenses/by-nc-sa/3.0/igo/

Foreword

I am pleased to present the new edition of ICT Price Trends, the second report in ITU’s new

Measuring Digital Development series of statistical and analytical publications, which replaces the

annual Measuring the Information Society Report.

ICT Price Trends 2019 monitors the affordability of ICT services by analysing and comparing price

data for mobile-voice services, mobile data and fixed broadband. Following a revision of the ICT

price benchmark methodology in 2017, this is the first time we are reporting on ITU’s revised price

baskets and, in particular, the first time we are sharing results for the combined data-and-voice

baskets introduced after the 2017 revision. These new results shed important light on the effect of

the bundling of services on consumer prices.

This publication also reports on the affordability gap between developed and developing countries

– that is, the difference in prices when these are held up against countries’ gross national income

(GNI) levels. It also provides information on countries’ progress towards achieving the United

Nations Broadband Commission for Sustainable Development target for 2025, according to which

entry-level broadband services should be made affordable in developing countries at a level

corresponding to less than 2 per cent of monthly GNI per capita.

Overall, while this report reveals that average prices are broadly continuing to fall, it confirms that

broadband services can still be too expensive for the poorest consumers, especially in countries with

a low GNI per capita.

The COVID-19 global health emergency has made us all acutely aware of the vital importance

of broadband networks to social and economic prosperity and global development. I hope this

authoritative report serves as a crucial pillar of renewed efforts to urgently make digital services more

available, and more affordable, to all people of the world.

Doreen Bogdan-Martin

Director, Telecommunication Development Bureau (BDT)

International Telecommunication Union

iii

Measuring Digital Development: ICT Price Trends 2019

Acknowledgements ............................................................................................................................................ ii

Foreword ............................................................................................................................................................. iii

List of boxes, charts, figures and tables .......................................................................................................... vi

Executive summary .............................................................................................................................................1

New benchmarks for a changing market .........................................................................................................4

About this publication..................................................................................................................................5

Mobile-data-and-voice baskets ......................................................................................................................... 6

Global trends .................................................................................................................................................6

Benchmarking countries ..............................................................................................................................9

Mobile-voice basket ..........................................................................................................................................19

Global trends ...............................................................................................................................................19

Benchmarking countries ............................................................................................................................27

Mobile-data basket ...........................................................................................................................................32

Global trends ...............................................................................................................................................32

Benchmarking countries ............................................................................................................................41

Fixed-broadband basket ..................................................................................................................................53

Global trends ...............................................................................................................................................53

Benchmarking countries ............................................................................................................................60

Conclusion..........................................................................................................................................................72

Annex 1: ICT price data methodology ...........................................................................................................75

ICT price baskets ........................................................................................................................................75

The mobile-cellular low-usage basket .....................................................................................................76

The fixed-broadband basket ....................................................................................................................79

The data-only mobile-broadband price basket .....................................................................................81

The data-and-voice price baskets ............................................................................................................83

Price-data collection and sources ............................................................................................................86

Annex 2: Detailed ICT price tables, 2019 ......................................................................................................89

Annex 3: ICT price basket country tables 2018 ......................................................................................... 141

v

Measuring Digital Development: ICT Price Trends 2019

Table of contents

List of boxes, charts, figures and tables

Charts

Chart 1: Mobile-data-and-voice baskets in USD, 2019 ........................................................................7

Chart 2: Mobile-data-and-voice basket in PPP$, 2019 .........................................................................8

Chart 3: Mobile-data-and-voice basket as a % of GNI p.c., 2019 .......................................................9

Chart 4: Global mobile-voice price basket in USD (left axis) and mobile-voice subscriptions

per 100 inhabitants (right axis), 2008-2019 ...............................................................................19

Chart 5: Mobile-voice basket in USD, 2019 .........................................................................................20

Chart 6: Global mobile-voice price basket in PPP$ (left axis) and mobile-voice subscriptions

per 100 inhabitants (right axis), 2008-2019 ...............................................................................21

Chart 7: Mobile-voice basket in PPP$, 2019 ........................................................................................22

Chart 8: Global mobile-voice price basket as a % of GNI p.c. (left axis) and mobile-voice

subscriptions per 100 inhabitants (right axis), 2008-2019 ......................................................23

Chart 9: Mobile-voice basket as a % of GNI p.c., 2019 ......................................................................24

Chart 10: Global mobile-voice price basket as a % of GNI p.c. by development level (left

axis) and affordability gap for mobile-voice (right axis), 2008-2019......................................25

Chart 11: Mobile-voice subscriptions per 100 inhabitants, 2008-2019* .........................................26

Chart 12: Global mobile-data price basket in USD (left axis) and active mobile-data

subscriptions per 100 inhabitants (right axis), 2013-2019 ......................................................32

Chart 13: Mobile-data basket in USD, 2019 ........................................................................................33

Chart 14: Global mobile-data price basket in PPP$ (left axis) and active mobile-data

subscriptions per 100 inhabitants (right axis), 2013-2019 ......................................................34

Chart 15: Mobile-data basket in PPP$, 2019 .......................................................................................35

Chart 16: Global mobile-data price basket as a % of GNI p.c. (left axis) and active mobile-

data subscriptions per 100 inhabitants (right axis), 2013-2019 .............................................. 36

Chart 17: Mobile-data basket as a % of GNI p.c., 2019 ...................................................................... 37

Chart 18: Mobile-cellular subscriptions, active mobile-broadband subscriptions and Internet

users, by level of development, 2019* .......................................................................................38

Chart 19: Global mobile-data price basket in terms of GNI p.c. by development level (left

axis) and affordability gap for mobile-data (right axis), 2008-2019 .......................................39

Chart 20: Active mobile-data subscriptions per 100 inhabitants, 2008-2019* ............................... 40

Chart 21: Number of countries having achieved the Broadband Commission target with

mobile-data services, 2019 ..........................................................................................................46

Chart 22: Mobile-data prices as a percentage of GNI p.c. and monthly data allowance,

Africa, 2019 ..................................................................................................................................... 47

Chart 23: Mobile-data prices as a percentage of GNI p.c. and monthly data allowance, Arab

States, 2019 ....................................................................................................................................48

Chart 24: Mobile-data prices as a percentage of GNI p.c. and monthly data allowance, Asia

and the Pacific, 2019 .....................................................................................................................49

vi

Measuring Digital Development: ICT Price Trends 2019

Chart 25: Mobile-data prices as a percentage of GNI p.c. and monthly data allowance, CIS,

2019 ................................................................................................................................................. 50

Chart 26: Mobile-data prices as a percentage of GNI p.c. and monthly data allowance,

Europe, 2019 .................................................................................................................................. 51

Chart 27: Mobile-data prices as a percentage of GNI p.c. and monthly data allowance, the

Americas, 2019 .............................................................................................................................. 52

Chart 28: Global fixed-broadband price basket in USD (left axis) and fixed-broadband

subscriptions per 100 inhabitants (right axis), 2008-2019 ...................................................... 53

Chart 29: Fixed-broadband basket in USD, 2019 ............................................................................... 54

Chart 30: Global fixed-broadband price basket in PPP$ (left axis) and fixed-broadband

subscriptions per 100 inhabitants (right axis), 2008-2019 ...................................................... 55

Chart 31: Fixed-broadband basket in PPP$, 2019 .............................................................................. 56

Chart 32: Global fixed-broadband price basket as a % of GNI p.c. (left axis) and fixed-

broadband subscriptions per 100 inhabitants (right axis), 2008-2019 ................................. 57

Chart 33: Fixed-broadband basket as a % of GNI p.c., 2019 ............................................................ 58

Chart 34: Global fixed-broadband price basket as a % of GNI p.c. by development level (left

axis) and affordability gap for fixed-broadband (right axis), 2008-2019 ............................... 59

Chart 35: Fixed-broadband subscriptions per 100 inhabitants, 2008-2019* ................................. 59

Chart 36: Entry-level fixed-broadband median speeds, 2019 ......................................................... 60

Chart 37: Number of countries having achieved the Broadband Commission target with

fixed-broadband services, 2019 .................................................................................................. 65

Chart 38: Fixed-broadband prices as a percentage of GNI p.c., speeds and caps, Africa,

2019 ................................................................................................................................................. 66

Chart 39: Fixed-broadband prices as a percentage of GNI p.c., speeds and caps, Arab

States, 2019 .................................................................................................................................... 67

Chart 40: Fixed-broadband prices as a percentage of GNI p.c., speeds and caps, Asia and

the Pacific, 2019 ............................................................................................................................. 68

Chart 41: Fixed-broadband prices as a percentage of GNI p.c., speeds and caps, CIS, 2019 .... 69

Chart 42: Fixed-broadband prices as a percentage of GNI p.c., speeds and caps, Europe,

2019 ................................................................................................................................................. 70

Chart 43: Fixed-broadband prices as a percentage of GNI p.c., speeds and caps, the

Americas, 2019 .............................................................................................................................. 71

Figures

Figure 1: New ITU ICT price baskets (from 2018) ................................................................................. 5

Annex Figure 1: New ICT price baskets (from 2018) .......................................................................... 75

Annex Figure 2: ICT price baskets up to 2017.....................................................................................75

vii

Measuring Digital Development: ICT Price Trends 2019

Tables

Table 1: Global average prices for the five baskets, 2019 ...................................................................2

Table 2: High-consumption mobile-data-and-voice basket, 2019 ...................................................10

Table 3: Low-consumption mobile-data-and-voice basket, 2019 ....................................................15

Table 4: Mobile-voice basket, 2019 ......................................................................................................27

Table 5: Mobile-data basket, 2019 ........................................................................................................41

Table 6: Fixed-broadband basket, 2019 ..............................................................................................61

Annex Table 1.1: Revised mobile-cellular low-usage basket, call and SMS distribution ..............77

Annex Table 2.1: High-consumption mobile-data-and-voice basket – plan details, 2019 ...........90

Annex Table 2.2: High-consumption mobile-data-and-voice basket – call and SMS rate,

2019 .................................................................................................................................................95

Annex Table 2.3: Low-consumption mobile-data-and-voice basket – plan details, 2019 .......... 100

Annex Table 2.4: Low-consumption mobile-data-and-voice basket – call and SMS rate, 2019

....................................................................................................................................................... 105

Annex Table 2.5: Mobile-voice basket – on-net and off-net, 2019 ................................................ 110

Annex Table 2.6: Mobile-voice basket – to fixed and SMS, 2019 .................................................. 115

Annex Table 2.7: Mobile-data basket, 2019 ..................................................................................... 120

Annex Table 2.8: Fixed-broadband basket, 2019 ............................................................................ 125

Annex Table 3.1: High-consumption mobile-data-and-voice basket, 2018 ................................ 142

Annex Table 3.2: Low-consumption mobile-data-and-voice basket, 2018 .................................. 147

Annex Table 3.3: Mobile-voice basket, 2018 .................................................................................... 152

Annex Table 3.4: Mobile-data basket, 2018 ..................................................................................... 157

Annex Table 3.5: Fixed-broadband basket, 2018 ............................................................................ 162

viii

Measuring Digital Development: ICT Price Trends 2019

Measuring Digital Development: ICT Price Trends 2019

1

Executive summary

• To accurately track and compare prices in

statistical terms internationally and over

time is no straightforward exercise. Price

comparisons can be difficult, depending on

whether they are conducted within a country,

over time, or internationally (when exchange

rates and purchasing power parity (PPP)

can complicate matters). Market trends can

also complicate the exercise – for example

network convergence, the growing number

of operators, intensifying competition

(especially in mobile) and bundling.

• The International Telecommunication Union

(ITU), its partners and stakeholders devote

considerable time and effort to developing

and refining price methodologies, in

particular through the Expert Group on

Telecommunication/ICT Indicators (EGTI).

ITU maintains a set of different price

baskets to reflect different usage patterns

and behaviour. In 2017, ITU updated and

adjusted its price baskets to reflect current

developments in the fixed and mobile

broadband markets. The price baskets

cover three different technologies: mobile-

voice, mobile-data and fixed-broadband.

In addition, the 2017 revision introduced

combined data-and-voice baskets, as a first

attempt to monitor the prices of bundled

services, which is now a very common

commercial practice.

Mobile-voice, mobile-data and fixed-

broadband baskets

• Table 1 provides an overview of average

prices for the five price baskets: mobile-data-

and-voice (low usage), mobile-data-and-

voice (high usage), mobile-voice, mobile-

data and fixed-broadband. It shows the

impact of bundling on prices, as a combined

data-and-voice basket is less expensive

than the sum of the two separate baskets.

Fixed-broadband packages were generally

more expensive on average than mobile-

data packages (although data allowances

were not directly equivalent). In all cases,

adjusting for PPP gave a higher relative price

than the nominal dollar equivalent.

• The good news is that, on average, mobile-

voice, mobile-data and fixed-broadband

prices are falling steadily around the world,

and in some countries even dramatically.

The reduction in price relative to income

is even more dramatic, suggesting that,

globally, telecommunication/ICT services

are becoming more affordable. However,

this trend in annual average prices is

not necessarily true of all countries or of

the entire population in each country.

Furthermore, falling prices are not

translated into rapidly increasing Internet

penetration rates, especially in least

developed countries (LDCs), pointing to the

fact that affordability may not be the only

barrier to Internet uptake.

Mobile-data-and-voice baskets

• The ITU mobile-data-and-voice baskets

include voice, text messages and data

for two different consumption levels. The

low-consumption mobile-data-and-voice

basket includes 70 voice minutes, 20 SMSs

and 500 MB of broadband data while the

high-consumption mobile-data-and-voice

basket includes 140 voice minutes, 70 SMSs

and 1.5 GB of broadband data. For the

low-consumption mobile-data-and-voice

basket, large differences in absolute price

levels between developed, developing and

least developed countries were apparent.

For the high-consumption mobile-data-

and-voice basket on the other hand, little

difference was evident in absolute prices by

level of development.

• Expressing prices relative to GNI per capita

(GNI p.c.), as a measure of affordability,

reveals huge gaps between prices

for different levels of development. In

developed countries, the price of a low-

consumption mobile-data-and-voice basket

was equivalent to 1 per cent of GNI p.c. in

2019. In developing countries, this basket

cost 7.5 per cent of GNI p.c., while in the

LDCs this rose sharply to 17 per cent. For

high-consumption mobile-data-and-voice

baskets, the differences were even larger.

• At the regional level, Europe had the most

affordable prices, ahead of the CIS region.

A second group of regions was formed

by the Americas, the Arab States and

Asia and the Pacific, all with reasonably

affordable prices. In Africa, however, a low-

consumption mobile-data-and-voice basket

already accounted for 16 per cent of GNI

p.c., and a high-consumption mobile-data-

and-voice basket amounted to no less than

31.2 per cent of GNI p.c., nearly one-third

of the average GNI p.c. in the region.

Mobile-voice basket

• Between 2008 and 2019, the global average

price of a mobile-voice basket decreased

from USD 21.4 to USD 11.8, equivalent to

a compound annual growth rate (CAGR)

of -5.3 per cent. PPP$-adjusted mobile

prices fell by -4.4 per cent CAGR, although

correcting for PPP effectively eliminates

price differences between developed

countries, developing countries and LDCs.

• Expressing mobile-voice prices as a share

of GNI p.c. introduces large variations in

price, with Africa and LDCs experiencing

relatively high mobile prices.

• The affordability gap between developed

and developing countries was reduced

from 9 to 2.9 percentage points between

2008 and 2019.

• In most countries, an entry-level mobile-

voice basket remains fairly affordable. In 70

countries, a low-usage mobile-voice plan

was available for less than 1 per cent of GNI

p.c., and in a further 37 countries it stood

below 2 per cent.

• Although causality is difficult to prove,

price reductions have undoubtedly helped

contribute to the rapid rise in the mobile-

voice penetration rate, alongside growing

competition and better price monitoring

and evaluation by regulators.

Mobile-data basket

• The global average price of a mobile-data

basket of at least 1.5 GB dropped by 7

per cent on average annually between

2013 and 2019.

• In terms of GNI p.c., there has been a

significant reduction in prices from 2013 to

2019. The global average price of a mobile-

data basket of 1.5 GB shrank from 8.4 per

cent of GNI p.c. in 2013 to 3.2 per cent in

2019, a CAGR of almost -15 per cent.

• A key benchmark is the 2 per cent target

set by the UN Broadband Commission

for Sustainable Development. For mobile

data, in 2019 in 95 countries, the cost of a

mobile-data basket of 1.5 GB was less than

2 per cent of GNI p.c. These 95 countries

consisted of 44 developed countries,

47 developing countries (non-LDCs),

and four LDCs. In 48 countries, of which

one developed country, 40 developing

countries and seven LDCs, prices were only

just above the Broadband Commission

Target, at 2-5 per cent of GNI p.c. In the

remaining nine developing countries and

31 LDCs, much progress still needs to be

made in order to reach the 2 per cent target

by 2025. In nine LDCs in particular, prices

were more than 20 per cent of GNI p.c.

2

Measuring Digital Development: ICT Price Trends 2019

Table 1: Global average prices for the five baskets, 2019

Mobile-data-

and-voice –

low usage

Mobile-data-

and-voice –

high usage

Mobile-

voice

Mobile-

data

Fixed-

broadband

Nominal price (converted into USD) USD 17 USD 25 USD 12 USD 14 USD 28

PPP$-adjusted price PPP$ 25 PPP$ 38 PPP$ 18 PPP$ 20 PPP$ 43

Affordability (percentage of GNI

per capita)

5.9% 10.3% 4.3% 4.3% 10.3%

Compound annual growth rate –

price in USD

-5.3%

(2008-2019)

-7%

(2013-2019)

-4.4%

(2008-2019)

Compound annual growth rate –

price in PPP$

-4.4%

(2008-2019)

-6%

(2013-2019)

-2.5%

(2008-2019)

Compound annual growth rate

– affordability

-9.3%

(2008-2019)

-15%

(2013-2019)

-9%

(2008-2019)

Measuring Digital Development: ICT Price Trends 2019

3

• While average prices for the mobile-voice

basket and the mobile-data basket are very

similar across levels of development and

regions, the gap in the penetration rate for

mobile-broadband and Internet uptake

between developed and developing

countries is much larger than the gap in

mobile-cellular uptake, in particular in LDCs.

One conclusion that could be drawn is that

if people in low-income countries have

the choice between a mobile-cellular or a

mobile-broadband subscription, preference

is given to the mobile-cellular subscription.

It also indicates that affordability is not the

only barrier to Internet use, but that other

barriers are important too, such as low level

of education, lack of relevant content, lack

of skills, in addition to a potentially low-

quality Internet connection, preventing

effective use.

Fixed-broadband basket

• From 2008 to 2019, the average price of an

entry-level fixed-broadband subscription,

converted into USD using market

exchange rates, decreased from USD 44 to

USD 27, equalling a CAGR of -4.4 per cent,

despite a certain levelling-out of prices

from 2016 onwards.

• Low nominal and PPP-adjusted prices stand

out in the CIS region, whereas the highest

nominal and PPP-adjusted prices are to be

found in Africa.

• Affordability is very dispersed according

to countries’ level of development. In

developed countries, an entry-level fixed-

broadband subscription cost 1.4 per cent of

GNI p.c.; in developing countries, this stood

at over 13 per cent, and nearly 36 per cent

in LDCs, over a third of average GNI p.c.

• Europe is the region with the lowest fixed-

broadband prices as a percentage of GNI

p.c. (1.4 per cent), followed by the CIS

region (3.7 per cent). Europe also enjoys

the highest median entry-level speeds.

In Africa, an entry-level fixed-broadband

subscription cost 33.3 per cent of GNI p.c.

• Over the past four years, the affordability

of fixed broadband has not changed

substantially, but advertised download

speeds are increasing.

• Despite the modest improvement in

affordability, fixed-broadband subscriptions

kept on increasing steadily around the

world, highlighting the importance of fixed

broadband. Wireless broadband networks

still carry far less traffic than fixed networks,

and they generally offer lower speeds and

reliability.

• The UN Broadband Commission set a

target for affordable entry-level service

as 2 per cent of GNI p.c. In 2019, 64

countries had achieved this target for fixed

broadband, mostly in Europe. Forty-five

countries are approaching the target,

whereas 34 developing countries and 30

LDCs still have a long way to go.

New benchmarks for a changing market

Efficient and reliable communication services are a foundation of socio-economic growth for many

countries, and have become hugely popular with consumers, both for work and entertainment.

Consumers and individuals can acquire important digital skills through access to, and experience

with, telecommunication/ICT devices and services and digital technologies. Today, such digital

skills are important in determining an individual’s competitiveness in the job market and access to

better-paid jobs.

Consumer surveys, however, have repeatedly identified affordability as a key barrier to access,

across many different countries. ITU, with its partners and stakeholders, regularly develops and

refines price methodologies for monitoring fixed and mobile broadband prices. To accurately

track and compare prices in statistical terms across different countries or across comparisons is no

straightforward exercise. Price comparisons are difficult, depending on whether they are conducted

within a single country or shared-currency region, versus internationally (when exchange rates and

PPP can complicate matters). They also depend on market share (i.e. whether the operator’s price

offering is for a large or niche customer base) and whether offers are bundled with other services.

Various market trends can complicate comparisons, such as the technological capability to provide

telephone, video and data communications over a single network (network convergence), the

growing number of operators, and intensifying competition (especially in mobile). For example, it

has become feasible to offer dual-play packages for voice and data, triple-play packages for phone,

television and Internet, and even quadruple-play packages combining fixed and wireless services.

Over and above convergence, mobile networks have underwent rapid development with the

introduction of mobile broadband and smartphones. Content platforms such as Facebook, Google,

Skype, WeChat, Line, Kakao, LinkedIn and WhatsApp also began offering a variety of text, voice and

video services that competed with traditional telecommunication and media services. These changes

have helped drive the decline of fixed telephony, the stagnation of voice revenues and increased

demand for data. To remain profitable in the new market environment, telecommunication

operators have had to ensure that their service offerings and pricing strategies evolve.

ITU maintains a set of different price baskets to track and compare market prices. To better reflect

the current realities of telecommunication markets worldwide, ITU has undertaken a major update

of the ICT price benchmark methodology, as endorsed by the eighth meeting of EGTI

1

held in

September 2017. This updated methodology was applied to price-data collection as from 2018,

which means that the ICT price benchmarks from 2018 onward are not directly comparable with

those of previous years.

Figure 1 provides an overview of the new price baskets adopted at the 2017 EGTI meeting.

The prices collected for each service correspond to the cheapest plan offered by the dominant

operator (in terms of market share) that fulfils the usage requirement of each basket (although

occasionally, when the market data were unclear, the historical incumbent or an alternative operator

was taken into account). The methodological details of the ITU price baskets are set out in Annex 1.

4

Measuring Digital Development: ICT Price Trends 2019

About this publication

With the aim of contributing to international, regional and national efforts to monitor the retail prices

and affordability of ICT services, this publication presents and analyses price data for five key services

based on the following five baskets:

1. mobile-data-and-voice basket (i.e. voice, SMS and mobile data combined) – low consumption

(70 minutes, 20 SMSs and 500 MB);

2. mobile-data-and-voice basket – high consumption (140 minutes, 70 SMSs and 1.5 GB);

3. mobile-voice (including voice and SMS);

4. mobile-data;

5. fixed-broadband.

For each basket, global and regional trends are presented, including time series insofar as they are

available, followed by country tables for the year 2019. An analysis is performed to identify which

countries and regions have achieved the UN Broadband Commission’s target for affordability.

Affordability gaps are also analysed, defined as the difference in price between developed and

developing countries.

Annex 1 describes the (revised) methodology. Annex 2 presents detailed tables with the underlying

data required to calculate the baskets. Country tables for the year 2018 for each of the five baskets

can be found in Annex 3.

Prices in this chapter are expressed in three complementary units:

• In United States dollars (USD), using the annual rates of exchange of the International Monetary

Fund (IMF). For those economies where IMF’s average annual rate of exchange was not

available, the average annual UN Operational Rate of Exchange was used, where available.

• In international dollars (PPP$), using PPP conversion factors instead of market exchange rates.

The use of PPP exchange factors helps to screen out price and exchange-rate distortions, thus

Measuring Digital Development: ICT Price Trends 2019

5

Figure 1: New ITU ICT price baskets (from 2018)

Source: ITU

providing a measure of the cost of a given service taking into account the purchasing power

equivalences between countries.

2

• As a percentage of countries’ monthly GNI p.c. (Atlas method).

3

Prices are expressed as a

percentage of GNI p.c. in order to present them relative to the size of the economy of each

country, averaged by population, thus providing an indication of the affordability of each ICT

service at country level.

Mobile-data-and-voice baskets

The introduction of prices for combined mobile services is a major departure from ITU’s previous

approach to ICT price data collection. In an increasing number of countries, operators offer several

products or services as one package with a single bill. Such bundled services are becoming the

norm and this trend is now reflected in ITU’s new, updated ICT price benchmarks.

4

Bundling is becoming increasingly widespread, as it enables converged telecommunication and

media companies to take greater advantage of consumers’ willingness-to-pay, thus increasing

revenues. It is not yet clear whether, on balance, price bundling benefits consumers or helps to close

gaps in access to broadband. For consumers, one main advantage of bundles is that they are often

offered at a discount, whereas stand-alone services are not. It may nevertheless be detrimental to

consumer welfare if price bundling limits choice and/or forces consumers to purchase services they

do not value.

Price bundling could potentially harm market competition when the use of bundles by network

operators deters market entry or increases the cost of switching between networks for consumers.

Bundling can deter market entry when a competing operator lacks access to wholesale inputs and is

unable to offer bundles at competitive rates. For consumers, bundles can complicate comparisons

between different service offerings, thus potentially making it difficult for them to switch between

network operators.

The lack of internationally comparable data makes it hard to assess the impacts of price bundling on

consumer welfare, competition and universal broadband access. ITU’s inclusion of mobile-data-and-

voice baskets in its price benchmarks is a first step in addressing this gap.

The ITU mobile-data-and-voice baskets include voice, text messages and data for two different

consumption levels. When EGTI analysed the mean and median values for voice (minutes of use

per month), SMSs per month and data (MB/GB per month) for two groups of consumption, a

clear disparity emerged in consumption patterns among countries in the low-income group and

those in the lower-middle, upper-middle and high-income groups.

5

The evidence suggested that

two consumption patterns ought to be considered, and this approach was adopted. The low-

consumption data-and-voice basket includes 70 voice minutes, 20 SMSs and 500 MB of broadband

data; the high-consumption data-and-voice basket includes 140 voice minutes, 70 SMSs and 1.5 GB

of broadband data.

Global trends

Chart 1 shows the price of the low-consumption and high-consumption data-and-voice baskets

in 2019 in USD, by level of development and by region. The average price globally for a low-

consumption data-and-voice basket stood at USD 17 in 2019, whereas on average a high-

consumption data-and-voice basket cost USD 25.

6

Measuring Digital Development: ICT Price Trends 2019

Chart 1: Mobile-data-and-voice baskets in USD, 2019

13

13

15

6

17

23

17

19

16

12

25

22

22

9

24

32

25

26

25

23

0

5

10

15

20

25

30

35

USD

Lowusage Highusage

Note: Simple averages. Based on 192 economies for which data on prices of mobile-data-and-voice baskets in USD

are available for the year 2019.

Source: ITU. USD exchange rates are from the IMF or UN.

For the low-consumption data-and-voice basket, there is a significant difference in price level,

according to level of development, when converting nominal prices in national currency into USD. In

developed countries, this data-and-voice basket cost USD 19, decreasing to USD 16 in developing

countries and USD 12 in the LDCs.

6

For the high-consumption data-and-voice basket, there was little

difference in prices by level of development.

Looking at the regions

7

, prices are comparatively low in the CIS region for both the low-consumption

and the high-consumption data-and-voice baskets, whereas higher prices are observed in the

Americas. Prices in the other four regions are close to the global average.

When converting prices from national currencies to international PPP$, a different picture emerges

(see Chart 2). In this case, there is little price difference between developed countries, developing

countries and LDCs for the low-consumption basket. For the high-consumption basket, however,

prices in developed countries are below the global average. In developing countries, prices are just

above the global average, whereas in LDCs they are significantly above it.

From a regional perspective, the CIS region still has the lowest prices, and in the Americas prices are

high;. What stands out most, however, is the high price for the high-consumption data-and-voice

basket in Africa, at a monthly average of PPP$ 50.

Measuring Digital Development: ICT Price Trends 2019

7

Chart 2: Mobile-data-and-voice basket in PPP$, 2019

27

23

20

13

21

32

25

22

26

24

50

39

31

18

30

43

38

31

40

45

0

10

20

30

40

50

60

PPP$

Lowusage Highusage

Note: Simple averages. Based on 165 economies for high-usage data-and-voice baskets and 162 economies for low-

usage data-and-voice baskets for which data on prices of mobile-data-and-voice baskets in PPP$ are available for the

year 2019.

Source: ITU. PPP$ conversion factors are from the World Bank.

When prices are expressed relative to GNI p.c., income levels are also taken into account. This has a

significant impact on price comparisons across the world (see Chart 3). Globally, the average price

of a low-consumption data-and-voice basket stood at 5.9 per cent of GNI p.c. in 2019, whereas the

price of a high-consumption data-and-voice basket stood at 10.3 per cent. There is a considerable

gap between prices at different levels of development.

In developed countries, a low-consumption data-and-voice basket cost 1 per cent of GNI p.c. in

2019. In developing countries, the same basket cost 7.5 per cent of GNI p.c., while in LDCs this rose

sharply to 17 per cent. For the high-consumption data-and-voice baskets, the differences are even

starker, with 1.4 per cent in developed countries, 13.2 per cent in developing countries and 32.3 per

cent in LDCs. It is interesting to note that in developed countries, there is only a very small difference

between the average price for a low-consumption and a high-consumption data-and-voice basket,

whereas in developing countries, and especially in LDCs, the difference is considerable. This

highlights the particular importance of the low-consumption data-and-voice basket for low-income

countries, as a more affordable means of access to a mobile-data-and-voice basket. At the same

time, these observations validate EGTI’s decision to establish these two data-and-voice baskets for

price comparison purposes.

At regional level, there are significant differences too. The most affordable prices are found in

Europe, ahead of the CIS region. A second group of regions is formed by the Americas, the Arab

States and Asia and the Pacific, all with reasonably affordable prices. In Africa, on the other hand, a

low-consumption data-and-voice basket already accounts for 16 per cent of GNI p.c., and a high-

consumption data-and-voice basket amounts to no less than 31.2 per cent of GNI p.c., nearly one-

third of GNI p.c. in the region.

8

Measuring Digital Development: ICT Price Trends 2019

Benchmarking countries

Table 2 presents the country-level details for high-consumption mobile-data-and-voice baskets, i.e.

those data-and-voice baskets offering at least 140 minutes of voice communication, 70 SMSs and

1.5 GB of data, for the year 2019.

8

Not surprisingly, the most affordable plans in terms of GNI p.c.

are to be found in high-income countries. Nevertheless, the 33 countries in which high-consumption

mobile-data-and-voice baskets can be purchased for less than 1 per cent of GNI p.c. include four

middle-income countries: the Russian Federation, India, Turkey and Sri Lanka. At the other end of

the scale, the 46 countries in which a high-consumption mobile-data-and-voice basket accounts for

over 10 per cent of GNI p.c. are almost all low or lower-middle income countries.

Measuring Digital Development: ICT Price Trends 2019

9

Chart 3: Mobile-data-and-voice basket as a % of GNI p.c., 2019

16.0

4.0

4.3

2.0

1.0

3.9

5.9

1.0

7.5

17.0

31.2

7.3

6.5

2.7

1.4

5.6

10.3

1.4

13.2

32.3

0

5

10

15

20

25

30

35

Asa%ofGNIp.c.

Lowusage Highusage

Note: Simple averages. Based on 182 economies for high-usage data and voice baskets and 179 economies for low-

usage data-and-voice baskets for which data on prices of mobile-data-and-voice baskets in PPP$ are available for the

year 2019.

Source: ITU. GNI p.c. data are from the World Bank.

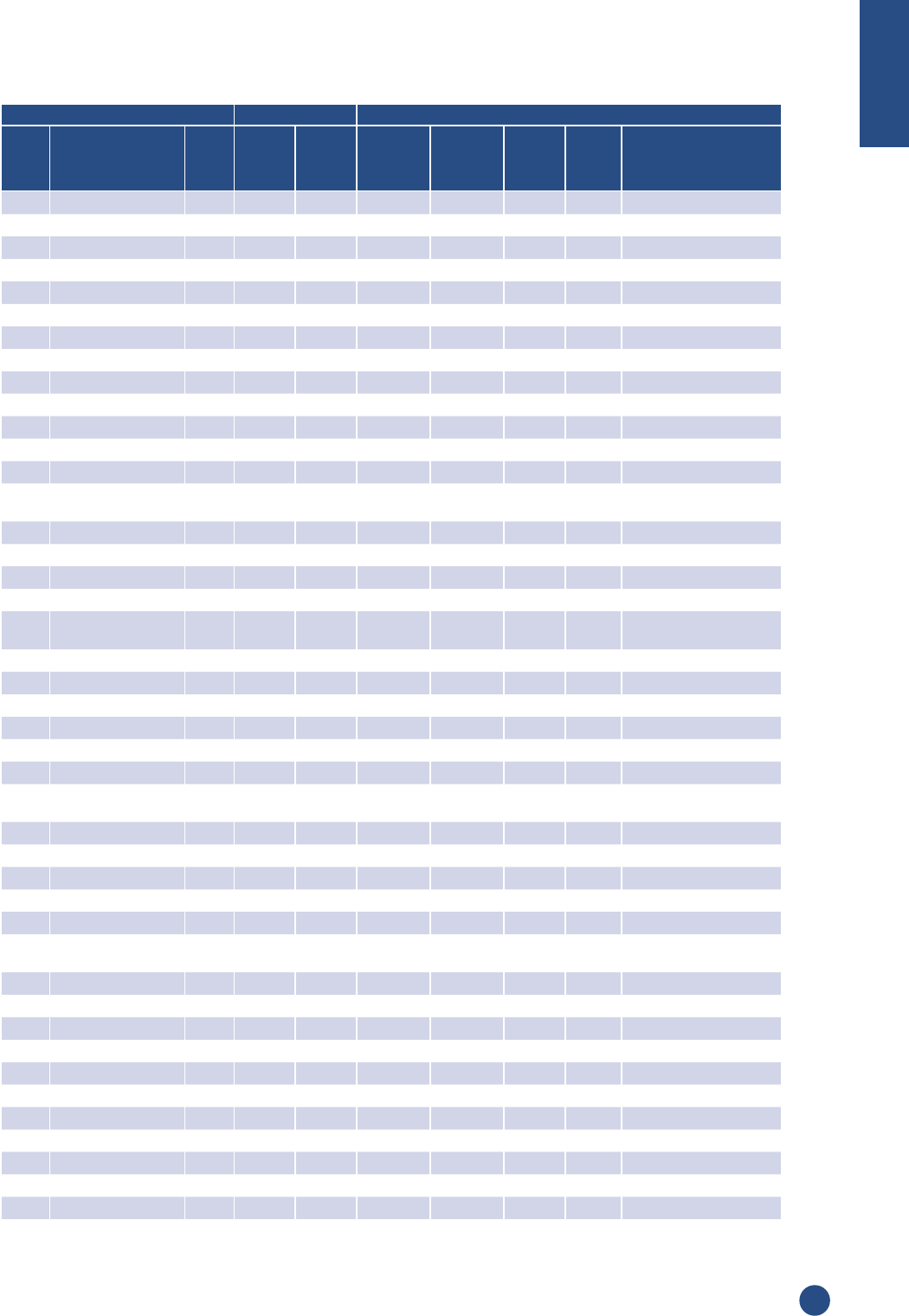

Table 2: High-consumption mobile-data-and-voice basket, 2019

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly voice

call allowance

(in minutes)

Monthly SMS

allowance

Monthly

data

allowance

(in GB)

Tax rate

included

(%)

GNI p.c.,

USD,

2018

1 Macao, China 0.2 14.31 17.82 480 70 2.0 0.0 78,320

2 Singapore 0.3 14.83 17.64 150 500 5.0 7.0 58,770

3 Qatar 0.3 16.48 21.62 140 70 2.0 0.0 61,190

4 Israel 0.3 11.11 9.42 1,500 2,500 30.0 17.0 40,850

5 Luxembourg 0.3 21.25 18.48 500 500 3.0 77,820

6 Hong Kong, China 0.4 16.53 20.23 140 70 2.0 0.0 50,310

7 Austria 0.4 16.63 16.76 1,000 1,000 4.0 20.0 49,250

8 New Zealand 0.4 14.53 13.08 200 500 1.8 15.0 40,820

9 Sweden 0.5 22.89 21.28 Unlimited Unlimited 2.0 25.0 55,070

10 Switzerland 0.5 35.79 25.45 Unlimited Unlimited 1.5 7.7 83,580

11 Denmark 0.5 26.76 21.15 Unlimited Unlimited 10.0 25.0 60,140

12 Iceland* 0.5 27.61 19.31 Unlimited Unlimited 5.0 24.0 60,740

13 Norway 0.5 36.77 27.73 Unlimited Unlimited 3.0 25.0 80,790

14 Netherlands 0.6 24.80 24.22 Unlimited Unlimited 2.0 21.0 51,280

15 Finland 0.7 26.44 23.65 140 70 Unlimited 24.0 47,820

16 Belgium 0.7 25.97 25.66 120 Unlimited 1.5 21.0 45,430

17 United Kingdom 0.7 25.35 24.08 Unlimited Unlimited 3.0 20.0 41,330

18 Russian Federation 0.7 6.38 15.28 200 200 4.0 20.0 10,230

19 Italy 0.8 21.26 23.06 Unlimited 500 20.0 22.0 33,560

20 Estonia 0.8 14.17 19.86 Unlimited Unlimited 5.0 20.0 20,990

21 Kuwait 0.8 23.18 35.58 Unlimited Unlimited 5.0 0.0 33,690

22 Australia 0.8 36.61 31.86 Unlimited Unlimited 15.0 10.0 53,190

23 United States 0.8 43.55 43.55 Unlimited Unlimited 1.5 8.9 62,850

24 Ireland 0.8 41.33 35.58 Unlimited Unlimited 20.0 23.0 59,360

25 India 0.9 1.43 4.75 Unlimited 300 2.0 18.0 2,020

26 Slovenia 0.9 17.70 23.14 Unlimited Unlimited 2.0 22.0 24,670

27 Germany 0.9 34.59 36.39 Unlimited 70 1.5 19.0 47,450

28 Lithuania 0.9 12.87 21.83 Unlimited Unlimited 2.0 21.0 17,360

29 Spain 0.9 22.12 26.19 Unlimited 70 3.0 21.0 29,450

30 France 0.9 31.87 31.88 Unlimited Unlimited 10.0 20.0 41,070

31 Turkey 0.9 8.08 23.20 750 100 2.5 25.5 10,380

32 United Arab Emirates 1.0 33.74 43.95 140 70 1.5 5.0 41,010

33 Sri Lanka 1.0 3.34 10.21 140 70 1.5 37.7 4,060

34 Latvia 1.0 14.16 21.30 Unlimited Unlimited 2.0 21.0 16,880

35 Portugal 1.0 18.90 24.06 250 250 3.0 23.0 21,680

36 Poland 1.1 12.46 24.12 Unlimited Unlimited 7.0 23.0 14,150

37 Kazakhstan 1.1 6.93 19.96 Unlimited 100 12.0 12.0 7,830

38 Korea (Rep. of) 1.1 27.96 31.99 Unlimited Unlimited 1.5 10.0 30,600

39 Romania 1.1 10.63 22.53 Unlimited Unlimited 30.0 19.0 11,290

40 Mauritius 1.2 12.20 20.81 140 1,000 1.7 15.0 12,050

41 Saudi Arabia 1.2 22.00 45.14 500 70 2.0 5.0 21,540

42 China 1.2 9.82 17.05 150 70 3.0 0.0 9,470

43 Bahrain 1.2 22.71 37.49 500 70 6.0 5.0 21,890

44 Brunei Darussalam 1.3 32.99 58.77 140 70 3.0 0.0 31,020

45 Ukraine 1.3 2.83 10.73 Unlimited 100 1.9 20.0 2,660

46 Mexico 1.4 10.39 19.66 Unlimited Unlimited 1.5 16.0 9,180

47 Azerbaijan 1.4 4.59 18.71 140 200 2.0 18.0 4,050

48 Egypt 1.4 3.22 16.46 330 70 1.5 43.0 2,800

10

Measuring Digital Development: ICT Price Trends 2019

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly voice

call allowance

(in minutes)

Monthly SMS

allowance

Monthly

data

allowance

(in GB)

Tax rate

included

(%)

GNI p.c.,

USD,

2018

49 Armenia 1.5 5.18 12.84 2,500 250 3.9 20.0 4,230

50 Chile 1.5 18.54 25.78 350 70 5.0 14,670

51 Greece 1.5 24.84 31.82 300 100 1.5 24.0 19,540

52 Malaysia 1.5 13.38 32.50 Unlimited 70 6.0 0.0 10,460

53 Bahamas* 1.6 39.96 35.27 3,000 3,000 2.0 12.0 30,210

54 Japan 1.6 55.85 56.80 140 70 2.0 8.0 41,340

55 Malta 1.6 35.43 47.48 140 70 1.5 18.0 26,220

56 Cyprus 1.6 36.02 44.06 Unlimited Unlimited 1.5 19.0 26,300

57 Oman 1.7 21.07 41.48 140 100 1.5 0.0 15,110

58 Peru 1.7 9.13 17.37 Unlimited Unlimited 2.9 6,530

59 Aruba* 1.7 33.52 40.02 1,000 100 4.0 23,630

60 Uruguay 1.8 22.95 27.54 433 Unlimited 1.5 15,650

61 Palau 1.8 25.00 26.86 190 2,000 2.0 0.0 16,910

62 Costa Rica 1.8 17.09 26.60 140 70 2.0 13.0 11,510

63 Brazil 1.8 13.68 22.23 Unlimited Unlimited 3.0 40.2 9,140

64 Belarus 1.8 8.55 33.80 250 70 1.5 25.0 5,670

65 Slovakia 1.9 28.34 44.46 Unlimited Unlimited 1.5 20.0 18,330

66 Tunisia 1.9 5.44 16.37 140 70 1.5 25.0 3,500

67 Panama 2.0 24.00 41.84 140 70 Unlimited 14,370

68 Croatia 2.1 23.73 38.28 Unlimited Unlimited 5.0 25.0 13,830

69 Viet Nam 2.2 4.34 10.56 200 70 3.0 10.0 2,400

70 Czech Republic 2.2 36.77 57.52 Unlimited Unlimited 4.0 21.0 20,250

71 Bangladesh 2.2 3.19 7.83 150 200 1.5 21.0 1,750

72 Namibia 2.2 9.67 19.20 400 2,800 4.0 15.0 5,250

73 Canada 2.2 83.42 80.67 Unlimited Unlimited 2.0 13.0 44,860

74 Georgia 2.3 7.89 Unlimited Unlimited 3.9 18.0 4,130

75 Philippines 2.4 7.52 19.39 400 Unlimited 4.0 12.0 3,830

76 Saint Kitts and Nevis 2.4 37.04 49.15 1,000 1,000 10.0 18,640

77 Morocco 2.5 6.39 14.54 160 100 2.0 20.0 3,090

78 Algeria 2.5 8.58 24.74 Unlimited Unlimited 13.0 19.0 4,060

79 Puerto Rico 2.5 44.60 Unlimited Unlimited 8.0 11.5 21,100

80 Uzbekistan 2.6 4.34 2,000 200 1.5 20.0 2,020

81 Bhutan 2.6 6.65 20.01 140 70 1.9 5.0 3,080

82 Myanmar 2.6 2.85 11.20 140 70 1.5 5.0 1,310

83 Colombia 2.6 13.53 28.34 500 2,000 4.4 23.0 6,190

84 Moldova 2.6 6.55 15.30 180 300 2.0 20.0 2,990

85 Bulgaria 2.6 19.53 43.13 200 80 1.5 20.0 8,860

86

Iran (Islamic Republic

of)*

2.7 12.24 39.06 1,000 1,000 2.0 9.0 5,470

87 Albania 2.7 11.11 23.20 2,500 2,200 2.0 20.0 4,860

88 Antigua and Barbuda 2.8 37.04 45.57 700 700 7.0 15,810

89 Montenegro 2.8 19.95 39.30 5,200 5,000 4.0 21.0 8,400

90 Kyrgyzstan 2.9 2.91 9.56 1,200 2,000 4.1 17.0 1,220

91 Pakistan 2.9 3.78 13.72 2,000 2,000 2.0 0.0 1,580

92 Indonesia 2.9 9.22 25.72 140 100 10.0 10.0 3,840

93 Barbados* 3.0 37.50 29.83 Unlimited Unlimited 1.5 15,240

94 Trinidad and Tobago 3.1 41.54 49.70 300 70 3.0 12.5 16,240

95 Ecuador 3.2 16.10 27.71 200 70 2.0 12.0 6,120

96 Maldives 3.2 24.86 32.67 140 70 2.5 6.0 9,310

97 Suriname 3.2 13.40 300 300 1.5 8.0 4,990

Measuring Digital Development: ICT Price Trends 2019

11

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly voice

call allowance

(in minutes)

Monthly SMS

allowance

Monthly

data

allowance

(in GB)

Tax rate

included

(%)

GNI p.c.,

USD,

2018

98 Hungary 3.3 40.30 72.25 140 70 3.0 5.0 14,590

99 Serbia 3.4 17.95 36.89 140 100 3.0 20.0 6,390

100 North Macedonia 3.4 15.33 35.03 Unlimited Unlimited 10.0 18.0 5,450

101 Jordan 3.7 12.93 26.82 5,000 200 4.0 46.0 4,210

102 Dominica 3.7 22.22 31.01 Unlimited Unlimited 1.5 7,210

103 Mongolia 3.7 11.17 30.80 140 70 3.0 10.0 3,580

104 Libya 3.9 20.44 140 70 2.0 0.0 6,330

105 Seychelles 3.9 50.78 80.25 140 70 1.5 15.0 15,600

106 Tonga 4.0 14.31 18.67 4,000 4,000 1.5 15.0 4,300

107 Nigeria 4.1 6.73 13.35 140 70 3.0 5.0 1,960

108 Saint Lucia 4.2 32.78 42.89 Unlimited Unlimited 8.0 9,460

109 Grenada 4.3 35.19 47.85 300 Unlimited 8.0 9,780

110 Gabon 4.4 25.19 36.81 240 800 2.3 18.0 6,800

111 Thailand 4.6 25.49 66.08 300 70 1.5 7.0 6,610

112 Dominican Rep. 4.7 28.75 62.44 200 1,000 3.0 30.0 7,370

113 Jamaica 4.7 19.63 30.65 Unlimited 70 3.5 25.0 4,990

114 Paraguay 4.8 22.77 48.79 Unlimited 70 3.0 10.0 5,680

115 Curacao* 5.2 82.31 104.76 Unlimited Unlimited 5.0 6.0 19,070

116

Saint Vincent and the

Grenadines

5.3 35.04 48.67 500 70 3.0 7,940

117

Bosnia and

Herzegovina

5.4 25.47 53.61 140 70 3.0 17.0 5,690

118 Turkmenistan 5.8 32.86 2,000 500 1.5 15.0 6,740

119 Nepal (Republic of) 6.2 4.96 14.52 490 300 1.5 26.0 960

120 Ghana 6.2 11.01 30.47 400 70 2.0 23.5 2,130

121 Nauru 6.3 58.73 140 70 1.8 15.0 11,240

122 Belize 6.4 25.00 180 Unlimited 5.4 12.5 4,720

123 Guyana 6.7 26.48 42.50 150 150 4.5 14.0 4,760

124 El Salvador 6.7 21.25 42.27 Unlimited 70 6.0 3,820

125 Tajikistan 6.8 5.75 140 100 1.6 23.0 1,010

126 South Africa 7.3 34.79 69.78 140 70 1.5 15.0 5,720

127 Kenya 7.5 10.12 20.40 140 70 2.0 31.0 1,620

128 Côte d'Ivoire 7.5 10.08 24.64 560 560 21.9 18.0 1,610

129 Lebanon 7.6 48.40 75.90 140 110 1.8 10.0 7,690

130 Eswatini 8.5 27.19 64.77 300 100 2.0 14.0 3,850

131 Samoa 8.6 30.07 41.32 140 70 12.0 15.0 4,190

132 Fiji 8.8 42.91 67.82 140 70 3.0 9.0 5,860

133 Timor-Leste 9.0 13.60 21.16 700 700 1.8 5.0 1,820

134 Iraq 9.1 38.30 76.29 140 70 2.0 0.0 5,030

135 Argentina 9.7 99.98 140 70 4.0 12,370

136 Palestine 9.8 30.25 43.48 140 70 2.5 16.0 3,710

137 Lao P.D.R. 10.7 21.90 58.24 140 70 1.5 10.0 2,460

138

Bolivia (Plurinational

State of)

12.0 33.57 67.24 140 70 2.0 13.0 3,370

139 Mauritania 12.0 11.94 33.76 140 70 4.0 18.0 1,190

140 Cambodia 12.4 14.25 34.87 140 70 1.5 10.0 1,380

141 Guinea 12.7 8.79 17.36 140 100 2.0 11.0 830

142 Angola 12.8 35.89 46.14 140 70 2.0 10.0 3,370

143 Tanzania 13.8 11.71 31.43 140 1,000 2.1 32.5 1,020

144 Micronesia 14.1 42.00 42.98 140 900 2.0 0.0 3,580

12

Measuring Digital Development: ICT Price Trends 2019

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly voice

call allowance

(in minutes)

Monthly SMS

allowance

Monthly

data

allowance

(in GB)

Tax rate

included

(%)

GNI p.c.,

USD,

2018

145 Botswana 14.2 91.67 175.06 140 70 1.5 12.0 7,750

146 Zambia 14.7 17.54 44.73 140 70 1.5 33.5 1,430

147 Honduras 15.0 29.06 57.02 1,200 70 4.0 15.0 2,330

148 Lesotho 15.6 17.97 48.63 248 70 2.0 9.0 1,380

149 Nicaragua 15.7 26.62 71.64 160 400 4.0 15.0 2,030

150 Ethiopia 16.3 10.72 31.51 166 70 2.0 15.0 790

151 Kiribati 18.1 47.37 140 70 2.7 0.0 3,140

152 Sao Tome and Principe 19.2 30.18 42.36 140 70 3.0 5.0 1,890

153 Guatemala 19.3 70.89 118.39 140 70 2.5 12.0 4,410

154 Cabo Verde 19.7 56.52 118.46 140 70 2.0 15.0 3,450

155 Rwanda 19.9 12.94 35.53 140 70 2.0 28.0 780

156 Vanuatu 20.6 51.01 47.88 140 70 2.5 15.0 2,970

157 Gambia 21.8 12.71 41.01 140 70 1.5 21.3 700

158 Afghanistan 21.8 9.99 34.00 140 70 2.0 0.0 550

159 Comoros 21.8 24.00 360 240 2.0 0.0 1,320

160 Benin 22.0 15.93 40.99 140 70 1.6 18.0 870

161 Cameroon 22.5 26.99 64.61 899 500 1.5 0.0 1,440

162 Djibouti 24.2 43.89 77.46 180 100 3.8 10.0 2,180

163 Haiti 24.5 16.33 34.92 140 70 1.6 10.0 800

164 Senegal 25.3 29.73 72.17 1,400 Unlimited 4.1 23.0 1,410

165 Papua New Guinea 29.1 61.45 74.63 140 70 2.3 10.0 2,530

166 Solomon Islands 29.7 49.49 51.02 140 70 3.2 10.0 2,000

167 Madagascar 31.9 11.70 40.96 140 70 2.0 20.0 440

168 Yemen 32.0 25.59 300 100 3.2 5.0 960

169 Togo 35.2 19.07 46.89 240 70 1.5 18.0 650

170 Mali 45.1 31.17 79.45 140 70 2.0 18.0 830

171 Sierra Leone 46.1 19.20 50.01 140 70 2.0 15.0 500

172 Uganda 51.9 26.83 80.30 1,800 2,000 2.0 18.0 620

173 Niger 56.8 17.99 44.81 2,500 Unlimited 4.0 22.6 380

174 Chad 58.0 32.39 1,000 1,000 1.6 18.0 670

175 Liberia 60.0 30.00 28.68 1,500 300 20.0 14.0 600

176 Guinea-Bissau 61.0 38.15 87.56 140 70 5.0 17.0 750

177 Central African Rep. 63.0 25.19 1,120 2,800 2.1 19.0 480

178 Burkina Faso 63.8 35.09 91.39 1,560 1,560 1.5 18.0 660

179 Malawi 73.4 22.03 64.94 140 70 2.0 26.5 360

180 Mozambique 81.4 29.84 6,300 1,800 1.8 17.0 440

181 Burundi 84.2 19.64 47.94 140 75 1.8 2.0 280

182

Dem. Rep. of the

Congo

112.2 45.80 250 70 1.8 26.0 490

Andorra** 29.63 200 100 1.5

Anguilla** 44.44 1,000 1,000 3.0 7.0

Cayman Islands** 64.08 300 70 3.0

Cuba** 55.55 140 70 2.5

Gibraltar** 40.03 300 300 2.0 0.0

Liechtenstein** 45.10 140 Unlimited 5.0 7.7

Monaco** 59.04 Unlimited Unlimited 50.0 20.0

Somalia** 12.70 140 70 2.0 10.0

Syrian Arab Republic** 33.34 140 100 1.8 5.0

Measuring Digital Development: ICT Price Trends 2019

13

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly voice

call allowance

(in minutes)

Monthly SMS

allowance

Monthly

data

allowance

(in GB)

Tax rate

included

(%)

GNI p.c.,

USD,

2018

Taiwan, Province of

China**

30.70 140 70 1.5 5.0

Note: Palestine is not an ITU Member State; the status of Palestine in ITU is the subject of Resolution 99 (Rev. Dubai,

2018) of the ITU Plenipotentiary Conference. * Data correspond to the GNI p.c. in 2017. ** Country not ranked because

data on GNI p.c. are not available.

Source: ITU. GNI p.c. and PPP$ conversion factors are from the World Bank. USD exchange rates are from the IMF or UN.

For the low-consumption mobile-data-and-voice baskets (i.e. those data-and-voice baskets offering

at least 70 minutes of voice communication, 20 SMSs and 500 MB of data), there are 49 countries

in which such a plan can be bought for less than 1 per cent of GNI p.c. (see Table 3), including 11

middle-income countries. Compared with the high-consumption data-and-voice basket, there are

16 more countries in which the cost is below 1 per cent of GNI p.c., owing to the lower allowances in

the plan in question. Conversely, there are also fewer countries in which the low-consumption data-

and-voice baskets are above 10 per cent of GNI p.c. – 30 in total – compared with 46 for the high-

consumption data-and-voice basket.

14

Measuring Digital Development: ICT Price Trends 2019

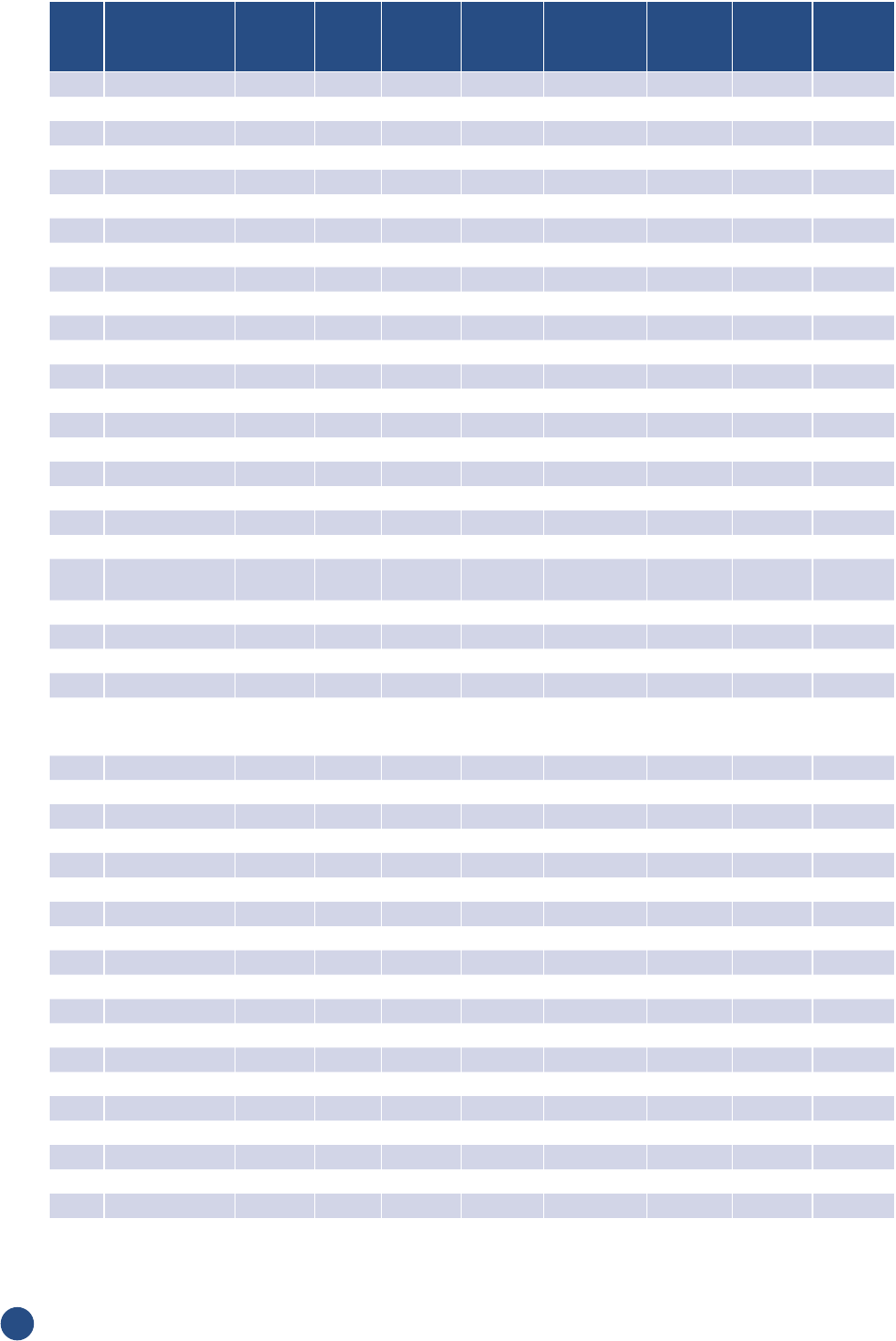

Table 3: Low-consumption mobile-data-and-voice basket, 2019

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly

voice call

allowance

(in minutes)

Monthly

SMS

allowance

Monthly

data

allowance

(in MB)

Tax rate

included

(%)

GNI p.c.,

USD, 2018

1 Luxembourg 0.1 5.89 5.13 70 30 1,024 77,820

2 Macao, China 0.1 6.57 8.18 480 20 880 0.0 78,320

3 Hong Kong, China 0.2 7.69 9.41 70 20 1,024 0.0 50,310

4 Austria 0.3 10.72 10.81 700 700 1,024 20.0 49,250

5 Singapore 0.3 14.83 17.64 150 500 5,120 7.0 58,770

6 New Zealand 0.3 10.38 9.34 200 50 500 15.0 40,820

7 Qatar 0.3 16.48 21.62 70 20 2,867 0.0 61,190

8 Israel 0.3 11.11 9.42 2,500 2,500 30,720 17.0 40,850

9 Estonia 0.3 5.90 8.28 Unlimited Unlimited 1,024 20.0 20,990

10 Iceland* 0.4 18.37 12.85 Unlimited Unlimited 500 24.0 60,740

11 Switzerland 0.4 25.57 18.18 Unlimited Unlimited 500 7.7 83,580

12 United Arab Emirates 0.4 13.14 17.12 70 20 500 5.0 41,010

13 Finland 0.4 16.66 14.90 70 20 Unlimited 24.0 47,820

14 Sri Lanka 0.5 1.53 4.68 70 50 500 37.7 4,060

15 Norway 0.5 30.62 23.09 70 20 1,024 25.0 80,790

16 Belgium 0.5 18.88 18.66 120 70 1,536 21.0 45,430

17 Sweden 0.5 22.89 21.28 Unlimited Unlimited 2,048 25.0 55,070

18 Denmark 0.5 26.76 21.15 70 20 10,240 25.0 60,140

19 Germany 0.6 22.19 23.35 Unlimited 20 1,024 19.0 47,450

20 Netherlands 0.6 24.80 24.22 Unlimited Unlimited 2,048 21.0 51,280

21 France 0.6 20.06 20.07 120 20 5,120 20.0 41,070

22 Portugal 0.6 10.63 13.53 70 20 500 23.0 21,680

23 Tunisia 0.6 1.74 5.23 70 20 500 19.0 3,500

24 Brunei Darussalam 0.6 15.94 28.40 70 20 1,024 0.0 31,020

25 United Kingdom 0.6 21.35 20.28 Unlimited Unlimited 1,024 20.0 41,330

26 United States 0.6 32.66 32.66 Unlimited Unlimited 500 8.9 62,850

27 Kuwait 0.6 17.88 27.45 100 20 5,120 0.0 33,690

28 Spain 0.7 16.40 19.42 Unlimited 20 3,072 21.0 29,450

29 Latvia 0.7 10.03 15.08 Unlimited Unlimited 500 21.0 16,880

30 Kazakhstan 0.7 4.73 13.61 Unlimited 20 4,096 12.0 7,830

31 Greece 0.7 11.81 15.13 300 50 600 24.0 19,540

32 Belarus 0.7 3.50 13.85 250 20 50 25.0 5,670

33 Russian Federation 0.7 6.38 15.28 200 200 4,096 20.0 10,230

34 Italy 0.8 21.26 23.06 Unlimited 500 20,480 25.0 33,560

35 Korea (Rep. of) 0.8 19.86 22.73 100 20 700 10.0 30,600

36 Oman 0.8 9.88 19.46 70 50 500 0.0 15,110

37 Mauritius 0.8 8.25 14.07 70 800 1,200 15.0 12,050

38 Australia 0.8 36.61 31.86 Unlimited Unlimited 15,360 10.0 53,190

39 Ireland 0.8 41.33 35.58 Unlimited Unlimited 20,480 23.0 59,360

40 India 0.9 1.43 4.75 Unlimited 300 2,048 18.0 2,020

41 Slovenia 0.9 17.70 23.14 Unlimited Unlimited 2,048 22.0 24,670

42 Egypt 0.9 2.01 10.29 280 20 500 43.0 2,800

43 Armenia 0.9 3.11 7.70 1,500 150 1,000 20.0 4,230

44 Lithuania 0.9 12.87 21.83 Unlimited Unlimited 2,048 21.0 17,360

45 China 0.9 7.19 12.48 70 20 1,024 0.0 9,470

46 Poland 0.9 10.80 20.91 Unlimited 20 3,072 23.0 14,150

47 Cyprus 0.9 20.08 24.56 300 300 500 19.0 26,300

48 Turkey 0.9 8.08 23.20 750 100 2,560 25.5 10,380

Measuring Digital Development: ICT Price Trends 2019

15

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly

voice call

allowance

(in minutes)

Monthly

SMS

allowance

Monthly

data

allowance

(in MB)

Tax rate

included

(%)

GNI p.c.,

USD, 2018

49 Slovakia 1.0 14.70 23.06 100 20 500 20.0 18,330

50 Bahrain 1.0 18.46 30.47 500 20 6,000 5.0 21,890

51 Mexico 1.0 7.79 14.75 Unlimited Unlimited 1,000 16.0 9,180

52 Saudi Arabia 1.0 18.67 38.30 500 20 2,000 5.0 21,540

53 Hungary 1.0 12.73 22.82 70 20 1,024 5.0 14,590

54 Uruguay 1.1 13.83 16.60 93 20 512 15,650

55 Chile 1.1 13.08 18.19 350 20 5,120 14,670

56 Malta 1.1 23.62 31.65 70 20 500 18.0 26,220

57 Azerbaijan 1.1 3.76 15.35 70 200 2,048 18.0 4,050

58 Romania 1.1 10.63 22.53 Unlimited Unlimited 30,720 19.0 11,290

59 Costa Rica 1.2 11.93 18.58 70 20 2,000 13.0 11,510

60 Myanmar 1.2 1.36 5.36 70 20 900 5.0 1,310

61 Malaysia 1.3 10.90 26.48 Unlimited 20 6,144 0.0 10,460

62 Bhutan 1.3 3.22 9.68 70 20 959 5.0 3,080

63 Ukraine 1.3 2.83 10.73 Unlimited 100 2,000 20.0 2,660

64 Iran (Islamic Republic of)* 1.3 6.12 19.53 400 400 1,000 9.0 5,470

65 Bangladesh 1.4 2.03 4.99 100 50 500 21.0 1,750

66 Japan 1.4 48.51 49.34 Unlimited 20 1,024 8.0 41,340

67 Canada 1.4 52.90 51.15 Unlimited 20 500 13.0 44,860

68 Czech Republic 1.4 24.34 38.08 Unlimited 20 500 21.0 20,250

69 Morocco 1.4 3.73 8.48 100 100 1,040 20.0 3,090

70 Indonesia 1.5 4.69 13.09 70 60 2,048 10.0 3,840

71 Barbados* 1.6 20.00 15.91 100 100 1,024 15,240

72 Maldives 1.6 12.23 16.08 70 20 70 6.0 9,310

73 Bahamas* 1.6 39.96 35.27 12,000 12,000 8,192 12.0 30,210

74 Panama 1.7 20.00 34.87 100 100 Unlimited 14,370

75 Peru 1.7 9.13 17.37 Unlimited Unlimited 3,000 6,530

76 Aruba* 1.7 33.52 40.02 1,000 100 4,096 23,630

77 Palau 1.8 25.00 26.86 190 2,000 2,048 0.0 16,910

78 Moldova 1.8 4.46 10.43 120 150 500 20.0 2,990

79 Brazil 1.8 13.68 22.23 Unlimited Unlimited 3,072 40.2 9,140

80 Uzbekistan 1.8 3.05 1,150 20 800 20.0 2,020

81 Montenegro 1.8 12.87 25.34 5,100 100 2,048 21.0 8,400

82 Puerto Rico 1.9 33.45 Unlimited Unlimited 1,024 11.5 21,100

83 Seychelles 1.9 24.97 39.46 70 20 1,024 15.0 15,600

84 Bulgaria 2.0 14.47 31.95 200 20 600 20.0 8,860

85 Viet Nam 2.0 3.98 9.69 200 30 3,072 10.0 2,400

86 Colombia 2.0 10.46 21.90 Unlimited Unlimited 750 23.0 6,190

87 Thailand 2.0 11.24 29.14 100 20 500 7.0 6,610

88 Albania 2.1 8.33 17.40 200 200 500 20.0 4,860

89 Serbia 2.1 10.96 22.53 Unlimited 100 500 20.0 6,390

90 Croatia 2.1 23.73 38.28 70 20 5,120 25.0 13,830

91 Namibia 2.2 9.67 19.20 1,400 2,800 800 15.0 5,250

92 Georgia 2.3 7.89 Unlimited Unlimited 4,000 18.0 4,130

93 Philippines 2.4 7.52 19.39 400 Unlimited 4,096 12.0 3,830

94 North Macedonia 2.4 10.88 Unlimited 20 1,536 18.0 5,450

95 Pakistan 2.4 3.20 11.63 10,000 10,000 1,000 0.0 1,580

96 Trinidad and Tobago 2.5 33.23 39.76 Unlimited Unlimited 1,000 12.5 16,240

97 Ecuador 2.5 12.60 21.69 200 20 2,000 12.0 6,120

16

Measuring Digital Development: ICT Price Trends 2019

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly

voice call

allowance

(in minutes)

Monthly

SMS

allowance

Monthly

data

allowance

(in MB)

Tax rate

included

(%)

GNI p.c.,

USD, 2018

98 Algeria 2.5 8.58 24.74 70 Unlimited 13,000 19.0 4,060

99 Bosnia and Herzegovina 2.6 12.10 25.47 70 20 500 17.0 5,690

100 Lebanon 2.7 17.60 27.60 70 440 60 10.0 7,690

101 Antigua and Barbuda 2.8 37.04 45.57 700 700 7,168 15,810

102 Kyrgyzstan 2.9 2.91 9.56 1,200 2,000 4,200 17.0 1,220

103 Paraguay 2.9 13.61 29.16 Unlimited 20 1,024 10.0 5,680

104 Libya 2.9 15.53 70 20 2,000 0.0 6,330

105 Mongolia 3.0 8.81 24.28 70 20 3,072 10.0 3,580

106 Suriname 3.0 12.52 70 60 550 8.0 4,990

107 Turkmenistan 3.1 17.14 2,000 500 500 15.0 6,740

108 South Africa 3.1 14.95 30.00 70 20 500 15.0 5,720

109 Ghana 3.2 5.62 15.55 100 40 500 23.5 2,130

110 Jordan 3.7 12.93 26.82 5,000 200 4,096 46.0 4,210

111 Dominica 3.7 22.22 31.01 Unlimited Unlimited 1,536 7,210

112 Gabon 3.8 21.59 31.55 240 1,350 900 18.0 6,800

113 Tonga 4.0 14.31 18.67 4,000 4,000 2,000 15.0 4,300

114 Nigeria 4.0 6.53 12.96 253 253 650 5.0 1,960

115 Nauru 4.2 39.49 70 20 1,843 15.0 11,240

116 Dominican Rep. 4.3 26.13 56.74 100 1,000 3,072 30.0 7,370

117 Iraq 4.3 18.09 36.04 70 20 500 0.0 5,030

118 Grenada 4.3 35.19 47.85 300 Unlimited 8,000 9,780

119 Jamaica 4.3 18.08 28.23 Unlimited 20 3,500 25.0 4,990

120 Nepal (Republic of) 4.6 3.65 10.69 70 20 1,500 26.0 960

121 Sao Tome and Principe 4.6 7.23 10.15 1,800 1,800 900 5.0 1,890

122 Eswatini 4.6 14.80 35.26 70 30 700 14.0 3,850

123 Guyana 4.6 18.34 29.44 80 80 3,500 4,760

124 Lao P.D.R. 4.9 10.11 26.88 70 20 540 10.0 2,460

125 El Salvador 5.0 16.07 31.97 Unlimited 20 6,144 3,820

126 Curacao* 5.2 82.31 104.76 Unlimited Unlimited 5,000 6.0 19,070

127 Angola 5.4 15.23 19.58 70 20 500 10.0 3,370

128 Kenya 5.5 7.38 14.88 70 20 2,048 31.0 1,620

129 Fiji 5.6 27.14 42.91 70 20 3,072 9.0 5,860

130 Argentina 5.6 57.31 70 20 1,400 12,370

131 Bolivia (Plurinational State of) 5.6 15.63 31.30 70 20 500 16.0 3,370

132 Botswana 5.6 35.98 68.71 70 20 500 12.0 7,750

133 Palestine 5.6 17.43 25.07 70 20 2,500 16.0 3,710

134 Cambodia 5.9 6.75 16.52 70 20 700 10.0 1,380

135 Mauritania 6.2 6.17 17.43 120 20 2,048 18.0 1,190

136 Samoa 6.2 21.72 29.84 70 20 12,288 15.0 4,190

137 Timor-Leste 6.3 9.60 14.93 700 700 856 5.0 1,820

138 Sierra Leone 6.4 2.65 6.90 70 20 585 15.0 500

139 Belize 6.4 25.00 90 Unlimited 5,400 12.5 4,720

140 Tajikistan 6.5 5.46 100 100 1,600 23.0 1,010

141 Ethiopia 6.6 4.34 12.76 166 20 500 15.0 790

142 Guinea 7.2 4.97 9.82 70 60 1,200 18.0 830

143 Cameroon 7.5 9.00 21.54 278 500 500 0.0 1,440

144 Côte d'Ivoire 7.5 10.08 24.64 560 560 2,240 18.0 1,610

145 Tanzania 7.8 6.63 17.79 135 1,000 600 32.5 1,020

146 Nicaragua 9.0 15.31 41.20 120 200 2,000 15.0 2,030

Measuring Digital Development: ICT Price Trends 2019

17

Rank Economy

as % of

GNI p.c.

USD PPP$

Monthly

voice call

allowance

(in minutes)

Monthly

SMS

allowance

Monthly

data

allowance

(in MB)

Tax rate

included

(%)

GNI p.c.,

USD, 2018

147 Zambia 9.1 10.84 27.64 70 20 1,536 33.5 1,430

148 Rwanda 9.6 6.26 17.19 70 20 1,024 28.0 780

149 Cabo Verde 9.6 27.73 58.11 70 20 1,000 15.0 3,450

150 Benin 10.4 7.54 19.38 84 20 500 18.0 870

151 Honduras 10.4 20.26 39.74 1,200 20 3,200 15.0 2,330

152 Lesotho 10.5 12.04 32.58 248 20 750 9.0 1,380

153 Micronesia 10.6 31.50 32.23 70 900 2,048 0.0 3,580

154 Guatemala 10.9 40.03 66.86 70 20 2,500 12.0 4,410

155 Madagascar 11.4 4.20 14.70 1,680 560 560 20.0 440

156 Kiribati 11.5 30.04 70 20 2,800 0.0 3,140

157 Vanuatu 11.6 28.68 26.92 70 20 2,560 15.0 2,970

158 Djibouti 12.4 22.51 39.72 240 100 500 10.0 2,180

159 Gambia 12.5 7.29 23.52 70 20 750 21.3 700

160 Afghanistan 13.5 6.17 21.01 70 20 1,024 0.0 550

161 Haiti 13.8 9.20 19.68 70 20 1,600 10.0 800

162 Yemen 14.5 11.63 300 100 500 5.0 960

163 Comoros 15.3 16.80 420 350 700 0.0 1,320

164 Papua New Guinea 19.2 40.56 49.26 70 20 2,400 10.0 2,530

165 Mali 20.4 14.14 36.06 70 20 500 18.0 830

166 Burkina Faso 20.9 11.52 29.99 480 480 500 18.0 660

167 Solomon Islands 22.6 37.64 38.80 70 20 3,276 10.0 2,000

168 Mozambique 22.6 8.29 1,750 500 500 17.0 440

169 Togo 24.9 13.50 33.18 285 237 1,050 18.0 650

170 Senegal 25.3 29.73 72.17 1,400 Unlimited 4,200 23.0 1,410

171 Uganda 26.0 13.42 40.15 900 1,000 1,024 18.0 620

172 Guinea-Bissau 26.3 16.47 37.79 70 20 600 17.0 750

173 Malawi 35.2 10.57 31.16 70 20 600 26.5 360

174 Chad 38.7 21.59 1,000 1,000 1,024 18.0 670

175 Burundi 38.8 9.06 22.12 70 60 500 2.0 280

176 Central African Rep. 48.1 19.25 70 20 1,800 19.0 480

177 Dem. Rep. of the Congo 49.0 20.00 120 25 600 26.0 490

178 Niger 56.8 17.99 44.81 2,500 Unlimited 4,096 22.6 380

179 Liberia 60.0 30.00 28.68 9,000 600 18,432 14.0 600

Andorra** 18.52 200 100 500

Anguilla** 37.03 1,000 1,000 1,024 7.0

Cayman Islands** 56.88 300 20 600

Cuba** 23.70 70 20 600

Gibraltar** 30.69 70 100 500 0.0

Liechtenstein** 29.76 70 Unlimited 1,024 7.7

Monaco** 59.04 Unlimited Unlimited 51,200 20.0

Saint Kitts and Nevis** 37.04 1,000 1,000 10,000 18,640

Saint Lucia** 32.78 Unlimited Unlimited 8,000 9,460

Saint Vincent and the Grenadines** 31.70 500 20 3,072 7,940

Somalia** 8.70 70 20 2,000 10.0

Syrian Arab Republic** 13.04 70 25 600 5.0

Taiwan, Province of China** 20.52 70 20 1,024 5.0

Note: Palestine is not an ITU Member State; the status of Palestine in ITU is the subject of Resolution 99 (Rev. Dubai,

2018) of the ITU Plenipotentiary Conference. * Data correspond to the GNI p.c. in 2017. ** Country not ranked because

data on GNI p.c. are not available.

Source: ITU. GNI p.c. and PPP$ conversion factors are from the World Bank. USD exchange rates are from the IMF or UN.

18

Measuring Digital Development: ICT Price Trends 2019

Mobile-voice basket

This section analyses the prices for a basket combining voice and text messages, but without a data

allowance. The revised basket for mobile-voice prices corresponds to the non-data part of a low-

consumption data-and-voice basket, i.e. 70 voice minutes and 20 SMSs.

9

The previous mobile-voice

basket, applied until 2017, contained 30 calls and 100 SMSs.

Global trends

Between 2008 and 2019, the global average price of a mobile-voice basket decreased from USD

21.4 to USD 11.8, equivalent to a CAGR of -5.3 per cent. Growth rates for the period 2008-2019

should be analysed with caution, as there is a break in series between 2017 and 2018. Since the

growth rates for 2009-2017 are very similar to the growth rates for 2008-2019, it is assumed that the

impact of the change in basket is minimal, and growth rates are therefore reported nevertheless.

Over the same period, mobile-voice penetration increased from 60 to 109 subscriptions per 100

inhabitants, a CAGR of 5.5 per cent.

Chart 4: Global mobile-voice price basket in USD (left axis) and mobile-voice

subscriptions per 100 inhabitants (right axis), 2008-2019

25

50

75

100

125

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Subscriptionsper100inhabitants

USD

Mobile‐cellularprice Mobile‐cellulartelephonesubscriptions

Note: Prices are calculated based on simple averages of data from 138 economies for which data on mobile-voice

prices were available for 2008-2019. There is a break in series between 2017 and 2018. Up to 2017, data are for a

basket of 30 calls and 100 SMSs.

Source: ITU. USD exchange rates are from the IMF or UN.

Measuring Digital Development: ICT Price Trends 2019

19

Converted to USD, the average price of the mobile-voice basket in LDCs, at USD 8, was USD

3 cheaper than the average price in developing countries and only half the price in developed

countries. The CIS region had the lowest prices, at only USD 3, whereas the most expensive baskets

were found in the Americas (USD 17) and Europe (USD 15).

Chart 5: Mobile-voice basket in USD, 2019

9

7

9

3

15

17

12

16

11

8

0

2

4

6

8

10

12

14

16

18

20

USD

Note: Simple averages. Based on 195 economies for which data on mobile-voice prices in USD are available for the

year 2019.

Source: ITU. USD exchange rates are from the IMF or UN.

20

Measuring Digital Development: ICT Price Trends 2019

Taking purchasing power into account, the mobile-voice basket fell from PPP$ 30.6 to PPP$ 18.7

between 2008 and 2019, a CAGR of -4.4 per cent, compared with a CAGR of 5.5 per cent for the

number of subscriptions.