1

The Role of Price Tiers in Advance Purchasing of Event Tickets

Wendy W. Moe

Associate Professor of Marketing

Robert H. Smith School of Business

University of Maryland

3469 Van Munching Hall

College Park, MD 20742

301.405.9187

[email protected]d.edu

Peter S. Fader

Frances and Pei-Yuan Chia Professor

The Wharton School

University of Pennsylvania

700 Huntsman Hall

3730 Walnut Street

Philadelphia, PA 19104

215.898.1132

January 2008

The authors would like to thank the anonymous company mentioned in this paper for providing the data and for

many insightful discussions surrounding the issues tackled in this paper. The authors would also like to thank Peggy

Tseng for assisting with the preliminary data analysis.

2

The Role of Price Tiers in Advance Purchasing of Event Tickets

ABSTRACT

Advance purchasing is common in several product markets (e.g., concerts, air travel, etc.) but has

generally been understudied in the marketing literature. Research to date has focused primarily

on the analytical modeling of optimal pricing policies. Our work complements this literature by

focusing on the empirical modeling of advance purchasing and the effects of price on consumer

purchasing behavior. Since pricing strategies in practice are typically more complex than simply

setting a single price point, we consider multiple aspects of price: (1) the existence and use of

multiple price tiers (generally based on seat quality), (2) the face value of each ticket, and (3)

discounts that result in week-to-week variations in price. We show that failure to account for

price tiers can lead to exaggerated inferences about the role of price over time. To sort out these

effects, we develop a tier-specific Weibull timing model to describe sales arrivals for event

tickets in the advance selling period, using a proportional hazards framework for the time-

varying covariates. Additionally, we include a component that captures the role of similar

covariates to explain spot market purchasing. Our empirical findings reflect substantial

differences across tiers. Purchasers in the high-priced tier tend to buy earlier in the selling period

and are influenced by price discounts/premiums in the spot market. Purchasers in the low- and

mid-priced tiers tend to delay purchasing and are influenced only by face value prices in the spot

market. Advance purchasers are not influenced by any aspect of price (after accounting for

differences across price-tiers), and this holds true across all price tiers for our dataset of 22

family events. We discuss the implications of these empirical observations for future modelers.

3

The Role of Price Tiers in Advance Purchasing of Event Tickets

In recent years, advance purchasing behavior has attracted increased attention from both

marketing managers and academics. In the technology and entertainment industries, for

example, marketers have been focusing more efforts on announcing and taking orders for

products well before they are actually available for consumption (Knowledge @ Wharton 2007).

These advance orders can provide marketers with actionable information pertaining to overall

demand, the diffusion process across customers, and customer responsiveness to marketing

efforts (e.g., Moe and Fader 2002).

Recent theoretical research in marketing has studied a number of market environments in

which advance purchasing is common (e.g., concerts, air travel, etc.) and has delineated key

differences among these markets. Desiraju and Shugan (1999) differentiate among advance

purchasing markets based on demand characteristics such as the nature of purchase arrivals and

consumer price sensitivity, two characteristics they analytically show to drive optimal pricing

policies. Other studies (Xie and Shugan 2001, Shugan and Xie 2000) have examined the role of

marginal costs and capacity constraints when determining optimal advance pricing policies.

A substantial amount of research on advance purchase markets can also be found in the

yield management literature, particularly with respect to airline revenue management, where

dynamic pricing policies are designed to maximize revenues given capacity constraints. Many of

these studies examine these dynamic pricing policies as a means to price discriminate between

high and low valuation customers (e.g., Biyalogorsky et al 1999, Borenstein and Winston 1990,

Dana 1998). A key behavioral assumption underlying these policy decisions is that low

valuation customers purchase earlier while high valuation customers purchase later.

4

In this paper, we take a different perspective in studying pricing in advance markets.

Rather than focusing on the optimal pricing policy that would arise from a set of behavioral

assumptions, we empirically examine customer purchasing and the role of price in these markets

and identify regularities in behavior, particularly as they pertain to the purchase timing and

nature of sales arrivals. Without a clear understanding of the underlying customer behavior, the

potential benefits of optimal pricing models may be limited. While our findings may have

significant policy implications for practice, our objective is not to propose an optimal pricing

policy or to provide a forecasting tool. Instead, our objective is to empirically study how

customers respond to various aspects of price in the advance purchase market.

Price has several dimensions in many advance markets. The first is the existence of price

tiers, i.e., the variety of prices that are typically offered at any given time. For example, tickets

for a given event may vary dramatically in price depending on the quality of the seats. As a

result, each price tier tends to attract a different segment of buyer, unique in its valuation for the

performance, purchase timing and price responsiveness over time. The second is the ticket’s

face value, which is set in advance for a given tier of tickets and remains unchanged throughout

the duration of the selling period. Finally, we model the effects of price discounting, a common

practice that leads to week-to-week variations in price.

We focus on the advance market for arena events. Like in the airline industry, event

tickets are generally available for purchase months before the actual performance takes place.

Also like in the airline industry, different price tiers for the same performance (or flight) exist.

However, the two industries differ substantially in other ways. First is how they identify price

tiers. In the airline industry, the allocation of price tiers within a flight (at least among coach-

class seats) is largely arbitrary and at the discretion of the airline. Additionally, these price tiers

5

have limited quality differences and are differentiated primarily by the time of purchase. In

contrast, event tickets have clearly distinguishable price tiers that are closely associated with

seating quality (e.g., distance from the stage). As such, the allocation of price tiers is not a

discretionary decision but rather one that is obviously related to the layout of the venue in ways

that virtually every customer would acknowledge and agree upon. Additionally, dynamic ticket

pricing is not a common practice among box offices and major ticket distributors. As a result,

price discrimination occurs primarily when the consumers choose their price tiers or use discount

codes; it is rarely the result of strategic week-to-week price changes instituted by the seller.

One relevant empirical paper that moves away from the airline setting is Leslie (2004),

who examined price discrimination in Broadway theater tickets through the use of price tiers and

couponing. The focus of his research was on the buyer’s price sensitivity and choice of tier.

When and what a consumer purchased depended on the ticket price, transaction costs and

capacity constraints. While Leslie (2004) examined the consumer’s choice of price tiers and

response to price discounting, he did not address any differences in purchase timing among the

available tiers (which reflect differences between low versus high valuation customers) aside

from the effects resulting from capacity constraints.

Despite the frequent focus on capacity constraints in many of these papers, surprisingly

few events actually bump into such constraints. While the press tends to highlight the sold-out

Hannah Montana concert or playoff basketball games, most arena performances (primarily

concerts, sporting activities, and family shows) take place with excess capacity. Even in Leslie’s

(2004) study of Broadway shows, only 12 of the 199 performances in their dataset were sold-out

shows – and those are held in theaters with far smaller capacity than most arenas. In our data set,

not a single performance sold out its capacity, either for the entire venue or for specific price

6

tiers. Therefore, in this paper, we examine advance purchase behavior in the absence of capacity

constraints – and we are quite comfortable generalizing from the observations we make here

We develop a Weibull timing model of purchasing for each tier that describes both the

purchase timing decision of buyers in that price tier as well as measuring their responsiveness to

various dimensions of price through the use of time-varying (and tier-specific) price-related

covariates. We also incorporate into the model a measure of spot market size. In this component

of the model, we allow the pricing schedule employed in the advance selling period to affect the

relative size of the spot market.

While previous research has modeled the nature of sales arrivals in advance markets

using stochastic models, they have done so at the aggregate performance level rather than at the

price-tier level (see McGill and van Ryzin 1999 for a review). By examining sales arrivals for

specific price tiers, we can empirically examine and compare the behaviors of buyers with

different valuations for the performance.

Our findings show that advance purchasing behavior tends to vary dramatically across

different price tiers even within a single performance. We examine a highly varied set of events

and find consistent results across them. While buying behavior varies across price tiers, buyers

are virtually unaffected by the face value price or week-to-week price variations in the advance

selling period. The only element of price that is important to these buyers is the price tier. Spot-

market buyers, on the other hand, are influenced both by face values (in the low- and mid-priced

tiers) and the spot-market price relative to the advance price (in the high-priced tier). Overall,

however, the largest source of variation in behavior arises from the differences across price tiers

rather than any pricing strategy within tier. This is a significant finding that we hope will

contribute to the extant literature as well as to how event marketers think about pricing.

7

The Role of Price Tiers in the Market for Event Tickets

Our Sample

Our analysis focuses on a sample of 22 performances of “family” events (e.g., circus,

children’s concerts, etc.). The 22 performances in our sample are held in a variety of locations

ranging from major markets such as New York and Los Angeles to smaller markets such as

Wheeling, WV, and Laredo, TX. As a result, sales and prices vary substantially across events.

The events all took place between January and June 2004, but ticket sales began far earlier with

events experiencing as many as 18 weeks of tickets sales leading up to the performance date.

Table 1 provides some descriptive information for each of the 22 performances in our sample.

The data were provided to us by a leading nationwide ticketing agency, which at the time

served as the dominant distribution channel for the vast majority of tickets at all events. Small

numbers of tickets can be held back by the venue, the event promoter, and other local entities.

But these tickets are not sold in a conventional manner (e.g., they are used for local radio station

giveaways), so there is little “leakage” of these tickets into the general population of buyers.

Thus our dataset provides a fairly accurate and complete representation of the sales patterns for

every event. (Our data period precedes the prominent role of now-popular resellers such as

StubHub.)

8

Table 1. Descriptive Information for Event Performances

Total Range of Selling

Event Location Month Sales Prices Paid Weeks

1. New York, NY April 2004 12252 $5.00 - $169.95 18

2. New York, NY March 2004 9929 $5.00 - $169.95 16

3. San Diego, CA February 2004 8247 $7.00 - $56.30 10

4. Atlanta, GA February 2004 7979 $5.00 - $101.35 15

5. Albany, NY April 2004 7713 $5.50 - $37.15 17

6. Phoenix, AZ June 2004 7198 $2.50 - $79.75 10

7. Los Angeles, CA January 2004 6695 $5.00 - $56.30 11

8. Nashville, TN January 2004 6336 $5.75 - $43.25 10

9. Raleigh, NC February 2004 6274 $10.00 - $42.80 8

10. Kansas City, MO March 2004 6160 $9.50 - $48.90 9

11. San Antonio, TX June 2004 6048 $5.00 - $40.05 10

12. Sacramento, CA February 2004 5891 $10.00 - $55.00 13

13. Phoenix, AZ January 2004 5405 $2.50 - $58.90 13

14. Miami, FL April 2004 5036 $8.50 - $58.00 12

15. Laredo, TX May 2004 4845 $8.25 - $44.50 7

16. Miami, FL January 2004 2866 $2.50 - $41.70 9

17. New Orleans, LA May 2004 2746 $10.50 - $40.50 8

18. Jacksonville, FL April 2004 1950 $10.00 - $54.25 10

19. Wheeling, WV March 2004 1720 $5.00 - $23.55 6

20. Atlantic City, NJ May 2004 1548 $6.50 - $66.00 10

21. Madison, WI May 2004 561 $6.00 - $33.25 5

22. Miami, FL March 2004 428 $1.50 - $58.00 11

The price of a ticket has several dimensions in our data. First is the face value of each

ticket. The face value is the full price of that ticket prior to any service charges or facilities fees

that may be imposed. The face value is set well in advance of the selling period and is fixed for

the duration of the selling period. However, this is not to say that consumers face unchanging

prices over time. Instead, discounts are common and vary from week to week. The price paid

by each buyer is the face value plus any service/facilities charges and less any price discount

available that week and claimed by the buyer. Because the available discounts vary from week

to week, the average price paid also changes from week to week. Therefore, the second

dimension of price that we consider is the week-to-week variation in price. We will discuss

measures of this aspect of price later when we develop our model. The final facet of price is the

9

price tier. For each performance, there are a variety of tickets with different face values and/or

seating locations that are defined by the layout of the venue. The number of ticket categories

varies across events. While some had as few as three ticket categories, others had as many as

nine. In many cases, multiple categories shared the same face value but were divided into two

separate categories to reflect the seating location. In these cases, we collapsed the two categories

into one.

To allow for comparability across performances, we grouped ticket categories into three

tiers: high-priced, mid-priced and low-priced. Two separate coders independently viewed the

floor plans of the venues along with the face-value prices and seating locations of those tickets

available for sale. Based on the distribution of ticket prices and seating locations, ticket

categories were assigned to one of the three price tiers. The task was surprisingly straight-

forward since the face value prices of tickets tended to cluster together.

One final issue that we need to address is that of capacity utilization. As noted earlier,

while the perception may be that capacity limitations pose frequent and pressing constraints in

this industry, this is rarely the case. The more common events, such as gymnastics competitions,

skating shows, circuses, rodeos or even concerts by less popular artists, are less salient than the

sold-out rock concerts that tend to be the focus of news stories and conversations. In our

conversations with two separate firms (i.e., our data provider and another nationwide ticketing

company), we were told that capacity is rarely an issue for a given performance. With the

exception of a handful of popular concerts, venue sizes far exceed demand for most events.

Table 2 summarizes the capacity utilization across the performances in our data. These measures

show that capacity constraints are non-binding in our data and therefore should not be the driving

force behind the purchasing behavior we model

10

Table 2. Capacity Utilization*

High-Priced Tier Mid-Priced Tier Low-Priced Tier

Minimum 22.0% 6.3% 2.9%

25

th

percentile 81.7% 58.0% 20.8%

Median 88.8% 83.5% 31.6%

75% percentile 91.7% 95.7% 64.3%

Maximum 99.7% 98.6% 97.3%

* Percentages are the percent of tickets available for sale that are actually sold. This measure excludes all

those tickets that are held back for special promotions.

Aggregate Sales and Pricing Patterns

To illustrate the typical sales and pricing patterns observed, consider two different events

that took place in Miami, FL. Figure 1 plots the overall sales and prices (aggregated across price

tiers) for each advance selling week, t.

Figure 1: Overall Sales and Pricing Patterns

Overall Sales and Price

Miami (January Event)

0

500

1000

1500

2000

2500

1234567Event

Week

Selling Week

Sales

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

Price

sales average price

Overall Sales and Price

Miami (April Event)

0

500

1000

1500

2000

2500

1 2 3 4 5 6 7 Event

Week

Selling Week

Sales

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

Price

sales average price

In both cases, peak sales occur in the performance week. In the advance weeks, sales start

relatively low and gradually build as the performance approaches. In contrast, average price paid

in the advance weeks starts high and gradually declines as the performance week approaches.

These aggregate sales and price patterns are similar across events and are consistent with the

11

analytical findings of Desiraju and Shugan (1999) relating optimal pricing policies to the nature

of sales arrivals.

Difference across Price Tiers

At first glance, the downward sloping price curve seems to suggest that the ticket seller is

employing a deliberate pricing policy of decreasing price as the performance nears. However,

upon further investigation, this trend is primarily an artifact of aggregating across price tiers.

Figure 2 plots the percent of sales attributable to each price tier and shows that tickets in the

high-priced tier tend to sell disproportionately in the early weeks of the advance selling period

while tickets in the low-priced tier tend to sell more as the performance approaches. When these

differences across price tiers are ignored and aggregated to provide an overall average price paid,

the result is what appears to be a schedule of decreasing prices over time.

Figure 2. Percent of Weekly Sales by Price Tier

Percent of Weekly Sales by Tier

Miami (January Event)

0%

10%

20%

30%

40%

50%

60%

70%

80%

1234567Event

Week

Selling Week

% of Weekly Sales

Low -Priced Tier Mid-Priced Tier High-Priced Tie

r

Percent of Weekly Sales by Tier

Miami (April Event)

0%

10%

20%

30%

40%

50%

60%

70%

80%

1234567Event

Week

Selling Week

% of Weekly Sales

Low -Priced Tier Mid-Priced Tier High-Priced Tie

r

The same phenomenon can be observed across the remaining events in our data set.

Figure 3 shows the percent of all sales that occur in the early selling period (i.e., all weeks prior

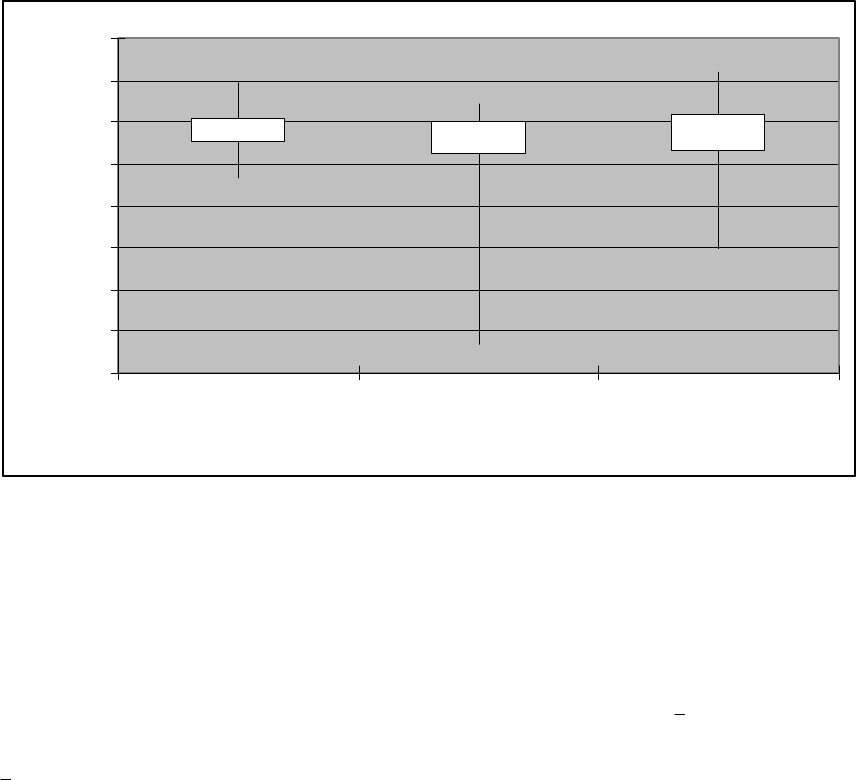

to the final month of sales) and provides an overview of how this measure varies across events

12

for each tier. The boxes represent the events in the interquartile range (i.e., the middle 50

th

percentile), while the lines indicate the full range of observed values. It is quite evident that only

a small percentage of the low-priced tickets sell in the early weeks of the advance selling period.

In contrast a significant percentage of high-priced tickets sell in the first four weeks. This

pattern is similar to that described above where the proportion of ticket sales in the high-priced

tier tend to decrease as the performance approaches while the opposite is true in the low-priced

tier. These sales patterns highlight the potential pitfalls of ignoring price tiers and conducting

aggregate level research, as many of the dynamics within price tiers are masked in aggregation.

They also highlight one of the key differences, discussed earlier, between demand patterns for

events compared to airlines and other industries that rely upon traditional notions of yield

management.

Figure 3. Summary of Sales Timing by Tier

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Low-Priced Tier Mid-Priced Tier High-Priced Tier

Percent Early Sales

13

Pricing over Time

In addition to the price differences across tiers, week-to-week price variations also exist

within tiers. However, these variations are not as dramatic and systematic as the price plots in

Figure 1 might suggest. For some events and tiers, prices do decline as the performance

approaches. However, there are also several instances where an increasing price pattern is

observed. In fact, pricing patterns differ even across the two Miami events used in our example.

In Figure 4, the average price in each tier is charted over time for the same two events presented

in Figure 2. For ease of presentation, the selling period is divided into three stages. The spot

period represents the week of the performance. The late period represents the month prior to the

performance (excluding the spot period), and the early period represents all weeks prior to the

final month of sales. Since face values are set before the tickets are made available for sales and

remain unchanged throughout the selling period, any variation seen in prices over time are due

largely to price discounting. For the January event, tier-specific prices remain quite stable over

time, a fact that is lost in the aggregate event-level data (Figure 1). The April event, on the other

hand, exhibits slightly more price variation over time. Specifically, tickets in the low- and the

mid-priced tiers tend to get less expensive as the performance approaches. Ticket prices for the

high-priced tier indicate a more irregular pricing pattern. But these within-tier variations are still

quite modest compared to the aggregate patterns shown in Figure 1.

In this section, we have shown that aggregate performance-level trends in sales and

pricing often masks the more complex dynamics that occur due to the existence of price tiers.

Therefore, in the next section, we model ticket sales at the tier level. We hope to complement

the existing research that relates optimal pricing policies to buyer behavior by empirically

modeling and highlighting differences in behavior across tiers.

14

Figure 4. Average Price Paid by Tier

Average Price by Tier

Miami (January Event)

$-

$10.00

$20.00

$30.00

$40.00

$50.00

Low -Priced Tier Mid-Priced Tier High-Priced Tier

Price

Ea r l y Late Spot

Average Price by Tier

Miami (April Event)

$-

$10.00

$20.00

$30.00

$40.00

$50.00

Low-Priced Tier Mid-Priced Tier High-Priced Tier

Price

Ea r l y Late Spot

Model Development

Our proposed model has several important characteristics which we will develop in turn.

First, it explicitly models sales of tickets in each price tier. Second, it differentiates between the

advance selling market and the spot market. Finally, we capture the effects of face value and

week-to-week variations in price and measure their impact on the advance market as well as the

spot market.

The Advance Market

We start by modeling the timing of sales arrivals for each tier as a Weibull process. This

process governs when buyers in the advance market purchase their tickets. This may be as early

as several months prior to the performance or as late as a few days before the performance. We

choose the Weibull for its flexibility in accommodating a variety of shapes that are consistent

with what we see empirically in our data. The associated hazard function

)|( jth

i

, survival

15

function )|( jtS

i

and cumulative distribution function )|( jtF

i

for each event i and tier j are as

follows:

1

)|(

−

=

ij

c

ijiji

tcjth

λ

ij

c

t

ij

jt

i

h

i

eejtS

λ

−

∫

−

==

)|(

)|(

ij

c

t

ij

ii

ejtSjtF

λ

−

−=−= 1)|(1)|(

where t = advance selling week

λ

ij

= slope parameter for event i purchases in tier j (

λ

ij

> 0)

c

ij

= shape parameter for event i purchases in tier j (c

ij

> 0)

Modeling ticket sales is different from most other purchasing contexts in that all

purchases must be made by a predetermined time – the time of the performance. However, if

purchase timing were modeled to strictly follow a Weibull timing process, ticket sales could

theoretically extend beyond the performance date. Since the occurrence of the performance

effectively right censors the selling period, buyers who would have preferred to delay purchase

are forced to purchase at or before the time of the performance. To accommodate this, we

assume that the remainder of the cdf at the time of the performance is compressed and

materializes at the last minute.

(1)

ij

c

t

ij

ii

ejtSjtF

λ

−

−=−= 1)|(1)|( if t < T

1)|(

=

jtF

i

if t = T

where T is the time of the performance.

16

The Spot Market

In addition to the advance-purchase market, there is also a substantial spot market that is

not fully captured by the model developed thus far. Therefore, we model the large number of

buyers who buy in the spot market by inflating the probability of purchase at t = T (i.e., the

performance week) in the same way that a zero-inflated Poisson inflates the probability at zero.

After accommodating both the spot market buyers and the discrete-time nature of our observed

data (i.e., weekly counts), we can write the probability of observing a tier j ticket purchase at

time t as:

(2)

[

]

)|1()|()1()|( jtFjtFIjtP

iiijtiji

−

−

⋅

−

+

=

φ

φ

where I

t

= 1 for t = T (I

t

= 0, otherwise),

φ

ij

represents the proportion of sales from strictly spot

buyers and

)|( jtF

i

is defined above in equation (1). Since the size of the spot market can be

influenced by the pricing policy, we will further define

φ

ij

in the next section.

The Role of Price

Our objective in this paper is to better understand the role of price in an advance market

1

.

This objective is partly satisfied by modeling the differences between price tiers as we have done

above. However, two other aspects of price remain: face value and week-to-week variations due

to discounting.

Sales in the advance market are modeled as a Weibull timing process. Incorporating

covariates in a Weibull hazard model is a relatively straightforward process. The first covariate

1

One potential concern is that pricing (i.e., discounting) strategies may not be independent of the expected market

response to price. Therefore, we also tested a model that treats price as non-random. Specifically, we followed the

approach taken by Manchanda, Rossi, and Allenby (2004) and simultaneously modeled price as a function of the

expected effect of price and expected baseline sales. None of these factors have a significant effect on price.

Therefore, for the remainder of the paper, we focus only on the model which treats price variations as exogenous

and random.

17

effect we consider is the effect of face value. Because there are some slight variations in face

value within a given price tier, we calculate the average face value (AFV) for each performance-

tier combination. This value is unchanged over time within a given performance-tier and

captures the primary impact of price level on advance buying behavior. The second covariate

effect we consider is that of week-to-week variations in price. The proportional hazards

framework allows us to easily incorporate time-varying covariates and provides coefficients that

reflect the effect of week-to-week changes in the covariates. However, the coefficients reflect

the overall level of the covariates as well. Therefore, to separate the effect of week-to-week

variations in price from the effect of overall price level, we use the average percentage discount

(DISCOUNT) instead of average price paid as a time-varying covariate. We also include the

number of advance selling weeks (PREWK) and seasonality variables (THANKS and XMAS) as

control covariates. We include all of these covariates through the Weibull hazard function as

follows:

{}

ijtij

Xβexp)|(

1−

=

ij

c

ijiji

tcjth

λ

where

X

ijt

is a vector of covariates that includes:

THANKS

it

= an indicator variable for the week before Thanksgiving

XMAS

it

= an indicator variable for the week before Christmas

PREWK

i

= number of advance selling weeks

AFV

ij

= average face value of tickets sold in tier j for performance i

DISCOUNT

ijt

= the average percentage discount for a tier j ticket for performance i at

week t

Using standard proportional hazard methods, we fine-tune the cdfs shown in equations

(1) and (2) to incorporate these covariates as follows.

⎭

⎬

⎫

⎩

⎨

⎧

∑

⎟

⎠

⎞

⎜

⎝

⎛

⋅−−−−=

=

t

u

ij

c

ij

c

iji

euujtF

1

])1([exp1)|(

iju

X

ij

β

λ

, if t < T

18

Our modeling objective in the spot market is the same as that in the advance market: to

capture the effects of face value as well as week-to-week price variations in the weeks leading up

to the performance. To model the effect of face value, we again use the average face value

(AFV) as a covariate. However, to capture the effect of week-to-week variations in price, we

need to consider a new measure that compares the spot market price to earlier prices. As a time-

varying covariate in the advance-selling period, the DISCOUNT covariate reflects the effect of

week-to-week changes in price as well as the size of the discount. However, as a covariate for

spot market size, the DISCOUNT measure would not provide any comparison to earlier prices.

Therefore, in the spot market component of the model, we use Spot Price Index (SPI) as a

covariate and calculate it for each tier as the average price paid in the spot market (t=T) divided

by the average price paid in the advance market (t<T). If pricing strategies are unchanged

between the advance market and the spot market, we would have SPI=1. An SPI<1 indicates

additional discounting in the spot market. An SPI>1 indicates that spot market tickets are selling

at a premium relative to the tickets sold in earlier weeks.

To incorporate spot market covariates, we define the spot market parameter,

φ

ij

, from

equation (2) as follows:

ij

ij

ij

e

e

θ

θ

φ

+

=

1

where

ijij

Zγ

=

ij

θ

where Z

ij

is a vector of covariates that includes an intercept and the following

2

:

PREWK

i

= number of advance selling weeks

AFV

ij

= average face value

SPI

ij

= spot price index

2

We do not include Thanksgiving or Christmas as covariates since none of the events in our data set have scheduled

performances during those weeks.

19

Heterogeneity across Events

To accommodate heterogeneity across events, we assume that both the slope (

λ

ij

) and

shape (c

ij

) parameters of the Weibull process governing sales within each performance-tier are

drawn from independent normal distributions as follows:

),(~)ln(

),(~)ln(

cjcjij

jjij

Normalc

Normal

σμ

σ

μ

λ

λλ

Additionally, we allow covariate effects to vary across events according to independent

normal distributions:

),(~

kj

s

kj

N

kij

ββ

and ),(~

rjrjrij

sN

γγ

where k indexes the covariates in the Weibull hazard model and r indexes the covariates

(including the intercept) in the spot market component of the model.

To complete the model specification, we choose appropriately diffuse and uninformative

priors for each of our parameters. We estimate this model using WinBUGS and run 20,000

iterations, discarding the first 15,000 for burn-in. Trace plots and Monte Carlo standard errors

were monitored to ensure convergence.

We also estimated a number of benchmark models, including one that allowed for

correlations among parameters and another that did not allow for parameter differences across

tiers. In the correlated model, we found that most correlations were statistically insignificant,

and most of the exceptions were not substantially different from zero (i.e., the largest correlation

was 0.0089). In the “homogeneous-tiers” model, all price tiers shared the same Weibull

parameters and price coefficients. This model performed far worse than the proposed model (as

indicated by the same fit measures described in the next section). Since our objective here is to

focus more on empirical regularities rather than model comparison, per se, we will limit our

20

discussion to the results of the proposed model alone, since it outperforms our benchmarks while

providing an accurate and parsimonious description of buyer behavior in this market.

3

Results

Model Validation

Figure 5 presents tracking plots for the same two events shown in Figure 1. It is clear

that the model fits the data quite well. In fact, because the week-to-week fit is so accurate, it is

difficult to distinguish the actual sales line from the estimated sales line.

Figure 5. Tracking Plots for Miami Events

Model Fit

Miami (January Event)

0

500

1000

1500

2000

2500

1234567Event

Week

Selling Week

Sales

ACTUAL ESTIMA TED

Model Fit

Miami (April Event)

0

500

1000

1500

2000

2500

1234567Event

Week

Selling Week

Sales

ACTUAL ES TIMA TED

To further illustrate the quality of the model, Figure 6 shows the model fit for the same

two events by tier. Again, for ease of presentation purposes, we divide the advance selling

period into early, late and spot periods.

3

Comparison measures between the models are available from the authors.

21

Figure 6. Model Fit by Tier for Miami Events

Model Fit by Tier

Miami (January Event)

0

200

400

600

800

1000

1200

Early Late Spot Early Late Spot Early Late Spot

Low -Priced Tier Mid-Priced Tier High-Priced Tier

Sales

Actual

Est i ma t ed

Model Fit by Tier

Miami (April Event)

0

200

400

600

800

1000

1200

1400

1600

1800

Early Late Spot Early Late Spot Early Late Spot

Low -Priced Tier Mid-Priced Tier High-Priced Tier

Sales

Actual

Estimated

Figures 5 and 6 show that the model provides a very good fit for the two events displayed

despite the earlier discussion that the two events exhibit slightly different sales patterns at the tier

level. For the January event, sales of tickets in the high-price tier increase as the performance

approaches

4

. In contrast, sales of tickets in the high-price tier decrease as the performance

approaches in April. Despite these differences, the model presented in this paper fits both events

very well.

To extend the analysis presented in Figure 6 to the complete set of events, we calculate

RMSE (root mean squared error) as an indicator of model fit and present the results in Table 3.

We use the selling period (i.e., spot, late, and early) as our unit of analysis and then average

across periods as follows:

3

)])([)((

},,{

2

∑

−

=

∈ earlylatespot

ijij

ij

SalesESales

RMSE

τ

ττ

4

While the number of tickets sold in the high-price tier increases as the event approaches, it represents a decreasing

percentage of all tickets sold since sales in the low- and mid-price tiers increase dramatically.

22

Table 3: Model Fit

Low-Priced Mid-Priced High-Priced Overall

RMSE 11.55 72.51 15.49 45.41

RMSE (% of sales) 1.25% 1.69% 2.35% 0.77%

# of performances with RMSE < 2.5% 20 17 16 21

# of performances with RMSE 2.5%-5.0% 1 4 4 1

# of performances with RMSE > 5.0% 1 1 2 0

Overall, the RMSE measures provided in Table 3 show that the model fits the data very well.

The overall fit for all performances, regardless of price tiers, generates an RMSE of 45.41. The

model fit by price tier is just as impressive with RMSE ranging from 11.55 for the low-priced

tier to 72.51 for the mid-priced tier. To better evaluate RMSE, we also provide in Table 3 the

percent of total performance-tier sales the RMSE represents. Given the volume of sales for each

performance-tier, the RMSE reported in Table 3 indicate an excellent fit with overall and tier-

specific errors falling within 2.5% of sales across performances.

Parameter Results: The Advance Market

We begin our discussion of results by examining the baseline Weibull parameters for

each price tier,

λ

j

and c

j

. These parameters represent the underlying purchase timing process

absent of any covariate or spot market effects (see Table 4 for all parameter estimates).

23

Table 4. Parameter Estimates

Low-Priced Mid-Priced High-Priced

Parameter Variable Tier Tier Tier

Baseline Weibull Parameters

μ(λ)

Slope parameter 0.0065 0.043

0.16

[0.0018, 0.029] [0.031, 0.058] [0.10, 0.26]

μ

(c) Shape parameter 4.16 2.94 2.12

[3.31, 5.23] [2.39, 3.63] [1.35, 3.22]

Advance-Market Parameters

THANKS

β

Thanksgiving effect 0.20 1.17 1.79

[-1.30, 1.36] [0.086, 2.08] [-0.33, 3.04]

XMAS

β

Christmas effect 0.69 0.78 0.90

[-1.83, 2.80] [-0.45, 1.97] [-0.75, 2.48]

PREWK

β

# of Adv. Selling Weeks -0.65 -0.33 -0.19

[-0.84, -0.44] [-0.46, -0.19] [-0.34, -0.039]

AFV

β

Average Face Value -0.074 -0.12 0.0069

[-0.19, 0.040] [-0.46, 0.15] [-0.21, 0.21]

DISCOUNT

β

Percent Price Discount 1.97 2.08 -0.59

[-2.31, 6.25] [-0.21, 4.30] [-4.88, 3.79]

Spot Market Parameters

INT

γ

Intercept -0.61 -0.17 2.00

[-5.06, 4.20] [-6.27, 4.96] [0.71, 3.54]

PREWK

γ

# of Adv. Selling Weeks -1.76 -3.05 -0.83

[-4.12, -0.032] [-5.86, -0.29] [-1.37, -0.35]

AFV

γ

Average Face Value -5.03 -3.82 -0.031

[-8.54, -1.89] [-7.31, -0.30] [-0.56, 0.39]

SPI

γ

Spot Market Index -0.25 0.14 -3.17

[-4.56, 4.41] [-4.67, 9.46] [-4.80, -0.65]

* Values in brackets represent the 90% confidence range

* Values in bold indicate parameters that are significant at

p = 0.10

24

Figure 7 plots the theoretical Weibull distributions that result from the parameter

estimates presented in Table 4. These distributions assume steady pricing in the advance selling

weeks and median values for the number of advance selling weeks, AFV, and SPI for each tier.

From this figure, we can see that tickets in the high-priced tier tend to sell earlier. In contrast,

buyers of the mid- or low-priced tickets tend to delay their purchase. This is the underlying

dynamic that results in the perception that prices decline as the performance approaches. This

result is also consistent with Desiraju and Shugan’s (1999) contention that for this class of

products (e.g., concerts, fashion, etc.), buyers who have the greatest value for the service buy

earlier in the advance selling period.

Figure 7. Baseline Weibull Process by Tier

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

12345678910

Selling Week

P(t)

Low-Priced Tier Mid-Priced Tier High-Priced Tier

For the most part, the seasonality covariates for Thanksgiving and Christmas have no

effect on the timing of ticket purchases for any tier of tickets. We see an effect of Thanksgiving

on the mid-priced tier that is marginally significant (the coefficient is significant at p=0.10 but

not at p=0.05). The number of advance selling weeks has a significant and negative effect on the

25

Weibull hazard across all three price-tiers. In other words, the earlier that the tickets are made

available for sale, the more gradual is the pattern of sales arrivals.

Interestingly, the price of the tickets also has no significant impact on sales in the early

market once price tiers are taken into account. Neither the face value nor any price discounting

influences the purchasing decision in the advance market. This suggests that price promotions in

the early market only serve to decrease margins.

Parameter Results: The Spot Market

In contrast to the results for the advance market, several covariates influence the size of

the spot market. The number of advance selling weeks has a significantly negative effect on the

size of the spot market for all three price tiers. In other words, the longer tickets for an event

have been available for sales, the smaller the spot market. This makes intuitive sense since the

longer selling period prior to the scheduled performance provides more opportunities for

consumers to buy early.

Pricing, unlike in the advance market, has a significant effect in the spot market. The

face value of the ticket influences the size of the spot market in the low- and mid-priced tiers

while the spot price (SPI) has an influence on the size of the spot market in the high-priced tier.

Figure 8 summarizes the pricing policies in the spot market across performances for each

of the three price tiers. The figure illustrates that additional price discounting in the final selling

week (SPI<1) is a common practice in all three tiers with the most severe discounting occurring

in the mid-price tier. However, there are also instances of tickets selling at a price premium in

the spot market (SPI>1). In our sample of 22 performances, all of them had one or more price

tiers selling at a price discount in the spot market. Fourteen performances had one or more price

26

tiers selling at a price premium in the spot market. (Perhaps these events had discount coupons

that expired before the performance date, but other fees that continued to apply.)

Figure 8. Summary of Spot-Market Pricing

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

Low-Priced Tier

(median=0.98)

Mid-Priced Tier

(median=0.96)

High-Priced Tier

(median=0.97)

SPI

Despite all the price variability shown in Figure 8, spot-market prices have very little

impact on the relative size of the spot market in the low- and mid-priced tiers. For these two

tiers, the only facet of price that has an impact on purchasing is the ticket’s face value, which

remains unchanged throughout the selling period. The model results (

LOWAFV,

γ

=-5.03,

MIDAFV,

γ

=-3.82) indicate that face value has a significant and negative effect in both the low-

and the mid-priced tiers, suggesting that higher face values encourage consumers to buy in the

advance market rather than in the spot market. This could be because higher prices require a

bigger commitment (and more advance planning) by the consumer. The Spot Price Index (SPI),

however, has no significant effect on the relative size of the spot market in these two tiers. This

result, coupled with the Weibull parameter estimates, indicates that price discounting, and the

27

week-to-week price variations that result, appear to have no impact on ticket buying behavior in

either the advance or the spot market for the low- and mid-priced tiers.

Customer behavior in the high-priced tier presents a sharp contrast to that seen in the

other two tiers. In the high-priced tier, face value has no significant impact on the size of the

spot market while a discounted spot market price can significantly increase the relative size of

the spot market (

HIGHSPI,

γ

=-3.17). This result is consistent with the asymmetric price effects

found by Blattberg and Wisniewski (1988) who showed that price discounts are more effective

when applied to high quality products than when applied to low quality products. In the context

of event tickets, discounting spot market prices for high-priced (and high-quality) tickets expand

the spot market more effectively than if the same discounts were applied to the other tiers.

Summary of Pricing Effects

Overall, there seem to be significant differences in purchasing behavior between price

tiers (see Table 5 for a summary). High-priced tier consumers tend to buy earlier while low- and

mid-priced tier consumers are more likely to delay their purchase.

In addition to difference across tiers, the prices themselves also have effects that vary

across tiers. While none of the pricing covariates have an impact on when tickets are purchased

in the advance market, we do see significant effects in the spot market. While the face value of

the tickets affects the spot market for the low- and mid-priced tiers, the spot price

premium/discount (SPI) is what influences buying behavior in the high-priced tier. Overall, it

appears to be difficult to influence sales in the low- and mid-priced tiers once a face value has

been set. Sales of tickets in the high-priced tier can, however, be influenced by discounting in

28

the spot market, but this has a limited impact due to the smaller number of consumers in this tier,

particularly as the performance gets closer..

Table 5. Summary of Pricing Effects

Low-Priced Tier Mid-Priced Tier High-Priced Tier

Advance Market Effects

Higher Face Values -- -- --

Larger Price Discounts -- -- --

Spot Market Effects

Higher Face Values smaller spot mkt smaller spot mkt --

Spot Market Discounts -- -- larger spot mkt

CONCLUSIONS AND DISCUSSION

In this paper, we model the effects of pricing on advance purchases of event tickets. Our

findings show that there are significant differences in buying behavior across price tiers, even

within a given performance. In fact, the differences across price tiers are far greater than any

variation within tier. Overall, buyers of high-priced tickets tend to purchase earlier in the selling

period than buyers of low- and mid-priced tickets. This is in contrast to the airline industry

where high-value customers tend to arrive later than low-value customers. One possible

explanation for this pattern of behavior is that high-value customers purchase earlier in the

selling period to avoid capacity constraints (Desiraju and Shugan 1999, Leslie 2004). However,

we examined an environment where capacity tends not to be a constraint. An alternative

explanation is that high-value customers are less sensitive to scheduling uncertainty and have

lower relative costs associated with committing to a future event. The idea that customers have

different costs of commitment is one that has been raised in previous research (Desiraju and

29

Shugan 1999) but not fully explored. Our findings suggest that this would be an important issue

to study further.

Not only do the expected purchase times vary across tiers, but consumer response to face

value prices and week-to-week variations in price also differ across tiers. With the exception of

spot-price discounting in the high-priced tier, event marketers have little ability to influence sales

with price once face values are set and tickets are made available for sale. In the spot market for

tickets in the high-priced tier, spot-price discounting can increase the number of buyers in the

spot market. The same effect is not seen in the other tiers.

Overall, advance purchasing continues to be a promising area of research in marketing.

In addition to the purchase timing and pricing issues discussed in this paper, several significant

opportunities remain for future research. In this paper, we examined only a sample of events and

treated each independently. However, event marketers often face the decision of scheduling a

series of performances in a given market rather than just offering one performance. This

schedule of performances has an impact on the advance-selling market that we do not yet

understand. Likewise, there is often a broader marketing campaign surrounding this schedule

(i.e., beyond price tactics alone) that has generally been overlooked as well. Overall, the advance

purchasing environment is rich with research questions that can provide a significant impact on

how event managers and ticket sellers make decisions, yet only a few of these questions have

been addressed in this paper and previous ones.

30

References

Biyalogorsky, E., Carmon, Z., Fruchter, G., and Gerstner, E. (1999), “Overselling and

Opportunistic Cancellations,” Marketing Science, (18), pp. 605–610.

Blattberg, Robert C. and Kenneth J. Wisniewski (1988), “Priced-Induced Patterns of

Competition,” Marketing Science, 8 (4), 291-309.

Borenstein, S., and Rose, L.R. (1994), “Competition and Price Dispersion in the U.S. Airline

Industry,” Journal of Political Economy, (102), pp. 653–683.

Cachon, Gerard P. (2004), “The Allocation of Inventory Risk in a Supply Chain: Push, Pull, and

Advance Purchase Discount,” Management Science, 50 (2), 222-238.

Dana, J.D. (1998), “Advance-Purchase Discounts and Price Discrimination in Competitive

Markets,” Journal of Political Economy, (106), pp. 395–422.

Desiraju, Ramarao and Steven M. Shugan (1999), “Strategic Service Pricing and Yield

Management,” Journal of Marketing, 63 (January), 44-56.

Knowledge @ Wharton (2007), “New Products (Like the iPhone): Announce Early or Go for the

Surprise Rollout?” June 13, http://knowledge.wharton.upenn.edu/article.cfm?articleid=1752.

Leslie, Philip (2004), “Price Discrimination in Broadway Theater,” RAND Journal of

Economics, 35 (3), 520-541.

McCardle, Kevin, Kumar Rajaram and Christopher S. Tang (2004), “Advance Booking Discount

Programs Under Retail Competition,” Management Science, 50 (5), 701-708.

McGill, J.I., and van Ryzin, G.J. (1999), “Revenue Management: Research Overview and

Prospects,” Transportation Science, (33), pp. 233–256.

Moe, Wendy W. and Peter S. Fader (2002), “Using Advance Purchase Orders to Forecast New

Product Sales,” Marketing Science, 21 (3), 347-364.

Shugan, Steven M. and Jinhong Xie (2000), “Advance Selling for Services,” California

Management Review, 46 (3), 37-54.

Tang, Christopher S., Kumar Rajaram, Aydin Alptekinoglu and Jihong Ou (2004), “The Benefits

of Advance Booking Discount Programs: Model and Analysis,” Management Science, 50 (4),

465-478.

Xie, Jinhong and Steven M. Shugan (2001), “Electronic Tickets, Smart Cards, and Online

Prepayments: When and How to Advance Sell,” Marketing Science, 20 (3), 219-243.