HTML Edition

The original hardcover textbook edition (ISBN 0-201-56355-X) of

Object-Oriented System Development by Dennis de Champeaux, Douglas

Lea, and Penelope Faure was published by Addison Wesley, copyright ©

1993 by Hewlett-Packard Company. You can purchase this book directly

from Addison-Wesley by phone at (800)822-6339, or order it through most

bookstores. All parties involved have graciously granted permission to create

this HTML edition, maintained by Doug Lea. Mail comments to

Contents

Preface

1 Overview

Scope; Objects; Development Paradigms; Development Phases; Summary;

Part 1: Analysis

2 Introduction to Analysis

Purpose; Models; Process; Summary;

3 Object Statics

Instances; Classes; Attributes; Attribute Features; Constraints; Identifying Objects and Classes;

Summary;

4 Object Relationships

Relationships; Collections; Identifying Relationships; Summary;

5 Object Dynamics

Describing Behavior; Transition Networks; Examples; Reducing Complexity; Summary;

6 Object Interaction

Transitions; Sending and Receiving Events; Interaction Notations; Examples; Summary;

7 Class Relationships

Property Inheritance; Subclasses; Multiple Inheritance; Sibling Relationships; Set Operations;

Inheritance of Relations; Summary;

8 Instances

Subclasses and Instances; Metaclasses; Parametric Instances ; Summary;

9 Ensembles

Ensembles; Other Decomposition Constructs; Ensembles as Systems; Summary;

10 Constructing a System Model

Requirements Fragment; Use Cases; Subsystems; Vocabulary; Classes; Ensembles; Model;

Summary;

11 Other Requirements

Resources; Timing; Other Constraints; Summary;

12 The Analysis Process

Software Development Process; Default Sequence of Steps; OO Analysis of the OO Analysis

Process; Alternative Processes; Tools; Summary;

13 Domain Analysis

Models; Reuse; Summary;

14 The Grady Experience

Part II: Design

15 From Analysis to Design

Continuity; Transformation; Design Phases; Design Criteria; Managing Design; Summary;

16 Description and Computation

Translating Analysis Models; From Abstract to Concrete; Composing Classes; Controlling

Transitions; Generic Classes; Generating Instances; Design for Testability; Transformation and

Composition; Summary;

17 Attributes in Design

Defining Attributes; Concrete Attributes; Views; Exports; Composition and Inheritance;

Summary;

18 Relationships in Design

Relationships; Collections; Coordinators; Relations versus Composites; Summary;

19 Designing Transitions

States and Guards; Atomicity; Timing Constraints; Concrete Transitions; Summary;

20 Interaction Designs

Callbacks; Replies; Invocations; Control Flow; Summary;

21 Dispatching

Selection; Resolution; Routing; Summary;

22 Coordination

Joint Actions; Controlling Groups; Open Systems; Summary;

23 Clustering Objects

Clustering; Cluster Objects; System Tools and Services; Persistence; Summary;

24 Designing Passive Objects

Transformations; Storage Management; Passive Objects in C++; Summary;

25 Performance Optimization

Optimization and Evolution; Algorithmic Optimization; Performance Transformations;

Optimization in C++; Summary;

26 From Design to Implementation

Testing; Performance Assessment; Summary;

Appendix: Notation Summary

OAN; ODL;

Search:

Enter a search string (any case insensitive perl regexp) to produce an HTML index of all

occurrences in the book:

Related information

Errata for the first printing of the hardcover book version.●

A brief overview of some of the book (mainly topics from Part II dealing with distributed objects)

is available as a set of HTML-ized or Postscript slides from a 1993 presentation.

●

FAQ answers:

Dennis wrote most of Part I with the assistance of Penelope; Doug wrote Part II. A few

sections of chapters 6, 7, 8, and 15 were written jointly. It was written in 1991-3.

❍

You can read Parts I and II pretty much independently. Some people like to start with

chapter 16.

❍

Many of the pages were generated mechanically from the book form. They are not laid out

or hyperlinked together as well as they would be if they were written originally in HTML.

Sorry.

❍

While the book is mostly self-contained, people report that it does not serve as an

introductory OO text. It helps to have had some previous exposure to basic OO concepts.

❍

The main differences between the accounts in this book and most other OO texts lie in (1)

its non-commital stance about particular OO `methods' and languages (2) its focus on the

analysis and logical design of potentially distributed OO systems. However, it does not

address many nuts-and-bolts issues surrounding the use of real OO languages, tools, and

❍

●

Submit

Reset

systems for distribution in part because so few of them (of appropriate production quality)

were available at the time of writing.

While Part II consists largely of OO Design Patterns, they are not phrased as such, mainly

because this was written before now-common ideas about presenting, structuring and

documenting patterns arose.

❍

While there are many things we'd do differently if we were rewriting this book, there are no

current plans for a second edition. However, Dennis and Penlope have written a book on OO

Development Process and Metrics, and Doug has written one on Concurrent Programming

in Java.

❍

No, there are not postscript versions or any other copyable files available. If you want your

own copy, you'll have to buy the book. Also, please do not mirror these pages. (We don't

even have rights to give you permission to do so.)

❍

History

May95 Created.1.

Jan96 Changed background color to off-white for easier reading.2.

Mar96 Expanded and reformatted this page.3.

Aug96 Killed an annoying example.4.

Jan97 Reformatted to one chapter per file, restored searchable index, transformed gif-versions of

tables to html tables.

5.

This document was generated with the help of the LaTeX2HTML translator Version 95.1 (Fri Jan 20

1995) Copyright © 1993, 1994, Nikos Drakos, Computer Based Learning Unit, University of Leeds.

Preface

Object-oriented (OO) programming has a growing number of converts. Many people believe that object

orientation will put a dent in the software crisis. There is a glimmer of hope that OO software

development will become more like engineering. Objects, whatever they are now, may become for

software what nuts, bolts and beams are for construction design, what 2-by-4s and 2-by-6s are for home

construction, and what chips are for computer hardware construction.

However, before making this quantum leap, object-oriented methods still have to prove themselves with

respect to more established software development paradigms. True, for small tasks the war is over.

Object-oriented programs are more compact than classic structured programs. It is easier to whip them

together using powerful class libraries. Inheritance allows ``differential programming'', the modification

in a descendant class of what is wrong with a parent class, while inheriting all of its good stuff. User

interfaces, which are often sizable fractions of small systems, can be put together easily from

object-oriented libraries.

Delivering large object-oriented software systems routinely and cost effectively is still a significant

challenge. To quote Ed Yourdon: ``A system composed of 100,000 lines of C++ is not to be sneezed at,

but we don't have that much trouble developing 100,000 lines of COBOL today. The real test of OOP

will come when systems of 1 to 10 million lines of code are developed.

1

''.

1

Footnote:

To be fair and accurate, systems of 100,000 lines of C++ and those of 1,000,000 lines of

COBOL are often of the same order of magnitude in complexity.

The development of large systems is qualitatively different from that of small systems. For instance, a

multinational banking conglomerate may want a system supporting around-the-clock access to the major

stock markets in the world. They may additionally want to integrate accounts for all worldwide

customers, providing fault-tolerant distributed transaction services. The banking conglomerate cannot

realize this system by relying exclusively on a bundle of smart programmers. Instead, as enshrined by the

structured paradigm, analysis and design must precede pure implementation activities. OO methods are

known by experience to scale up to such large systems. For example, Hazeltine [2] reports a project with

``about 1000 classes, 10 methods per class, involving an average of 40 persons over 2 years.''

This book is intended to help the reader better understand the role of analysis and design in the

object-oriented software development process. Experiments to use structured analysis and design as

precursors to an object-oriented implementation have failed. The descriptions produced by the structured

methods partition reality along the wrong dimensions. Classes are not recognized and inheritance as an

abstraction mechanism is not exploited. However, we are fortunate that a multitude of object-oriented

analysis and design methods have emerged and are still under development. Core OO notions have found

their home place in the analysis phase. Abstraction and specialization via inheritance, originally

advertised as key ingredients of OO programming, have been abstracted into key ingredients of OO

analysis (OOA). Analysis-level property inheritance maps smoothly on the behavior inheritance of the

programming realm.

A common selling point of the OO paradigm is that it is more ``natural'' to traverse from analysis to

implementation. For example, as described in [1], developers at Hewlett-Packard who were well versed

in the structured paradigm reported that the ``conceptual distances'' between the phases of their project

were smaller using OO methods. Classes identified in the analysis phase carried over into the

implementation. They observed as well that the defect density in their C++ code was only 50% of that of

their C code.

However, more precise characterizations of why this might be so and how best to exploit it are still

underdeveloped. The black art mystique of OO methods is a major inhibitor to the widespread

acceptance of the OO paradigm. Hence we have devoted ample attention to the process aspects of

development methods.

Will this book be the last word on this topic? We hope not. The object-oriented paradigm is still

developing. At the same time, new challenges arise. Class libraries will have to be managed. Libraries for

classic computer science concepts can be traversed using our shared, common knowledge. But access to

application specific domain libraries seems to be tougher. Deciding that a particular entry is adequate for

a particular task without having to ``look inside'' the entry is a challenge. Will the man-page style of

annotations be sufficient? Our experience with man-pages makes us doubt that it will be.

Further horizons in OO are still too poorly understood to be exploited in the construction of reliable

systems. For example, some day methods may exist for routinely developing ``open systems'' of ``smart''

active objects inspired by the pioneering work of Hewitt.

2

While active object models do indeed form

much of the foundation of this book, their furthest-reaching aspects currently remain the focus of

research and experimental study.

2

Footnote :

Some quotes from this manifesto paper [3]: ``This paper proposes a modular ACTOR

architecture and definitional method for AI that is conceptually based on a single kind of

object: actors... The formalism makes no presuppositions about the representation of

primitive data structures and control structures. Such structures can be programmed,

micro-coded or hard-wired in a uniform modular fashion. In fact it is impossible to

determine whether a given object is `really' represented as a list, a vector, a hash table, a

function or a process. Our formalism shows how all of the modes of behavior can be defined

in terms of one kind of behavior: sending messages to actors.'' We briefly discuss open

systems of actors in Chapter 22.

The object oriented paradigm, and this book, may impact different software professionals in different

ways:

Analysts.

OO analysis is a fairly new enterprise. There is an abundance of unexplored territory to exploit. On

the other hand there are few gurus to rely on when the going gets tough. The OO paradigm is

tough going when one has been inundated with the structured way of thinking. While structured

analysis is supposed to be implementation technique independent, it turns out to have a built-in

bias toward classical implementation languages. Its core abstraction mechanism is derived from

the procedure/function construct. Letting structured abstractions play second violin to object and

inheritance takes some effort.

Designers.

OO design is as novel as OO analysis. By virtue of object orientation, more activities in the design

phase and links to both analysis and implementation can be distinguished than has been previously

possible. Our treatment focuses on the continuity of analysis and design, thus presenting many

descriptive issues that are normally considered as ``OO design'' activities in the context of OOA.

On the other side, it pushes many decisions that are usually made in the implementation phase into

design.

Implementors.

OO implementation should become easier when the task of satisfying functional requirements has

been moved into the design phase. Implementation decisions can then concentrate on exploiting

the features of a chosen configuration and language needed to realize all the remaining

requirements.

Software engineers.

OO software development is becoming a viable alternative to structured development. The

application domains of both appear virtually the same. While the structured version has the

advantage of currently being better supported by CASE tools, the object-oriented version will most

likely become even better supported.

Project managers.

Experience with OO methods may be obtained using a throwaway, toy example to go through all

the phases. The promise of large scale reuse should justify the transition costs. Software

development planning is notoriously hard. This text addresses this topic by formulating a generic

development scenario. However, foolproof criteria for measuring progress are as yet unavailable.

Tool builders.

The OO community needs integrated tools. In addition to object orientation, team effort, version

control, process management, local policies, metrics, all need support.

Methodologists.

We cite open issues and unsolved problems throughout the text, usually while discussing further

readings.

Students and teachers.

While the object-oriented paradigm is rapidly overtaking industrial software development efforts,

few courses address fundamental OO software engineering concepts untied to particular

commercial methods. We have successfully used material in this book as a basis for one-semester

graduate and undergraduate courses, one-week courses, and short tutorials

3

.

3

Footnote :

A team-based development project is almost mandatory for effective learning in

semester courses, but raises logistics problems common to any software engineering

course. Projects should neither be so big that they cannot be at least partially

implemented by a team of about three students within the confines of a semester, nor

be so small that they evade all systems-level development issues. Successful projects

have included a version of ftp with an InterViews[4] based interface, and a simple

event display system for Mach processes. To implement projects, students who do not

know an OO programming language will need to learn one long before the end of the

course. One way to address this is to teach the basics of OOP in a particular language

and other implementation pragmatics early on, independently of and in parallel with

the topics covered in this book. For example, in a course meeting two or three times

per week, one class per week could be devoted to programming and pragmatics. As

the semester continues, this class could focus on project status reports and related

discussions. This organization remains effective despite the fact that the contents of

the different classes are often out of synch. By simplifying or eliminating project

options corresponding to the contents of Chapters 22 through 26, final

implementation may begin while still discussing how these issues apply to larger

efforts.

Others.

The reader may think at this point that this book is relevant only for large system development. We

don't think so. Even in a one-hour single-person programming task, activities applying to a large

system can be recognized. The difference is that these activities all happen inside the head of the

person. There is no written record of all the decisions made. The person may not even be aware of

some of the decisions. We hope that everyone will obtain a better understanding of the overall

development process from this book.

This text does not aim at defining yet another OO ``method''. Instead, we aim to give a minimum set of

notions and to show how to use these notions when progressing from a set of requirements to an

implementation. We reluctantly adopt our own minimal (graphical) analysis and (textual) design

notations to illustrate basic concepts. Our analysis notation ( OAN) and design language ( ODL) are

``lightweight'' presentation vehicles chosen to be readily translatable into any OO analysis, design, and

programming languages and notations you wish to use. (Notational summaries may be found in the

Appendix 27.)

Most of what we have written in this book is not true. It is also not false. This is because we are in the

prescriptive business. Software development is a special kind of process. We describe in this book a

(loosely defined) algorithm for producing a system. Algorithms are not true or false. They are

appropriate for a task or not. Thus this book should contain a correctness proof that demonstrates that the

application of its methods invariably yields a desired system. However, due to space limitations, we have

omitted this proof.

More seriously, we have tried to decrease the fuzziness that is inherent in prescriptive text by giving

precise textual descriptions of the key notions in the respective methods. We have tried to be precise as

well, in describing how analysis output carries over into design and how the design output gets massaged

into an implementation. Thus we obtain checks and balances by integrating the methods across the

development phases. This, of course, provides only a partial check on the correctness of the methods.

Their application will be their touchstone.

We are opinionated regarding formal techniques. We want to offer software developers ``formality a la

carte''. Developers may want to avoid rigorous ``mathematical'' precision as one extreme, or may want to

provide correctness proofs of a target system against the requirements as another extreme. We leave this

decision to the developer. As a consequence for us, we avoid introducing notions for which the semantics

are not crystal clear. As a result, the developer can be as formal as desired. Since we were at times unable

to come up with concise semantics, we have omitted some modeling and design notions that are offered

in other accounts.

While we have tried to provide a solid foundation for the core concepts, we are convinced as well that a

true formalist can still point out uncountably many ambiguities. On the other side, we simply do not

understand most of the material in this book sufficiently well to trivialize it into recipes.

Although one can read this book while bypassing the exercises, we do recommend them. Some exercises

ask you to operationalize the concepts in this book. Others are quick ``thought questions'', sometimes

even silly sounding ones, that may lead you into territory that we have not explored.

Acknowledgments

Together, we thank our editors Alan Apt and John Wait, and reviewers Jim Coplien, Lew Creary,

Desmond D'Souza, Felix Frayman, Watts Humphrey, Ralph Johnson, and Hermann Kaindl.

DdC thanks Alan Apt for being a persistent initiator to this enterprise. He has an amazing ability to

exploit your vanity and lure you in an activity that is quite hazardous to plain family life. On the way he

gives encouragement, blissfully ignoring the perilous situation in which the writer has maneuvered

him/herself. Donna Ho provided an initial sanity check. Patricia Collins expressed very precisely her

concerns about domain analysis.

DL thanks others providing comments and advice about initial versions, including Umesh Bellur, Gary

Craig, Rameen Mohammadi, Rajendra Raj, Kevin Shank, Sumana Srinavasan, and Al Villarica. And, of

course, Kathy, Keith, and Colin.

We remain perfectly happy to take blame for all remaining omissions, stupidities, inaccuracies,

paradoxes, falsehoods, fuzziness, and other good qualities. We welcome constructive as well as

destructive critiques. Electronic mail may be sent to [email protected].

References

1

D. de Champeaux, A. Anderson, M. Dalla Gasperina, E. Feldhousen, F. Fulton, M. Glei, C. Groh,

D. Houston, D. Lerman, C. Monroe, R. Raj, and D. Shultheis. Case study of object-oriented

software development. In OOPSLA '92. ACM, 1992.

2

N. Hazeltine. Oopsla panel report: Managing the transition to object-oriented technology. OOPS

Chapter 1: Overview

Scope●

Objects●

Development Paradigms●

Development Phases●

Summary●

Scope

The development of a software system is usually just a part of finding a solution to a larger problem. The

larger problem may entail the development of an overall system involving software, hardware,

procedures, and organizations.

In this book, we concentrate on the software side. We do not address associated issues such as

constructing the proper hardware platform and reorganizing institutional procedures that use the software

to improve overall operations. We further limit ourselves to the ``middle'' phases of OO system

development. We discuss the initial collection of system requirements and scheduling of efforts only to

the extent to which they impact analysis. Similarly, we discuss situation-dependent implementation

matters such as programming in particular languages, porting to different systems, and performing

release management only with respect to general design issues. Also, while we devote considerable

attention to the process of OO development, we do not often address the management of this or any

software development process. We urge readers to consult Humphrey [8], among other sources, for such

guidance.

We cannot however, ignore the context of a software system. The context of any system is simply that

part of the ``world'' with which it directly interacts. In order to describe the behavior of a target system,

we have to describe relevant parts of the immediate context forming the boundary of the system.

Consequently, one may argue that the apparatus that we present in this book could be used for modeling

nonsoftware aspects as well. We do not deny potential wider applicability, but we have no claims in that

direction.

Running Example

Many examples in this text describe parts of the following system of automated teller machines

(ATMs):

We assume that the American Bank (AB) has partly decentralized account management. Every branch

office has equipment to maintain the accounts of its clients. All equipment is networked together. Each

ATM is associated and connected with the equipment of a particular branch office. Clients can have

checking, savings and line of credit accounts, all conveniently interconnected. Clients can obtain cash out

of any of their accounts. A client with a personal identification number (PIN) can use an ATM to transfer

funds among attached accounts. Daemons can be set up that monitor balance levels and trigger

automatic fund transfers when specifiable conditions are met and/or that initiate transfers periodically.

Automatic periodic transfers to third party accounts can be set up as well.

We will expand on these requirements as necessary. For presentation reasons, we often revise

descriptions from chapter to chapter. Our examples represent only small fragments of any actual system.

Objects

Objects have complex historical roots. On the declarative side, they somewhat resemble frames,

introduced in artificial intelligence (AI) by Marvin Minsky [10] around 1975. Frames were proposed in

the context of knowledge representation to represent knowledge units that are larger than the constants,

terms, and expressions offered by logic. A frame represents a concept in multiple ways. There is a

descriptive as well as a behavioral component. A frame of a restaurant would have as a descriptive

component its prototypical features -- being a business, having a location, employing waiters, and

maintaining seating arrangements. The behavioral component would have scripts. For example, a

customer script outlines stereotypical events that involve visiting a restaurant.

Objects and frames share the property that they bring descriptive and behavioral features closely

together. This shared feature, phrased from the programming angle, means that the storage structures and

the procedural components that operate on them are tightly coupled. The responsibilities of frames go

beyond those of objects. Frames are supposed to support complex cognitive operations including

reasoning, planning, natural language understanding and generation. In contrast, objects for software

development are most often used for realizing better understood operations.

On the programming side, the Simula [3] programming language is another, even older, historical root of

objects. Unsurprisingly, Simula was aimed at supporting simulation activities. Procedures could be

attached to a type (a class in Simula's terminology) to represent the behavior of an instance. Simula

supported parallelism , in the approximation of coroutines , allowing for many interacting entities in a

simulation.

Simula objects share the close coupling of data and procedures. The concurrency in Simula was lost in

Smalltalk , Eiffel , Objective-C , C++ , and other popular OO programming languages. However,

parallelism has reentered the OO paradigm via OO analysis methods and distributed designs. Modeling

reality with ``active'' objects requires giving them a large degree of autonomy.

The notion of whether objects have a parallel connotation or not is currently a major difference between

OO analysis and OO programming. Since we expect OO programming languages to evolve to support

the implementation of distributed, parallel systems, we expect this difference to decrease. The parallel

OO paradigm is well positioned to meet these upcoming demands.

Definitions

Like ``system'', ``software'', ``analysis'', and ``design'', the term ``object'' evades simplistic definition. A

typical dictionary definition reads:

object: a visible or tangible thing of relative stable form; a thing that may be apprehended

intellectually; a thing to which thought or action is directed [7].

●

Samplings from the OO literature include:

An object has identity, state and behavior (Booch [1]).●

An object is a unit of structural and behavioral modularity that has properties (Buhr [2]).●

Our own working definition will be refined throughout this book. We define an object as a conceptual

entity that:

is identifiable;●

has features that span a local state space;●

has operations that can change the status of the system locally, while also inducing operations in

peer objects.

●

Development Paradigms

The structured analysis (SA) paradigm [15] is rooted in third generation programming languages

including Algol , Fortran , and COBOL . The procedure and function constructs in these languages

provide for a powerful abstraction mechanism. Complex behavior can be composed out of or

decomposed into simpler units. The block structure of Algol-like languages provides syntactic support for

arbitrary many layers. Applied to the development of systems, this abstraction mechanism gives

prominence to behavioral characterization. Behavior is repeatedly decomposed into subcomponents until

plausibly implementable behavioral units are obtained.

The abandonment of sequential control flow by SA was a major breakthrough. Procedure invocations

have been generalized into descriptions of interacting processes. The ``glue'' between the processes are

data flows, the generalization of data that is passed around in procedure invocations. Processes represent

the inherent parallelism of reality. At the same time, the use of processes produces a mapping problem.

One has to transform a high level, intrinsically parallel description into an implementation that is usually

sequential. As we will see, the OO paradigm faces the same mapping problem.

The starting point for process modeling resides in the required behavior of the desired system. This

makes SA a predominantly top-down method. High level process descriptions are consequently target

system specific, and thus unlikely to be reusable for even similar systems. As a result, a description (and

a subsequent design and implementation) is obtained that is by and large custom fit for the task at hand.

OO software development addresses the disadvantage of custom fitting a solution to a problem. At all

levels of the development process, solution components can be formulated that generalize beyond the

local needs and as such become candidates for reuse (provided we are able to manage these

components).

Other aspects of OO development are available to control the complexity of a large system. An object

maintains its own state. A history-dependent function or procedure can be realized much more cleanly

and more independently of its run-time environment than in procedural languages. In addition,

inheritance provides for an abstraction mechanism that permits factoring out redundancies.

Applicability

Are the applicability ranges of the object-oriented paradigm and the structured paradigm different? If so,

how are they related? Is one contained in the other? Can we describe their ranges?

As yet there is not enough evidence to claim that the applicability ranges are different, although OO may

have an edge for distributed systems. Structured analysis thrives on process decomposition and data

flows. Can we identify a task domain where process decomposition is not the right thing to do, but where

objects can be easily recognized? Conversely, can we identify a task where we do not recognize objects,

but where process decomposition is natural? Both cases seem unlikely.

Processes and objects go hand in hand when we see them as emphasizing the dynamic versus the static

view of an underlying ``behaving'' substratum. The two paradigms differ in the sequence in which

attention is given to the dynamic and static dimensions. Dynamics are emphasized in the structured

paradigm and statics are emphasized in the OO paradigm. As a corollary, top-down decomposition is a

strength for the SA approach, while the grouping of declarative commonalities via inheritance is a

strength for the OO approach.

Mixing Paradigms

The software development community has a large investment in structured analysis and structured design

(SD). The question has been raised repeatedly whether one can mix and match components from the

structured development process with components of the OO development process. For instance, whether

the combination of SA + SD + OOP or SA + OOD + OOP is a viable route.

Experts at two recent panels

1

denied the viability of these combinations (but see Ward [13] for a

dissenting opinion). A key problem resides in the data dictionaries produced by structured analysis. One

cannot derive generic objects from them. Inheritance cannot be retrofitted. Also, the behavior of any

given object is listed ``all over the place'' in data flow diagrams.

1

Footnote :

panels at OOPSLA/ECOOP '90 and OOPSLA '91.

Consequently and unfortunately, we cannot blindly leverage SA and SD methods and tools. However,

OO analysis methods exist that do (partially) rely on SA to describe object behavior; see [6] for a

comparative study.

Development Methods

Within a given paradigm, one may follow a particular method

2

. A method consists of:

A notation with associated semantics.1.

A procedure/pseudo-algorithm/recipe for applying the notation.2.

A criterion for measuring progress and deciding to terminate.3.

2

Footnote :

We use the word method, not methodology. The primary meaning of methodology is ``the

study of methods'' which is the business of philosophers. The secondary meaning of

methodology is method. Since that is a shorter word we refrain from joining the

methodology crowd. (Similarly, we prefer using technique over technology.)

This book does not introduce yet another new method for OO development. We instead attempt to

integrate methods representative of the OO paradigm. Our OO analysis notation is just borrowed from

multiple sources. Still we have given it a name, OAN (Our Analysis Notation), for easy referencing. In

part II, we introduce ODL (Our Design Language), a language with similarly mixed origins. Summaries

of each are presented in the Appendix 27. When necessary to distinguish our views from those of others,

we will refer to these simply as ``our method'' ( OM).

Development Phases

No author in the area of software development has resisted denouncing the waterfall model . Everyone

agrees that insights obtained downstream may change decisions made upstream and thus violate a simple

sequential development algorithm. The notion of a development process in which one can backtrack at

each point to any previous point has led to the fountain metaphor (with, we assume, the requirements at

the bottom and the target system at the top).

Whether the development process has few feedback loops (the waterfall model) or many (the fountain

model) depends on several factors. The clarity of the initial requirements is an obvious factor. The less

we know initially about the desired target system, the more we have to learn along the way and the more

we will change our minds, leading to backtracking.

Another factor might be the integration level of tools that support the development process. A highly

integrated development environment encourages ``wild'' explorations, leading to more backtracking. On

the other hand without tool support, we may be forced to think more deeply at each stage before moving

on because backtracking may become too costly. The development style of team members may be a

factor as well.

It has been said that the object-oriented paradigm is changing the classic distinctions between analysis,

design and implementation. In particular, it is suggested that the differences between these phases is

decreasing, that the phases blur into each other. People claim that the OO paradigm turns every

programmer into a designer, and every designer into an analyst. We are willing to go only part way with

this view. There is empirical evidence from projects in which objects identified in the requirements phase

carried all the way through into the implementation (see [5]). We will see as well that notions and

notations used in analysis and design are similar, lending more support for this thesis.

On the other hand, intrinsic differences among phases cannot be forgotten. Analysis aims at clarifying

what the task is all about and does not go into any problem solving activity. In contrast, design and

implementation take the task specification as a given and then work out the details of the solution. The

analyst talks to the customer and subsequently (modulo fountain iterations) delivers the result to the

designer. The designer ``talks'', via the implementor, with hardware that will ultimately execute the

design. In a similar vein we do not want to blur the difference between design and implementation.

Contemporary OO programming languages have limitations and idiosyncrasies that do not make them

optimal thinking media for many design tasks.

It is, in our opinion, misleading to suggest that phase differences disappear in the OO paradigm. Objects

in the analysis realm differ significantly from objects in the implementation phase. An analysis object is

independent and autonomous. However, an object in an OO programming language usually shares a

single thread of control with many or all other objects. Hence, the design phase plays a crucial role in

bridging these different computational object models.

Prototyping

Prototyping

3

and exploratory programming are common parts of OO analysis, design and

implementation activities. Prototyping can play a role when aspects of a target system cannot be

described due to lack of insight. Often enough, people can easily decide what they do not want, but they

cannot describe beyond some vague indications what is to be produced.

3

Footnote :

We avoid the trendy phrase rapid prototyping since no one has yet advocated slow

prototyping.

Graphical user interfaces are an example. What makes a particular layout on a screen acceptable? Must a

system keep control during human interaction by offering menu choices or should control be relinquished

so that a user can provide unstructured input?

These kinds of question are sometimes hard or impossible to answer. Prototyping experimental layouts

can help. The situation resembles that of an architect making a few sketches so that a customer can

formulate preferences.

As long as the unknown part of the requirements is only a fragment of a system, OO analysis cooperates

with prototyping. Exploratory programming is called for when most of the requirements are not well

understood. Research projects fall into this category. Programming in artificial intelligence is an

example. Problem solving by analogy is particularly murky behavior. Exploratory programming can be a

vehicle for validating theories and/or for obtaining better conjectures.

We feel that purely exploratory programming applies to an essentially different set of tasks than the more

tractable (although possibly very large) tasks to which the methods described in this book apply.

Formulated negatively, the methods in this book may not apply when the development task is too simple

or when the task is too hard.

Elucidating functionality is just one of the motivations for prototyping. We have so far used

``prototyping'' primarily in the sense of ``throwaway prototyping'' -- aimed at gathering insights -- in

contrast to ``evolutionary prototyping'' -- aimed at implementing a system in stages. A prototyping

activity may have both aims but they need not coincide (see [4]). In Part II, we describe a framework for

design prototyping that is explicitly evolutionary in nature. Similarly, performance constraints may

require empirical evaluation via implementation-level prototyping.

Development Tools

Acceptance of the fountain metaphor as the process model for software development has profound

ramifications. Beyond toy tasks, tool support and integration of different tools is essential in enabling

backtracking. Of course these tools also need to support versioning, allow for traceability , and cater to

team development. These are quite stringent requirements, which are currently not yet satisfied. Various

groups are working on the standards to achieve tool control and data integration [11]. Manipulating

objects in all phases of the development process should make it easier to construct an integrated

development environment. We consider these issues in more detail in Chapter 12 and 15.

Summary

Software systems are often components of general systems. This book discusses only object-oriented

approaches to developing software systems. The roots of the OO paradigm include AI frames and

programming languages including Simula.

The structured paradigm focuses on decomposing behaviors. The OO paradigm focuses on objects,

classes, and inheritance. The two paradigms do not mix well. While the OO paradigm tightly integrates

the development phases of analysis, design and implementation, intrinsic differences between these

phases should not be blurred. OO methods are compatible with prototyping efforts, especially those

constructed in order to elucidate otherwise unknown requirement fragments.

Further Reading

Standard non-OO texts include Ward and Mellor's Structured Development for Real-Time Systems [14]

and Jackson's Systems Development [9]. OO texts that cover the full life cycle include Booch's Object

Oriented Design with Applications [1] and Rumbaugh et al's Object Oriented Modeling and Design [12].

Yearly proceedings are available from the principal OO conferences, OOPSLA (held in the Western

hemisphere) and ECOOP (Europe). Both originally focused on programming and programming

languages but have more recently broadened their attention to the full life cycle.

Exercises

Analysis aims at giving an unambiguous description of what a target system is supposed to do.

Enumerate the differences, if any, of an analysis method for characterizing software systems

versus an analysis method for characterizing hospital systems, or any other nonsoftware system

with which you are familiar.

1.

Consider whether the following list of items could be objects with respect to the definition given in

Section 1.2: an elevator, an apple, a social security number, a thought, the color green, yourself, a

needle, an emotion, Sat Jun 1 21:35:52 1991, the Moon, this book, the Statue of Liberty, high tide,

the taste of artichoke, 3.141..., (continue this list according to its pattern, if there is one).

2.

In general, prototyping may be seen as ``disciplined'' hacking that explores a narrow well defined

problem. Would the throwaway connotation of a produced artifact in this characterization change

as the result of an overall OO approach?

3.

References

1

G. Booch. Object Oriented Design with Applications. Benjamin/Cummings, 1990.

2

R. Buhr. Machine charts for visual prototyping in system design. Technical Report 88-2, Carlton

University, August 1988.

3

O. Dahl and K. Nygaard. Simula: An algol-based simulation language. Communications of the

ACM, 9, 1966.

4

A.M. Davis. Software Requirements, Analysis and Specification. Prentice-Hall, 1990.

5

D. de Champeaux, A. Anderson, M. Dalla Gasperina, E. Feldhousen, F. Fulton, M. Glei, C. Groh,

D. Houston, D. Lerman, C. Monroe, R. Raj, and D. Shultheis. Case study of object-oriented

software development. In OOPSLA '92. ACM, 1992.

6

D. de Champeaux and P. Faure. A comparative study of object-oriented analysis methods. Journal

of Object-Oriented Programming, March/April 1992.

7

Random House. The Random House College Dictionary. Random House, 1975.

8

W.S. Humphrey. Managing the Software Process. Addison-Wesley, 1990.

9

M. Jackson. Systems Development. Prentice Hall, 1982.

10

M. Minsky. A framework for representing knowledge. In P. Winston, editor, The Psychology of

Computer Vision. McGraw-Hill, 1975.

11

NIST. Reference Model for Frameworks of Software Engineering Environments. National Institute

of Standards and Technology, December 1991.

12

J. Rumbaugh, M. Blaha, W. Premerlani, F. Eddy, and W. Lorensen. Object-Oriented Modeling

and Design. Prentice Hall, 1991.

13

P.T. Ward. How to integrate object orientation with structured analysis and design. IEEE Software,

March 1989.

14

P.T. Ward and S. Mellor. Structured Development for Real-Time Systems. Prentice Hall, 1985.

15

E. Yourdon. Modern Structured Analysis. Yourdon Press, 1989.

Next: Chapter 2

Doug Lea

Wed Jan 10 07:51:53 EST 1996

Chapter 2: Introduction to Analysis

Purpose●

Models●

Process●

Summary●

Purpose

The analysis phase of object-oriented software development is an activity aimed at clarifying the

requirements of an intended software system, with:

Input:

A fuzzy, minimal, possibly inconsistent target specification, user policy and project charter.

Output:

Understanding, a complete, consistent description of essential characteristics and behavior.

Techniques:

Study, brainstorming, interviewing, documenting.

Key notion for the descriptions:

Object.

The final item in this list distinguishes object-oriented analysis from other approaches, such as Structured

Analysis [14] and Jackson's method [6].

Importance

Constructing a complex artifact is an error-prone process. The intangibility of the intermediate results in

the development of a software product amplifies sensitivity to early errors. For example, Davis [4]

reports the results of studies done in the early 1970's at GTE, TRW and IBM regarding the costs to repair

errors made in the different phases of the life cycle. As seen in the following summary table, there is

about a factor of 30 between the costs of fixing an error during the requirement phase and fixing that

error in the acceptance test, and a factor of 100 with respect to the maintenance phase. Given the fact that

maintenance can be a sizable fraction of software costs, getting the requirements correct should yield a

substantial payoff.

Development Phase Relative Cost of Repair

Requirements 0.1 -- 0.2

Design 0.5

Coding 1

Unit test 2

Acceptance test 5

Maintenance 20

Further savings are indeed possible. Rather than being aimed at a particular target system, an analysis

may attempt to understand a domain that is common to a family of systems to be developed. A domain

analysis factors out what is otherwise repeated for each system in the family. Domain analysis lays the

foundation for reuse across systems.

Input

There are several common input scenarios, generally corresponding to the amount of ``homework'' done

by the customer:

At one extreme, we can have as input a ``nice idea''. In this case, the requirements are most likely

highly incomplete. The characterization of the ATM system in Chapter 1 is an example. The

notion of a bank card (or any other technique) to be used by a customer for authentication is not

even mentioned. In this case, elaboration on the requirements is a main goal. Intensive interaction

between analyst and client will be the norm.

●

In the ideal case, a document may present a ``totally'' thought-through set of requirements.

However, ``totally'' seldom means that the specification is really complete. ``Obvious'' aspects are

left out or are circumscribed by reference to other existing systems. One purpose of the analysis is

to make sure that there are indeed no surprises hiding in the omissions. Moreover, a translation

into (semi) formal notations is bound to yield new insights in the requirements of the target

system.

●

In another scenario, the requirements are not yet complete. Certain trade-offs may have been left

open on purpose. This may be the case when the requirements are part of a public offering for

which parties can bid. For instance, we can imagine that our ATM example is a fragment of the

requirements formulated by a bank consortium. Since the different members of the consortium

may have different regulations, certain areas may have been underdefined and left to be detailed in

a later phase. A main aim of the analysis will be the precise demarcation of these ``white areas on

the map''.

●

A requirements document may propose construction of a line of products rather than one system in

particular. This represents a request for an OO domain analysis. Domain analysis specifies features

common to a range of systems rather than, or in addition to, any one product. The resulting domain

●

characterization can then be used as a basis for multiple target models. Domain analysis is

discussed in more detail in Chapter 13. Until then, we will concentrate most heavily on the

analysis of single target systems. However, we also note that by nature, OO analysis techniques

often generate model components with applicability stretching well beyond the needs of the target

system under consideration. Even if only implicit, some form and extent of domain analysis is

intrinsic to any OO analysis.

Across such scenarios we may classify inputs as follows:

Functionality:

Descriptions that outline behavior in terms of the expectations and needs of clients of a system.

(``Client'' is used here in a broad sense. A client can be another system.)

Resource:

Descriptions that outline resource consumptions for the development of a system (or for a domain

analysis) and/or descriptions that outline the resources that an intended system can consume.

Performance:

Descriptions that constrain acceptable response-time characteristics.

Miscellaneous:

Auxiliary constraints such as the necessity for a new system to interface with existing systems, the

dictum that a particular programming language is to be used, etc.

Not all these categories are present in all inputs. It is the task of the analyst to alert the customer when

there are omissions.

As observed by Rumbaugh et al [10], the input of a fuzzy target specification is liable to change due to

the very nature of the analysis activity. Increased understanding of the task at hand may lead to

deviations of the initial problem characterization. Feedback from the analyst to the initiating customer is

crucial. Feedback failure leads to the following consideration [10]: If an analyst does exactly what the

customer asked for, but the result does not meet the customer's real need, the analyst will be blamed

anyway.

Output

The output of an analysis for a single target system is, in a sense, the same as the input, and may be

classified into the same categories. The main task of the analysis activity is to elaborate, to detail, and to

fill in ``obvious'' omissions. Resource and miscellaneous requirements often pass right through, although

these categories may be expanded as the result of new insights obtained during analysis.

The output of the analysis activity should be channeled in two directions. The client who provided the

initial target specification is one recipient. The client should be convinced that the disambiguated

specification describes the intended system faithfully and in sufficient detail. The analysis output might

thus serve as the basis for a contractual agreement between the customer and a third party (the second

recipient) that will design and implement the described system. Of course, especially for small projects,

the client, user, analyst, designer, and implementor parties may overlap, and may even all be the same

people.

An analyst must deal with the delicate question of the feasibility of the client's requirements. For

example, a transportation system with the requirement that it provide interstellar travel times of the order

of seconds is quite unambiguous, but its realization violates our common knowledge. Transposed into the

realm of software systems, we should insist that desired behavior be plausibly implementable.

Unrealistic resource and/or performance constraints are clear reasons for nonrealizability. Less obvious

reasons often hide in behavioral characterizations. Complex operations such as Understand, Deduce,

Solve, Decide, Induce, Generalize, Induct, Abduct and Infer are not as yet recommended in a system

description unless these notions correspond to well-defined concepts in a certain technical community.

Even if analysts accept in good faith the feasibility of the stated requirements, they certainly do not have

the last word in this matter. Designers and implementors may come up with arguments that demonstrate

infeasibility. System tests may show nonsatisfaction of requirements. When repeated fixes in the

implementation and/or design do not solve the problem, backtracking becomes necessary in order to

renegotiate the requirements. When the feasibility of requirements is suspect, prototyping of a relevant

``vertical slice'' is recommended. A mini-analysis and mini-design for such a prototype can prevent

rampant throwaway prototyping.

Models

Most attention in the analysis phase is given to an elaboration of functional requirements. This is

performed via the construction of models describing objects, classes, relations, interactions, etc.

Declarative Modeling

We quote from Alan Davis [4]:

A Software Requirements Specification is a document containing a complete description of

what the software will do without describing how it will do it.

Subsequently, he argues that this what/how distinction is less obvious than it seems. He suggests that in

analogy to the saying ``One person's floor is another person's ceiling'' we have ``One person's how is

another person's what''. He gives examples of multiple what/how layers that connect all the way from

user needs to the code.

We will follow a few steps of his reasoning using the single requirement from our ATM example that

clients can obtain cash from any of their accounts.

Investigating the desired functionality from the user's perspective may be seen as a definition of

what the system will do.

The ability of clients to obtain cash is an example of functionality specified by the user.

1.

``The next step might be to define all possible systems ... that could satisfy these needs. This step

clearly defines how these needs might be satisfied. ...''

The requirements already exclude a human intermediary. Thus, we can consider different

techniques for human-machine interaction, for example screen and keyboard interaction, touch

screen interaction, audio and voice recognition. We can also consider different authentication

techniques such as PIN, iris analysis, handline analysis. These considerations address the how

dimension.

2.

``On the other hand, we can define the set of all systems that could possibly satisfy user needs as a

statement of what we want our system to do without describing how the particular system ... will

behave.''

The suggestion to construct this set of all systems (and apply behavior abstraction?) strikes us as

artificial for the present discussion, although an enumeration of techniques may be important to

facilitate a physical design decision.

3.

``The next step might be to define the exact behavior of the actual software system to be built ...

This step ... defines how the system behaves ...''

This is debatable and depends on the intended meaning of ``exact behavior''. If this refers to the

mechanism of the intended system then we subscribe to the quotation. However, it could also

encompass the removal of ambiguity by elaborating on the description of the customer-ATM

interaction. If so, we still reside in what country. For example, we may want to exemplify that

customer authentication precedes all transactions, that account selection is to be done for those

customers who own multiple accounts, etc.

4.

``On the other hand, we can define the external behavior of the actual product ... as a statement of

what the system will do without defining how it works internally.''

We may indeed be more specific by elaborating an interaction sequence with: ``A client can obtain

cash from an ATM by doing the following things: Obtaining proper access to the ATM, selecting

one of his or her accounts when more than one owned, selecting the cash dispense option,

indicating the desired amount, and obtaining the delivered cash.'' We can go further in our example

by detailing what it means to obtain proper access to an ATM, by stipulating that a bank card has

to be inserted, and that a PIN has to be entered after the system has asked for it.

5.

``The next step might be to define the constituent architectural components of the software system.

This step ... defines how the system works internally ...''

Davis continues by arguing that one can define what these components do without describing how

they work internally.

6.

In spite of such attempts to blur how versus what, we feel that these labels still provide a good initial

demarcation of the analysis versus the design phase.

On the other hand, analysis methods (and not only OO analysis methods) do have a how flavor. This is a

general consequence of any modeling technique. Making a model of an intended system is a constructive

affair. A model of the dynamic dimension of the intended system describes how that system behaves.

However, analysts venture into how-country only to capture the intended externally observable behavior,

while ignoring the mechanisms that realize this behavior.

The object-oriented paradigm puts another twist on this discussion. OO analysis models are grounded in

object models that often retain their general form from analysis (via design) into an implementation. As a

result, there is an illusion that what and how get blurred (or even should be blurred). We disagree with

this fuzzification. It is favorable indeed that the transitions between analysis, design, and implementation

are easier (as discussed in Chapter 15), but we do want to keep separate the different orientations

inherent in analysis, design, and implementation activities.

We should also note that the use of models of any form is debatable. A model often contains spurious

elements that are not strictly demanded to represent the requirements. The coherence and concreteness of

a model and its resulting (mental) manipulability is, however, a distinct advantage.

Objects in Analysis

OO analysis models center on objects. The definition of objects given in Chapter 1 is refined here for the

analysis phase. The bird's eye view definition is that an object is a conceptual entity that:

is identifiable;●

has features that span a local state space;●

has operations that can change the status of the system locally, while also inducing operations in

peer objects.

●

Since we are staying away from solution construction in the analysis phase, the objects allowed in this

stage are constrained. The output of the analysis should make sense to the customer of the system

development activity. Thus we should insist that the objects correspond with customers' notions, and add:

an object refers to a thing which is identifiable by the users of the target system -- either a tangible

thing or a mental construct.

●

Another ramification of avoiding solution construction pertains to the object's operator descriptions. We

will stay away from procedural characterizations in favor of declarative ones.

Active Objects

Some OO analysis methods have made the distinction between active and passive objects. For instance

Colbert [3] defines an object as active if it ``displays independent motive power'', while a passive object

``acts only under the motivation of an active object''.

We do not ascribe to these distinctions, at least at the analysis level. Our definition of objects makes them

all active, as far as we can tell. This active versus passive distinction seems to be more relevant for the

design phase (cf., Bailin [1]).

This notion of objects being active is motivated by the need to faithfully represent the autonomy of the

entities in the ``world'', the domain of interest. For example, people, cars, accounts, banks, transactions,

etc., are all behaving in a parallel, semi-independent fashion. By providing OO analysts with objects that

have at least one thread of control, they have the means to stay close to a natural representation of the

world. This should facilitate explanations of the analysis output to a customer. However, a price must be

paid for this. Objects in the programming realm deviate from this computational model. They may share

a single thread of control in a module. Consequently, bridging this gap is a major responsibility of the

design phase.

Four-Component View

A representation of a system is based on a core vocabulary. The foundation of this vocabulary includes

both static and dynamic dimensions. Each of these dimensions complements the other. Something

becomes significant as a result of how it behaves in interaction with other things, while it is distinguished

from those other things by more or less static features. This distinction between static and dynamic

dimensions is one of the axes that we use to distinguish the models used in analysis.

Our other main distinction refers to whether a model concentrates on a single object or whether

interobject connections are addressed. The composition of these two axes give us the following matrix:

inside object between objects

static

attribute

constraint

relationship

acquaintanceship

dynamic

state net and/or

interface

interaction and/or

causal connection

Detailed treatments of the cells in this matrix are presented in the following chapters.

The static row includes a disguised version of entity-relationship (ER) modeling . ER modeling was

initially developed for database design. Entities correspond to objects, and relations occur between

objects.

1

Entities are described using attributes . Constraints capture limitations among attribute value

combinations. Acquaintanceships represent the static connections among interacting objects.

1

Footnote:

The terms ``relation'' and ``relationship'' are generally interchangeable. ``Relationship''

emphasizes the notion as a noun phrase.

The dynamic row indicates that some form of state machinery is employed to describe the behavior of a

prototypical element of a class . Multiple versions of causal connections capture the ``social'' behavior of

objects.

Inheritance impacts all four cells by specifying relationships among classes. Inheritance allows the

construction of compact descriptions by factoring out commonalities.

Other Model Components

The four models form a core. Additional models are commonly added to give summary views and/or to

highlight a particular perspective. The core models are usually represented in graphic notations.

Summary models are subgraphs that suppress certain kinds of detail.

For instance, a summary model in the static realm may remove all attributes and relationship

interconnections in a class graph to highlight inheritance structures. Alternatively, we may want to show

everything associated with a certain class C, for example, its attributes, relationships in which C plays a

role, and inheritance links in which C plays a role.

An example in the dynamic realm is a class interaction graph where the significance of a link between

two classes signifies that an instance of one class can connect in some way or another with an instance of

another class. Different interaction mechanisms can give rise to various interaction summary graphs.

Another model component can capture prototypical interaction sequences between a target system and its

context. Jacobson [7] has labeled this component use cases . They are discussed in Chapters 10 and 12.

All of these different viewpoints culminate in the construction of a model of the intended system as

discussed in Chapter 10.

Process

Several factors prevent analysis from being performed according to a fixed regime. The input to the

analysis phase varies not only in completeness but also in precision. Backtracking to earlier phases is

required to the extent of the incompleteness and the fuzziness of the input. Problem size, team size,

corporate culture, etc., will influence the analysis process as well.

After factoring out these sources of variation, we may still wonder whether there is an underlying

``algorithm'' for the analysis process. Investigation of current OO analysis methods reveals that:

The creators of a method usually express only a weak preferences for the sequence in which

models are developed.

●

There is as yet no consensus about the process.●

There appear to be two clusters of approaches: (1) Early characterization of the static dimension by

developing a vocabulary in terms of classes, relations, etc. (2) Early characterization of the

behavioral dimension, the system-context interactions.

●

We have similarly adopted a weak bias. Our presentation belongs to the cluster of methods that focuses

on the static dimension first and, after having established the static models, gives attention to the

dynamic aspects. However, this position is mutable if and when necessary. For instance in developing

large systems, we need top-down functional decompositions to get a grip on manageable subsystems.

Such a decomposition requires a preliminary investigation of the dynamic realm. Chapter 9 (Ensembles)

discusses these issues in more detail. A prescribed sequence for analysis is given via an example in

Chapter 10 (Constructing a System Model). A formalization of this ``algorithm'' is given in Chapter 12

(The Analysis Process).

Summary

Analysis provides a description of what a system will do. Recasting requirements in the (semi) formalism

of analysis notations may reveal incompleteness, ambiguities, and contradictions. Consistent and

complete analysis models enable early detection and repair of errors in the requirements before they

become too costly to revise.

Inputs to analysis may be diverse, but are categorizable along the dimensions of functionality, resource

constraints, performance constraints and auxiliary constraints.

Four different core models are used to describe the functional aspects of a target system. These core

models correspond with the elements in a matrix with axes static versus dynamic, and inside an object

versus in between objects.

Analysis is intrinsically non-algorithmic. In an initial iteration we prefer to address first the static

dimension and subsequently the behavioral dimension. However, large systems need decompositions that

rely on early attention to functional, behavioral aspects.

Further Reading

We witness an explosion of analysis methods. A recent comparative study [5] describes ten methods. A

publication half a year later [9] lists seventeen methods. Major sources include Shlaer and Mellor

[11,12], Booch [2], Rumbaugh et al [10], Wirfs-Brock et al [13], and Jacobson et al [8].

Exercises

Discuss whether analysis, in the sense discussed in this chapter, should be performed for the

following tasks:

The construction of a new Fortran compiler for a new machine with a new instruction

repertoire.

1.

The planning for your next vacation.2.

The repair of faulty software.3.

The acquisition of your next car.4.

The remodeling of your kitchen.5.

The decision to get married.6.

The reimplementation of an airline reservation system to exploit five supercomputers.7.

A comparative study of OO analysis methods.8.

1.

Analysis is a popular notion. Mathematics, philosophy, psychiatry, and chemistry all have a claim

on this concept. Is there any commonality between these notions and the notion of analysis

developed in this chapter?

2.

Do you expect the following items to be addressed during OO analysis?

Maintainability.1.

3.

Quality.2.

The development costs of the target system.3.

The execution costs of the target system.4.

The programming language(s) to be used.5.

The reusability of existing system components.6.

The architecture of the implementation.7.

The relevance of existing frameworks.8.

References

1

S.C. Bailin. An object-oriented requirements specification method. Communications of the ACM,

32(5), May 1989.

2

G. Booch. Object Oriented Design with Applications. Benjamin/Cummings, 1990.

3

E. Colbert. The object-oriented software development method: A practical approach to

object-oriented development. In TRI-Ada 89, October 1989.

4

A.M. Davis. Software Requirements, Analysis and Specification. Prentice-Hall, 1990.

5

D. de Champeaux and P. Faure. A comparative study of object-oriented analysis methods. Journal

of Object-Oriented Programming, March/April 1992.

6

M. Jackson. Systems Development. Prentice Hall, 1982.

7

I. Jacobson. Object-oriented development in an industrial environment. In OOPSLA '87. ACM,

1987.

8

I. Jacobson, M. Christerson, P. Jonsson, and G. Overgaard. Object-Oriented Software Engineering.

Addison-Wesley, 1992.

9

T.D. Korson and V.K. Vaishnavi. Managing emerging software technologies: A technology

transfer framework. Communications of the ACM, September 1992.

10

J. Rumbaugh, M. Blaha, W. Premerlani, F. Eddy, and W. Lorensen. Object-Oriented Modeling

and Design. Prentice Hall, 1991.

11

S. Shlaer and S.J. Mellor. Object-Oriented Systems Analysis. Yourdon Press, 1988.

12

S. Shlaer and S.J. Mellor. Object Life Cycles: Modeling the World in States. Yourdon Press, 1991.

13

R. Wirfs-Brock, B. Wilkerson, and L. Wiener. Designing Object-Oriented Software. Prentice Hall,

1990.

14

E. Yourdon. Modern Structured Analysis. Yourdon Press, 1989.

Next: Chapter 3

Doug Lea

Wed Jan 10 07:52:09 EST 1996

Chapter 3: Object Statics

Instances●

Classes●

Attributes●

Attribute Features●

Constraints●

Identifying Objects and Classes●

Summary●

Instances

In previous chapters, we have shown definitions of objects, but we do not expect that the reader has a

``gut level'' understanding of what they are beyond the things that are usually encountered in everyday

life. We surmise that everyone starts out this way. Thus, an object can be your boyfriend, NYC, the

Ferrari in the showroom which is beyond your means, the Taj Mahal, etc. At the same time, objects can

be non-tangible things (provided that someone wants to see it that way) such as a bank transaction, a

newspaper story, a phone call, a rental car contract, a utility bill, an airline reservation, a bank account,

etc.

Our graphical notation for a singular object is simply a dot. For example an instance of the class

Account:

The heading of this section is ``instances'', not just ``objects''. We use the notion of an instance when we

want to emphasize that an object is a ``member'' of a class. In Chapter 2, we were already using the

notion of instance in the context of ``... an instance of one class ...'' In most methods, each object is

perceived as being a member of a certain class.

Classes

Sometimes we need to talk about a particular instance in our system model. For example, a bank may

maintain some key ``system'' accounts. We may want to describe a few special employees, e.g., the

executive officers. Usually, however, collections of objects, so-called classes

1

are described.

Footnote

1

:

The notions of ``type'' and ``class'' are sometimes distinguished in the implementation realm.

A type is the abstract characterization of a particular ``family'' of objects, while a class is

then the actual realization in a particular programming language of that type. We will

uniformly use the term ``class''. Later in Part II we refer to directly implementable versions

as ``concrete''.

A class stands for a family of objects that have something in common. A class is not to be equated with a

set of objects, although at any moment we can consider the set of instances that belong to the class. A

class may be seen as what all these sets have in common. In technical terminology, a class stands for the

intension of a particular characterization of entities, while the set of objects that conform to such a

characterization in a certain period is known as the extension (see Carnap [3]).

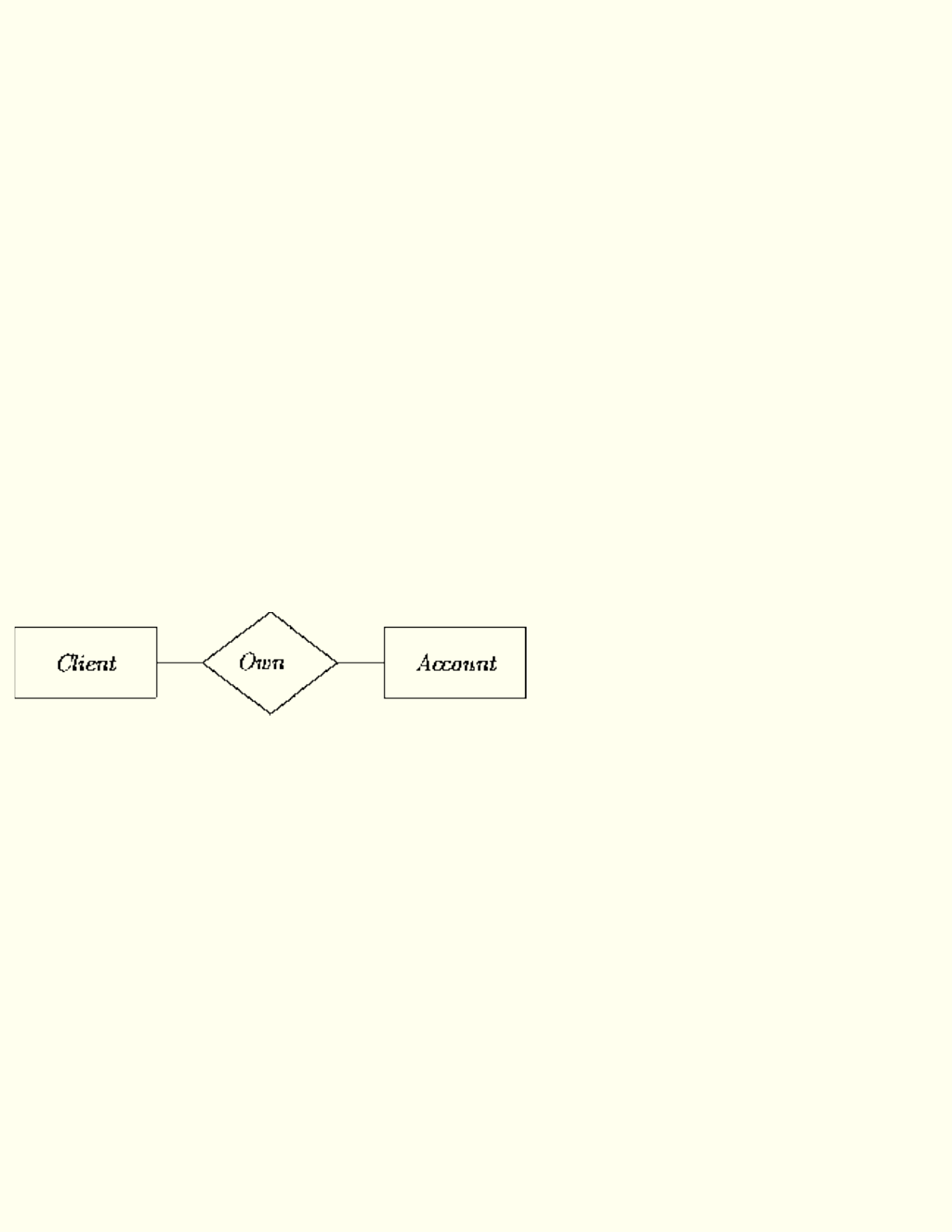

Notationally, a rectangle surrounds the name of a class. For example, the class Account is depicted as:

An object is an instance of at least one and at most one class. Certain methods allow an object to change,

during its lifetime, the class of which it is an instance. This freedom increases the expressive power of

the analysis method. But since most OO software development methods and languages do not support

this feature, and since the effects of change may be described by other means, we refrain from this

practice.

Individual objects are primarily characterized by an indication of which class they belong. For example:

The arrow between the instance and its class is called the ISA relationship. This is not the same as the

class inheritance relationship discussed in Chapter 7.

This instance characterization is insufficient. At this stage, we do not have available the means, beyond

naming, to distinguish multiple instances of the class Account. In general, we avoid using names to

describe individual objects, because usually objects do not have natural names. Just consider the

examples given earlier -- a bank transaction, a newspaper story, a phone call, a rental car contract, a

utility bill, and an airline reservation. Instead, descriptions are used that somehow denote unique entities.

Attributes of objects will do the descriptive job.

Attributes

Real-life entities are often described with words that indicate stable features. Most physical objects have

features such as shape, weight, color, and type of material. People have features including date of birth,

parents, name, and eye color. A feature may be seen as a binary relation between a class and a certain

domain. Eye color for example, may be seen as a binary relation between the class of Eyes and an

enumerated domain {brown, blue, yellow, green, red}. A domain can be a class as well, for example, in

the case of the features parents, spouse, accountOwnedBy, etc.

The applicability of certain features (i.e., the features themselves, not just their values) may change over

time. For example, frogs and butterflies go through some drastic changes in their lifetime. We avoid this

kind of flexibility. Thus, a class is characterized by its set of defining features, or attributes. This

collection of features does not change. (We later present tricks for getting around this limitation.)

The notion of a (binary) relation crept into the previous discussion. The reader may wonder how we can

discuss them here since we have relegated them to another model in our four-component view. We make

a distinction between attribute (binary) relationships that represent intrinsic, definitional properties of an

object versus relationships that describe contingent, incidental connections between objects. Because we,