This report does not constitute a rating action

Swedish Covered Bonds

Withstand Higher Mortgage Rates

Casper Andersen

Phuong Nguyen

June 20, 2024

• Average monthly mortgage payments in Sweden have increased by more than 68% since 2022, as policy and mortgage rates increased

to multi-year highs. Housing and utility costs now comprise 64% of the recent growth in consumer price index (CPI).

• The average monthly payment per loan part for a sample of over a million mortgage loans backing Swedish covered bond programs we

rate has risen to Swedish krona (SEK) 2,527 in 2024 from SEK1,503 in 2022, partly due to the increasing popularity of floating-rate

mortgages. Most Swedish borrowers have two loan parts.

• In our 2024 sample, borrowers already paying high installments have been proportionally more affected by increasing interest rates.

Since 2022, the proportion of borrowers paying less than SEK2,000 has decreased to below 50% from 74% and the proportion paying

more than SEK5,000 has increased to 7.4% from 2.2% .

• Loans originated in 2023 had 20% higher installments than those originated in 2021 due to lower interest-only availability and a higher

proportion of floating-rate loans. This has likely affected mortgage market activity.

• In our sample, more than 80% of loans are either floating-rate or will be reset to a fixed rate by the end of 2024, having then experienced

higher interest rates. The proportion of floating-rate and short-term fixed floating-rate loans has increased, thereby increasing overall

borrower interest sensitivity.

• Swedish mortgage performance remains stable despite our analysis highlighting higher-than-expected monthly payments. We expect

Swedish covered bond ratings to remain stable, given high overcollateralization buffers and unused notches of uplift from the issuer

credit rating.

Key Takeaways

2

3

Consumer Prices Are Normalizing, But Housing Costs Remain High

• Over 2022-2023, Swedish consumers suffered

a substantial cost of living shock.

• Despite falling since early 2023, consumer

price inflation remains higher than the long-

term average, mainly due to persistent

housing and utilities cost pressures, which

comprise 64% of the recent growth in CPI.

• We increased our short-to-medium term

inflation forecast due to prolonged high wage

growth against a backdrop of sluggish

productivity and uncertain trade

developments.

• As housing continues to contribute the most

to CPI growth (particularly at the start of

2024), the recent lowering of the policy rate

may have a knock-on effect on housing costs,

although it has not explicitly been stated by

the Swedish central bank as a driver for the

decision.

Swedish consumer price inflation components

Sources: Statistics Sweden, S&P Global Ratings.

-2

0

2

4

6

8

10

12

Jan-2020 Jul-2020 Jan-2021 Jul-2021 Jan-2022 Jul-2022 Jan-2023 Jul-2023 Jan-2024

Housing and Utilities Transport Food Other Overall Unemployment

• Following eight consecutive rate hikes leaving

the Swedish base rate at 4% in late 2023,

Sweden’s central bank (Riksbank) lowered its

policy rate by 25 basis points in May 2024, to

reflect closer to target inflation and weak GDP

growth and labor markets.

• We expect policy and market rates to continue

falling. The market consensus for the Swedish

base rate suggests 3% by the end of 2024.

• Swap rates are down and are steady at

between 2% and 3%, establishing a new

normal for mortgage rates. In our view, this will

help support mortgage borrowers.

Swedish interest rate benchmarks (%)

First Policy Rate Cut Since The 2023 Peak; Market Rates Continue To Fall

Dotted lines indicate market-implied forward rates for swaps and market consensus forecast for the policy rate.

Sources: Bloomberg, S&P Global Ratings.

-1

0

1

2

3

4

5

Jan. 2017 Jan. 2018 Jan. 2019 Jan. 2020 Jan. 2021 Jan. 2022 Jan. 2023 Jan. 2024

Policy rate Two-year swaps Five-year swaps

4

5

Typical Monthly Mortgage Payment Up By 68% Between Early 2022 And 2024

• We compared monthly mortgage payments in a 2024

sample of over a million Swedish mortgage loans with a

previous sample from 2022.

• The average monthly mortgage payment per loan part in our

2024 sample had increased by 68% to more than SEK2,500,

from SEK1,500 in our 2022 sample. Most Swedish borrowers

have two loan parts.

• Monthly payments have risen proportionally more for

borrowers already making higher payments than for those

making lower payments.

• The proportion of borrowers paying less than SEK2,000 has

decreased to below 50% in 2024 from 74% in 2022. Those

paying more than SEK5,000 now account for 7.4%, up from

2.2%.

bps--Basis points. SEK--Swedish krona. Source: S&P Global Ratings.

Monthly payment distribution

Rate (%)

Average

payment (SEK)

Average

increase (SEK)

Average

increase (%)

January

2022

1.60 1,503 -- --

January

2024

3.95 2,527 1,024 68

0

5

10

15

20

25

0-500

500-1000

1000-1500

1500-2000

2000-2500

2500-3000

3000-3500

3500-4000

4000-4500

4500-5000

5000-5500

5500-6000

6000-6500

6500-7000

7000-7500

7500-8000

>8000

Fraction of loan sample (%)

Monthly mortgage payment (SEK)

Jan. 2022 Jan. 2024

Collateral breakdown, by interest rate type Reset date distribution for fixed rate loans

Short-term fixed

49%

Floating for life

51%

6

Interest Rate Sensitivity On The Rise Due To More Floating-Rate Mortgages

And Shorter Rate Fixings

• Sweden is traditionally a mortgage market with short-term interest rate fixings. During the low interest rate environment, longer interest rate fixings gained

popularity, but this trend has now reversed.

• Between 2022 and 2024, the proportion of floating-rate mortgage loans in the sample backing the covered bonds we rate has increased to 51% from 41%,

making borrowers more sensitive to rate rise, on average.

• Furthermore, fixed-rate mortgages have a shorter fixing period, and about 45% of those will have reset by the end of 2024, from 40% in the 2022 sample.

0

5

10

15

20

Already

reset

2024 Q2

2024 Q3

2024 Q4

2025 Q1

2025 Q2

2025 Q3

2025 Q4

2026 Q1

2026 Q2

2026 Q3

2026 Q4

and later

Fraction of fixed-rate

loan sample (%)

Fixed-rate reset date

Collateral breakdown, by repayment type Remaining term for amortizing loans

Amortizing

57%

Interest-only

43%

7

Pools Now Have Lower Rate Sensitivity, Due To Fewer Loans With Long

Maturities And Interest-Only Repayment Profiles

• The proportion of our 2024 sample that is interest-only loans has decreased to 43% from 45% in 2022. However, this is still a significant share. Higher

mortgage rates have not led borrowers to take more interest-only loans but seem to have encouraged amortization slightly.

• Absolute monthly payments are generally lower for interest-only loans. However, these loans are more sensitive than amortizing loans to interest rate rises.

• Amortizing loans with a remaining term of more than 30 years have decreased to 14% of our sample, from 15%. Higher interest rates do not seem to have

increased mortgage maturities. This is important as loans with a longer maturity are also more sensitive to rising interest rates as the interest component is

a comparably higher portion of monthly installments.

0

10

20

30

40

50

60

<5 5-10 10-15 15-20 20-25 25-30 30-35 35-40 40-45 >45

Fraction of amortizing

loan sample (%)

Remaining term (years)

1,515

2,998

1,494

2,027

1,483

533

0

1,000

2,000

3,000

4,000

Jan. 2022 Jan. 2024 Jan. 2022 Jan. 2024

Floating for life Short-term fixed

(SEK)

Monthly payment Payment shock Share of sample

• In the 2024 sample, 49% of loans are fixed

rate and the rest (51%) are floating rate,

where rate rises materialize quicker.

• In our 2022 sample, 40% of loans had a

short-term fixed-rate, resetting by 2023,

and a further 45% will end their fixed-rate

period in 2024, which mean almost all

borrowers in the sample have been

affected by higher interests at the end of

2024.

• Therefore, more than 80% of the loans in

our 2024 sample will have seen some

impact from rate rises by the end of 2024.

• While payments on fixed- and floating-rate

mortgages were similar in our 2022 sample,

rising interest rates have doubled floating-

rate mortgage payments, while payments

on fixed-rate loans have only increased by

about one-third.

Monthly payments by loan product type

Most Loans Are Floating Rate, Or Will Revert From Fixed Rate By Year-End

Pie charts show prevalence of each loan product type in the sample. bps--Basis points. SEK--Swedish krona. Source: S&P Global Ratings.

51%

49%

8

2,152

3,007

716

1,903

855

1,187

0

1,000

2,000

3,000

4,000

Jan. 2022 Jan. 2024 Jan. 2022 Jan. 2024

Amortizing Interest-only

(SEK)

Monthly payment Payment shock Share of sample

9

Payment Shock Is More Severe For Interest-Only Borrowers

• In our 2022 sample, interest-only loan monthly payments

were typically much lower due to not having to regularly pay

down principal, averaging just SEK716, versus SEK2,152 for

repayment loans.

• Interest rate rises since 2022 have typically more than

doubled the monthly payment on interest-only loans, with

the average payment rising by almost SEK1,200 to more

than SEK1,900 per month in our 2024 sample.

• Repayment loans posted only a 40% average payment

increase of SEK855 from the previous payment.

• In the 2022 sample, amortizing mortgage payments were

more about three time that of average payments on

interest-only loans. In 2024, the difference changed to 58%.

Pie charts show prevalence of each loan product type in the sample. bps--Basis points. Base scenario is as of Jan. 1, 2022.

SEK--Swedish krona. Source: S&P Global Ratings.

Monthly payments by repayment type

57%

43%

10

New Loans Have High Payments, While Older Vintage Loans Have The Highest

Payment Increases

• Across our samples, loan payments for interest-only loans

increased. Since fewer new interest-only loans are being

granted, older vintage loans are more likely to be affected by

higher interest rates and payment shock.

• For instance, interest-only loans constituted a high

proportion (60%-70%) of loans originated before 2015.

• Earlier vintage loans--despite generally having lower loan

balances and lower monthly payments--have a greater

relative sensitivity to interest rate rises, on an average.

• For example, the average payment for 2011 vintage loans

was SEK963 at the beginning of 2022, compared with

SEK2,128 for the 2021 vintage.

• However, for 2011 vintage loans, the average monthly

payment has increased by 88%, versus only 34% for the

2021 vintage.

• Regardless, due to higher interest rates, borrowers from the

2023 vintage had a more than 20% higher installment than

borrowers from the 2021 vintage.

Payment shock and interest-only share, by loan vintage

SEK--Swedish krona. Source: S&P Global Ratings.

0

10

20

30

40

50

60

70

80

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Average monthly

payment (SEK)

Loan vintage

Interest-only (right scale)- 2024 sample

Interest only - 2024 sample

Amortizing loan - 2024 sample

Jan. 2024

Jan. 2022

(%)

Ratio of available to required credit enhancement Covered bond program uplift from issuer credit rating

11

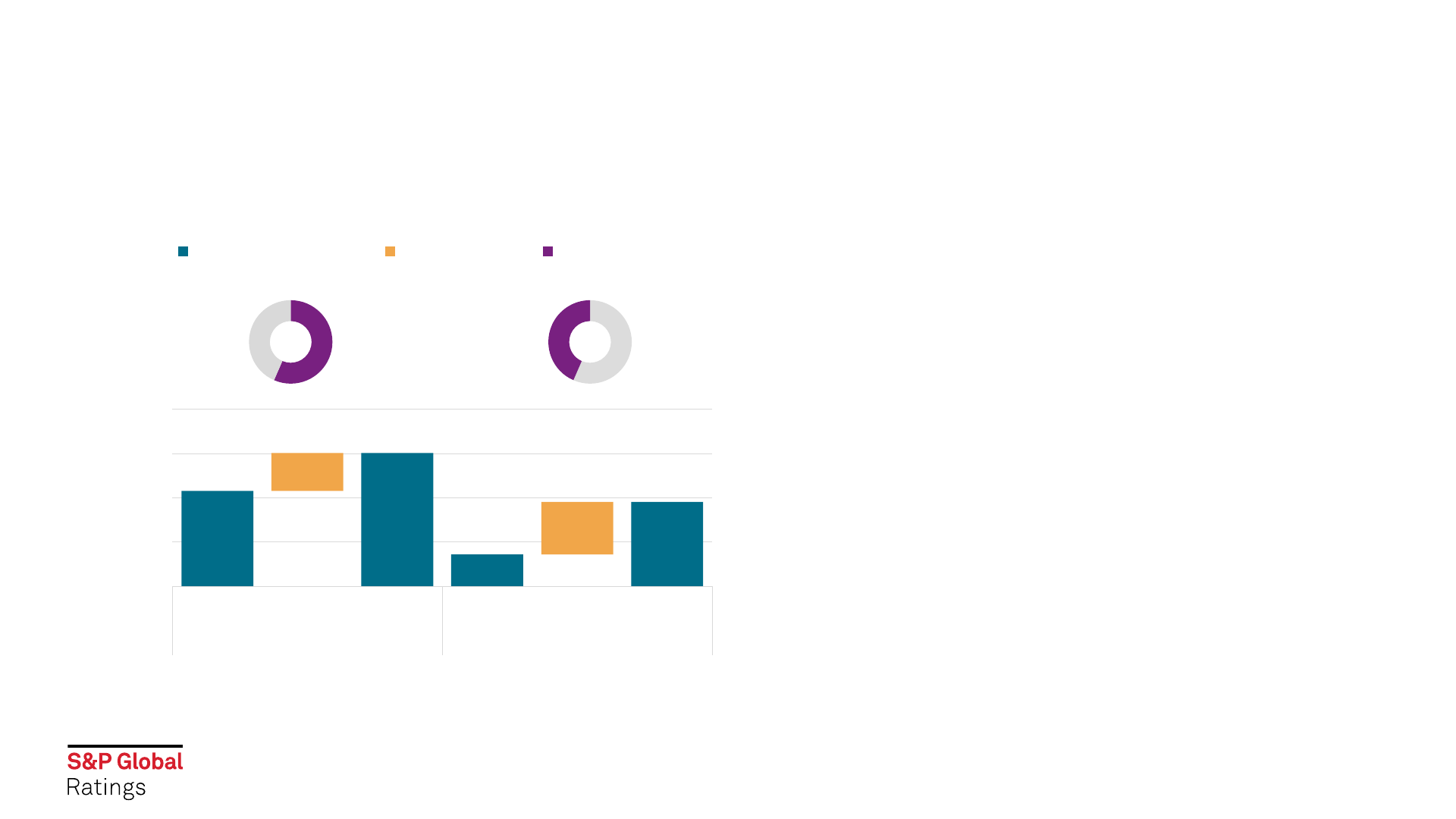

Swedish Covered Bond Ratings Should Withstand Weaker Loan Performance

• In 2024, Swedish banks' asset credit quality will likely remain under pressure due to high mortgage rates and potential labor market

pressure.

• However, Swedish covered bond programs have significantly more available credit enhancement than the level required to maintain

the current ratings, acting as a buffer against increasing credit losses.

• The ratings also benefit from "unused notches" of uplift, insulating program ratings if the issuer rating comes under pressure.

0

5

10

15

20

25

Sep-20

Dec-20

Mar-21

Jun-21

Sep-21

Dec-21

Mar-22

Jun-22

Sep-22

Dec-22

Mar-23

Jun-23

Sep-23

Dec-23

Mar-24

Jun-24

(x)

3

1

2

2

1

15 16 17 18 19 20 21 22 23

Swedbank Mortgage

Sparbank Skane

Lansforsakringar Hyp

Landshypotek

Danske Hyp

Issuer credit rating Resolution regime uplift

Jurisdictional uplift Sovereign rating

Number of unused notches

AAAAA+AAAA-A+AA-BBB+

• EMEA Structured Finance Chart Book: May 2024, May 13, 2024

• Global Covered Bond Insights Q2 2024: Strong Start To The Year For Issuance, March 27, 2024

• Economic Outlook Eurozone Q2 2024: Labor Costs Hinder Disinflation As Rate Cuts Loom

, March 26, 2024

• Swedish Real Estate: The End Of The Slump Could Soon Be In Sight, Feb. 29, 2024

• Nordic Banks In 2024: Ploughing On Through Tough Terrain, Feb. 7, 2024

• European Housing Markets: Forecast Brightens Amid Ongoing Correction, Jan. 25, 2024

• European Structured Finance Outlook 2024: Pushing On Through, Jan. 9, 2024

• Covered Bonds Outlook 2024: Stability Amid Turbulence, Dec. 11, 2023

• Swedish Covered Bond Market Insights 2023, Oct. 5, 2023

• Payment Shock In Swedish Covered Bond Pools, April 18, 2023

Related Research

12

Copyright © 2024 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form

by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized

purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P

Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is

provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE,

FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall

S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and

opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions

(described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following

publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other

business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no

duty of due diligence or independent verification of any information it receives. Rating-related publications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not

limited to, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such

acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been

suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not

available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are

made available on its Web sites, www.spglobal.com/ratings

(free of charge) and www.ratingsdirect.com (subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional

information about our ratings fees is available at www.spglobal.com/ratings/usratingsfees

.

Australia: S&P Global Ratings Australia Pty Ltd holds Australian financial services license number 337565 under the Corporations Act 2001. S&P Global Ratings' credit ratings and related research are not intended for and must not be

distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).

STANDARD & POOR'S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor's Financial Services LLC.

spglobal.com/ratings

14