UNIVERSITY OF OXFORD

Expenses Policy and

Claimant’s Guide

University of Oxford’s Expenses Policy

Purpose

This Policy establishes the rules on reimbursement of reasonable expenses incurred in the course of

University business. The overall purpose of the Policy is to guide claimants through incurring and

claiming these expenses, ensuring the process is as easy and efficient as possible. The Policy also

aims to make sure that:

• individuals neither lose nor gain financially;

• value for money is achieved;

• fraud is avoided; and

• tax and legal obligations are complied with.

Principles

Individuals should make payments to be reclaimed through expenses in line with the following

principles:

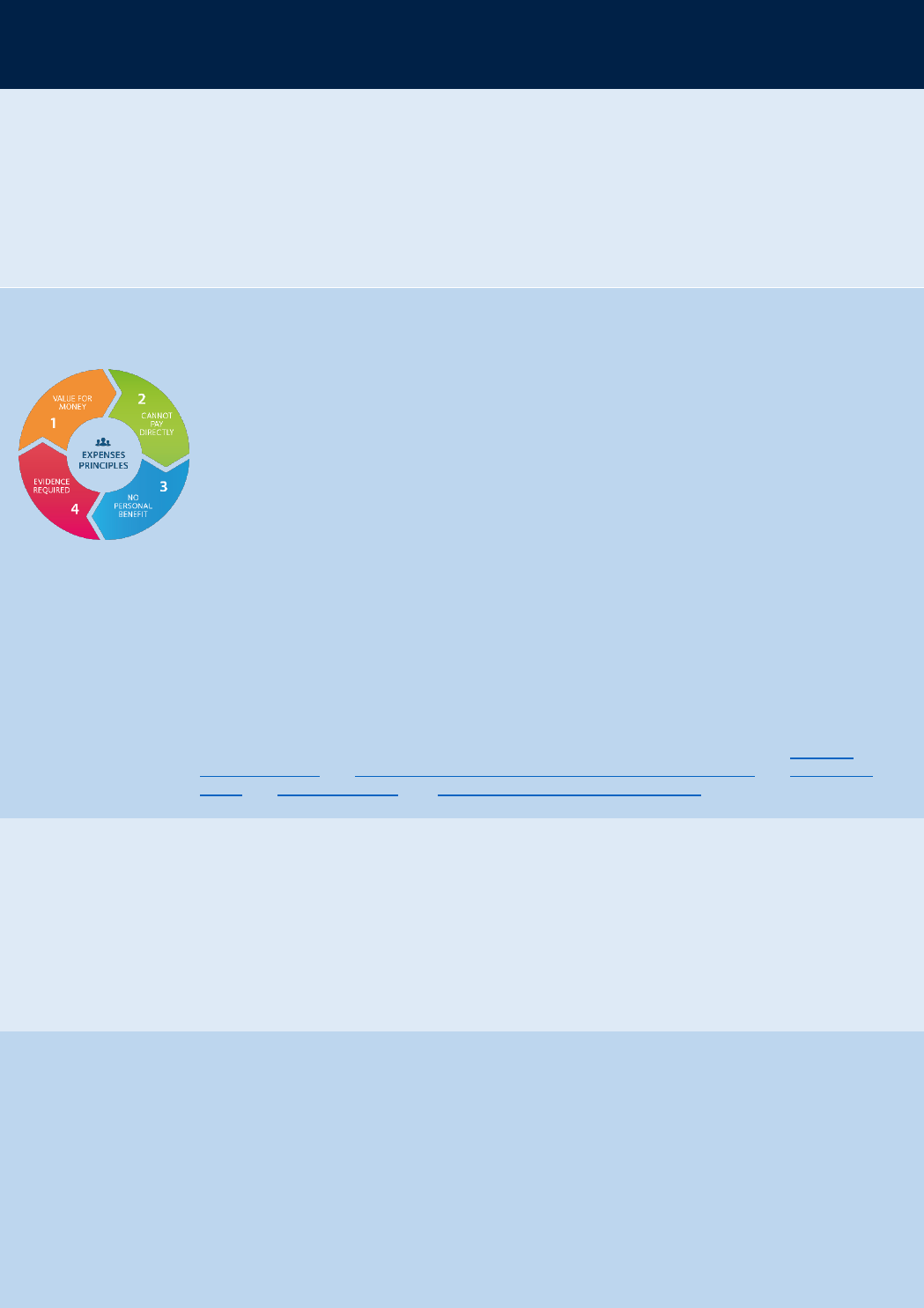

1. Value for money is achieved. Costs should be modest and reasonable, and any cost which

an external observer might regard as being unnecessary or excessive use of

public/charitable funds must be avoided. “Reasonable” expenses are those that are cost-

effective when weighed against the purpose of the activity. Reimbursement in full is not

guaranteed if the claim is not considered to be value for money.

2. Expenses should only be used when it is not possible and/or practical for the University to

pay for the good or service directly by raising a purchase order or receiving an invoice (as

opposed to the individual incurring the expense and being reimbursed.)

3. Costs incurred are for business purposes only, and the individual does not receive a

personal benefit (see taxation below).

4. Only actual and evidenced costs are reclaimed on a timely basis within the timeframe and

claims are authorised by someone other than the claimant or a related individual. Claimants

should note that an expense is not considered legitimate until authorised.

All expense claims must be in line with this Policy, which forms part of the Financial Regulations.

Any expenses charged to funds provided by research or other funders must, in addition, be in line

with that funder’s specific terms and conditions. This Policy applies in all cases unless grant terms

and conditions are stricter. The University is responsible for acting as a good steward of funds, and

therefore all expenditure should be in line with the principles irrespective of the source of funding.

This Policy should be read in conjunction with other University policies including the Gifts and

Hospitality Policy, the Statement of Policy and Procedure on Conflict of Interest, the Anti-Bribery

Policy, the Anti-Fraud Policy, and the Reward and Recognition Scheme.

Scope

This Policy applies to any expense claim submitted to the University (with the exception of OUP and

subsidiary entities). Claimants may include staff, students and visitors. The Policy also covers all

expenditure on an individual’s University Barclaycard and petty cash where relevant.

Heads of units are responsible for ensuring all members of the unit are made aware of the Expenses

Policy and the consequences of failing to comply. Compliance is mandatory and subject to audit.

Breaches will be taken seriously, and non-compliance may lead to disciplinary action.

Please note that the University does not refund expenses that constitute taxable benefits to non-staff

members (including students), except those included on a PAYE Settlement Agreement Form.

Responsibilities

• Claimant - responsible for ensuring that their claim is in line with all the requirements set out

in this Policy and any additional requirements established by research or other external

funders. Claimants submit a declaration confirming this with each claim submitted.

• Budget-holder/supervisor/Principal Investigator (optional) - if required by the Head of

Unit (or delegate), confirms that the activity has taken place and supports a genuine

business need, that it is appropriate to be met from their budget and there is budget

available.

• Head of unit (or their delegate) - has financial authority to approve claims in line with the

delegated scheme of authority. By approving the claim, the Authorised Signatory confirms

that:

• Each expense claim complies with the principles and requirements set out in this

Policy and any additional requirements established by research or other external

funders; the cost was incurred solely for business purposes; only actually and

evidenced costs are reclaimed; and the claim is correct, and all receipts are

attached.

• Budget is available.

• Coding is correct.

• Tax implications have been considered and any appropriate actions taken to

ensure that relevant items have been flagged to the Finance Division for the

application of tax.

• Finance Division - will hold departments to account for compliance with this policy. The

Finance Division will ensure that all tax treatment is correct.

Reasonable

Adjustments

Reasonable adjustments to this policy may be considered for those with disabilities or medical

conditions.

Departments may use discretion in application of the policy to ensure that the principles of equality

are met.

Taxation

Personal Benefits - an expense may be deemed a benefit and therefore taxable if the claimant could

benefit personally from it. For example if the University purchases a railcard for an employee which

allows discounted train travel, even though the primary use of train travel is for work, the employee

would be able to use that railcard for personal travel and so it would be deemed a taxable benefit.

The University manages tax treatment in line with HMRC regulations. No items resulting in a personal

taxable benefit should be claimed unless specified in this policy. All tax on benefits should be charged

to the individual, apart from tax charges arising as a result of declarations on a PAYE Settlement

Agreement Form.

Departments are provided with sufficient detail to understand when items should be referred to the

Finance Division for application of tax regulations. The Finance Division is responsible for ensuring

that tax is applied as appropriate.

Using this Policy

All claims must be in line with the principles set out above. The following sections of the Policy

provide further detail on the types of cost that are likely to meet these principles, noting that while

some flexibility is expected according to the situation, the principles apply in all cases.

If there are any doubts, you should always contact your departmental finance team prior to incurring

any costs. The Finance Division provides extra information and support to ensure departmental

finance teams can implement the policy.

Please note: This Policy is a live document that is subject to change on an ongoing basis. To ensure you

have the most up to date policy, please refer to the website at: https://finance.web.ox.ac.uk/expenses

1. Travel

The University will only reimburse the costs of travel incurred for a clearly defined and necessary

business purpose to an external site for activity that could not otherwise be facilitated at the place

of work or online.

Claimable

If you are travelling on University business you should use the best value for money method of travel.

Public

Transport

Rail, metro, bus, coach, plane

• Travel should be by standard / economy class; travel by other classes is unlikely to meet the value

for money principle.

• In exceptional circumstances, where travel in Premium Economy or Business Class is the only

practical option, this should be pre-agreed with the Head of Department (or their authorised

delegate) prior to travel being booked. Evidence of the agreement should be retained.

• Travel should be paid for by the University directly, using the preferred supplier when possible.

Taxis and

mini cabs

Taxis and mini cabs

May be permitted for short and infrequent journeys.

Hired Vehicles

In some circumstances where it is impractical to use public transport, hired vehicles may be needed.

• Hired vehicles should be booked by the University where possible.

• Hired vehicles may only be kept for as long as necessary for undertaking University business and

should not be used for private use.

Note: if you hire a vehicle directly you must ensure it is correctly insured for University use.

Private

Vehicles

If it is necessary to use private vehicles, mileage may only be claimed in line with the standard HMRC rates:

1. Car/Van:

• 45p per mile for the first 10,000 miles in each tax year;

• Then 25p per mile thereafter.

• An extra 5p per passenger per mile accompanying for University business can be claimed

up to the vehicles designed capacity.

2. Motorcycle/moped: at 24p per mile.

3. Bicycles: at 20p per mile.

Note: By submitting an expenses claim for mileage in a private vehicle, the claimant is declaring that they

have a valid driving licence, the vehicle is safe, legal and roadworthy, is maintained to the manufacturer’s

recommendations and is insured for business use.

Note: University credit cards may not be used to purchase fuel for private vehicles.

Travel

Charges

Reasonable parking charges, road tolls and congestion charges incurred on University business can be

claimed.

Travel insurance for overseas business travel may be reclaimed with departmental approval, only when

University insurance cannot be obtained.

Travel visas

Cost of essential travel visas can be claimed.

What

should not

be claimed

1. Ordinary commuting between your home and your normal place of work.

2. Charges for parking at your normal place of work.

3. Season/multiple journey tickets where it cannot be proved that they are solely for business use.

Only the cost of individual journeys will be refunded.

4. First class travel.

5. Fines e.g. parking or speeding fines.

6. Vaccinations should be arranged via the University’s Travel Clinic (Occupational Health).

2. Accommodation and Subsistence

The University will only reimburse accommodation and subsistence incurred while travelling for

University business and where the travel occupies the whole or substantial part of the working day.

Claimable

Accommodation and subsistence (meals, beverages and limited incidental costs) should be in line with

value for money principles, and claimants should not benefit.

Overnight

Accommodation

Appropriate and safe accommodation should be used, ensuring that value for money is achieved.

1. UK accommodation: reasonable rates are considered to be:

a. Major cities: £150 per night.

b. Other: £100 per night.

2. Overseas accommodation: at the discretion of the department. Reference can be made to

HMRC’s worldwide subsistence rates guide as needed.

Meals and

Beverages

Food and beverages taken as a meal (breakfast, lunch and dinner) can be claimed while travelling on

University business if the meal-time falls within the journey. Costs should not be excessive. Reasonable

rates in the UK are considered to be:

1. Breakfast: £10

2. Lunch: £10

3. Dinner: £25

4. Tips: Up to 15%.

These cannot be accumulated and must be supported by receipts.

Note: limited alcohol consumption as part of the meal can be claimed, however, this should be kept at a

reasonable level.

Incidental

Expenses

Incidental expenses such as WIFI, beverages, snacks, newspapers incurred whilst travelling (and

supported by receipts) can be claimed within the limits below. These limits cannot be accumulated.

1. UK: £5 per night for stays in the UK.

2. Non-UK: £10 per night for stays in the rest of the world.

Laundry

Laundry bills may be claimable if you are required to stay away from home for more than a week.

What should

not be claimed

1. No payment or payment in kind can be made if you stay with family/friends.

2. Personal items (e.g. toiletries).

3. Hospitality and Entertaining

The University will reimburse the provision of food, drink or other hospitality incurred in furthering

University business.

Claimable

Costs of refreshments and entertaining should be, and be seen to be, reasonable, in line with the value for

money principle and should not create a personal benefit. Government and some funders view hospitality

and entertainment as a personal benefit and therefore will not refund the costs. Wherever possible seek

guidance from your department before incurring costs.

Types of

Entertainment

Business entertainment: costs may be claimed for entertainment that furthers or promotes University

business (e.g. dinner for a seminar speaker, examiner lunch, meals with government officials).

Non-business (social) entertainment: please note that unless certain conditions (regular event, open to

all staff with a maximum spend of £150 per person per tax year inclusive of VAT) are met, this is a taxable

benefit.

Entertainment

Considerations

When entertaining, you should consider the following:

1. Cost: reasonable and proportionate to the situation?

2. Scale: what would be the public perception of the entertaining?

3. Alcohol: could the alcohol consumed be considered excessive either in price or amount

consumed? Would attendees have been affected by the amount of alcohol such that it is unlikely

that effective activity (e.g. networking) could be achieved?

Note: reference should also be made to the Anti-Bribery Policy, the Gifts and Hospitality Policy, the

Misuse of Alcohol and Drugs Policy and alcohol guidelines published by the Chief medical Officers of the

UK.

Refreshments

and Working

Meals

Refreshments and working meals should be arranged and purchased through your department wherever

possible.

It is reasonable to provide light refreshments (e.g. tea, coffee and biscuits) before, during or after a

meeting.

The cost of a working meals can only be claimed if:

• it is integral to the meeting; and

• a copy of the agenda, notes or action points are retained; and

• it takes place in an appropriate location:

o University staff only: must be taken on University premises

o University staff and externals: can take place on or off University premises; and

• alcohol is not consumed.

Note: a meal taken immediately after a meeting is considered to be entertainment, not a working meal.

A meal taken on college premises is not considered to be University premises.

Making a Claim

To make a claim, the following information must be provided:

1. the names of all attendees including staff;

2. the organisation of each attendee and staff status (OU staff/ non-OU staff);

3. the purpose of the entertainment; and

4. agenda/ meeting documentation should be attached when claiming working meals.

Note: for non-business entertaining that is deemed a taxable benefit (i.e. it does not meet the conditions

above, for example a team celebration meal or collaborator meal) the department is required either to

submit a PAYE Settlement Agreement (PSA) Form (the department will pay the tax) or to include the

event on the P11D Form so tax is charged to individuals.

What should

not be claimed

1. Entertaining for political events.

2. Tips in excess of 15%

4. Miscellaneous

The University may reimburse other costs relevant to undertaking University business.

Claimable

Below is a summary of some other common expenses incurred by University staff. You should speak to

your departmental finance team for further advice before spending.

Training and

Conferences

Where possible, training and conferences should be paid for in advance by the University. If this is not

possible, costs can be claimed in agreement with your department. Training and conferences should be

relevant to and support your role in the University.

Membership Fees

Fees for membership(s) relevant to your work can be claimed. Please note that if they are not on HMRC’s

list of approved professional bodies membership is considered a taxable benefit and tax may be charged.

Note: departments can take out organisation subscriptions which must be in the name of the University

i.e. a job title not a name.

Communication

Costs

Business use of a personal device will only be refunded if an itemised bill is provided with the relevant

costs identified. This includes overseas data bundles.

Note: University devices must be paid for by the department and remain the property of the University.

Phone hardware and associated costs will not be refunded via the expenses process.

Eyesight Costs

Arrangements have been made with certain opticians in Oxford who can provide eye tests for users of

display screen equipment. Most will submit an invoice i.e. a PO should be requested in advance.

Otherwise relevant costs can be claimed in line with the Health and Safety Policy (approved opticians

only).

Childcare Costs

Additional costs, surplus to existing childcare costs, may be claimed whilst undertaking training or

attending a conference, but not whilst in the performance of regular duties.

Sundry Costs

Occasionally, it will be most expedient to purchase low value computer accessories and office supplies

directly (e.g. a charging cable while travelling) and reclaim via expenses.

Gifts

From time to time it may be appropriate to give gifts. For example it may be culturally expected that an

official gift is given to non-staff members, or departments may consider it appropriate to give a small gift to

staff. Please note that any gift may be considered taxable.

The costs of gifts can only be claimed if they are:

• not in return for service(s);

• not money or vouchers;

• in line with the Gifts and Hospitality Policy;

• trivial;

• not regularly occurring.

Note: members of the University must act, and be seen to act, at all times in a manner that is fair,

impartial and without favouritism or bias. Reference should also be made to the Anti-Bribery Policy and the

Gifts and Hospitality Policy.

What should

not be claimed

1. Clothing - where required, the University will issue appropriate uniforms or workwear including

protective clothing.

2. IT equipment must be purchased by your department, including:

• hardware (e.g. monitors, laptops, tablets); and

• software including:

• Smartphone apps

• Cloud storage

• Other (e.g. operating systems, analytical programmes).

Note: all hardware or software is the property of the University.

3. Medical examinations - where the University requires individuals to undergo health checks or

screening, it will make all necessary arrangements directly with the medical practitioner and pay

directly all costs incurred.

4. Credit card costs – penalty charges or late payment fees will not be refunded if you use your

personal credit card.

5. Exceptional Circumstances and Complex Situations

Many departments have colleagues undertaking complex activities, including, for example, travel to

difficult or remote locations or fieldwork overseas.

In these circumstances, there may be a number of issues that need to be considered, including, but not

limited to, health and safety, insurance, tax, appropriate routes for engaging local workers, and ensuring

any funder terms and conditions are met.

Colleagues are likely to incur more unusual costs in these situations, and to ensure that the best possible

arrangements can be put in place to support and facilitate your work, please talk to your departmental

administration teams as soon as possible when you start planning. Departmental teams can obtain further

information from the Finance Division and other central services to ensure your work runs smoothly.

6. Advances

Advances for travel and subsistence will be provided where an individual would otherwise be

significantly financially disadvantaged by using the Expense Claim or other processes.

Travel

Advances

To avoid being significantly out of pocket, you can request funds in advance.

You should always ensure that the University pays for travel and accommodation directly before

considering an advance.

You can request a travel advance if:

• you will be travelling on business away from your normal place of work for at least one night;

• you would otherwise expect to submit an expenses claim in excess of £300; and

• it has not been possible for the University to pay directly.

Note: spend in a foreign currency is not in itself a valid reason for requesting an advance

Type of

Advance

Advances may be paid in a number of ways including:

1. Direct payment into the recipient's bank account. This is the preferred method.

2. Pre-paid card – you may be issued with a Mastercard which can be used to make purchases or

withdraw cash. All expenditure must be in line with this policy.

3. Currency (both cash and / or travellers' cheques). This should only be requested if it is

considered essential to carry cash (e.g. you are visiting a remote area and there are no local

banking facilities). Please note that cash overseas is not covered by University insurance (up to

£2,500 is covered in the UK).

Advances are limited to 75% of anticipated expenditure.

Note: reference should also be made to the Safety in Fieldwork Policy, Overseas Travel Policy, and

insurance and risk assessment arrangements.

Reporting

Advances

Funds provided in advance should only be used for the purposes outlined in the advance request and

must conform to the rules specified in this document.

• All expenditure must be in line with this policy. Repayment will be required for any expenditure

deemed inappropriate and not authorised.

• Expenditure should be reported promptly after travel is completed and must be completed

within three months of the activity concluding or return from travel.

• All expenditure must be supported by evidence.

• Any unspent advance must be repaid promptly.

• Claimants are not eligible to apply for another advance if reporting or repayment is outstanding.

7. Claiming Expenses

Claiming

Expenses

Claimants must provide the following information:

• Personal details (name, address, bank details).

• Sufficient information about the reason for the claim e.g. purpose of journey.

• If the expense was incurred in a foreign currency, evidence of the exchange rate used must be

provided. Appropriate evidence includes:

o Confirmation of exchange rate on date of payment from an established source e.g.

XE.com

o Evidence from bank, credit or charge card statement of actual rate of exchange.

Evidence

All claims must be supported by evidence i.e. receipts or equivalent proof of purchase. Credit card slips

or copies of bank statements alone are not normally considered to be as sufficient evidence to support a

claim.

Note: some funders may require additional information e.g. a boarding pass.

Submission of a

Claim

Claims should be submitted as close as possible to the time of expenditure. Claims should be submitted

within three months of the activity concluding or return from travel.

Declaration by

Claimant

In submitting an expense claim you are confirming that:

• Value for money was achieved.

• It was not possible and/or practical for the University to pay directly.

• The cost was incurred for business purposes only.

• Only actual and evidenced costs are reclaimed.

Authorisation

Claims must be authorised by an appropriate Authorised Signatory. In no circumstances will self-

authorised claims be paid.

Note: if required, the budget holder, supervisor or principle investigator can give initial approval. This is

a matter of departmental practice.

The Authorised Signatory is responsible for confirming:

• Each expense complies with the principles and requirements set out in this Policy and any

additional requirements established by research or other external funders; the cost was

incurred solely for business purposes; only actually and evidenced costs are reclaimed; and the

claim is correct, and all receipts are attached.

• Budget is available.

• Coding is correct.

• Tax implications have been considered and any appropriate actions taken to ensure that

relevant items have been flagged to the Finance Division for the application of tax.

Payment instructions and claims must not be authorised by any member of staff junior to the person

receiving payment unless either the signatory is defined in the following table or a separate, specific

arrangement has been agreed in writing with the Director of Finance.

Claimant

Authoriser

Head of Administration and

Finance (or equivalent)

Head of Department or any of the officers below.

Head of Department (for

claims exceeding £100)

Head of Division

Divisional Registrar

Divisional Financial Controller

Any of the officers below.

Head of Division or Pro-Vice

Chancellor

Director of Finance (or Divisional Financial Controller as their

delegate)

Registrar (or Divisional Secretary as their delegate)

Vice Chancellor

Vice Chancellor

Chancellor

Chancellor

Chairman of Audit Committee