FDIC QUARTERLY

51

TRENDS IN MORTGAGE ORIGINATION AND SERVICING:

Nonbanks in the Post-Crisis Period

1

For this article, the financial crisis period is defined throughout as 2008 through 2009, corresponding roughly to the most acute

phase of the financial crisis. The FDIC has referred to the broader banking crisis as extending through 2013. See FDIC, Crisis and

Response: An FDIC History, 2008–2013 (2017), https://www.fdic.gov/bank/historical/crisis/.

2

Home equity loans and home equity lines of credit are included in 1–4 family mortgages outstanding.

3

Board of Governors of the Federal Reserve System, “Z.1 Financial Accounts of the United States, Second Quarter 2019,”

https://www.federalreserve.gov/releases/z1/20190920/z1.pdf, L.218.

4

Private-label issuance is 5.2 percent of all residential mortgage-backed securitization issuance, down from more than 50 percent

in 2005 and 2006, and the 1995 to 2003 share of near 20 percent, according to the Urban Institute, “Housing Finance at a Glance,”

August 2019:12, https://www.urban.org/sites/default/files/publication/100866/august_chartbook_2019_0.pdf.

5

According to the Urban Institute’s July 2019 edition of “Housing Finance at a Glance,” of all first-lien originations in first

quarter 2019, 39.6 percent were GSE securitizations, 37.3 percent were portfolio originations, 20.2 percent were Federal Housing

Administration (FHA) or Department of Veterans Affairs (VA) securitizations, and 2.9 percent were private-label securitizations.

The percentage of private-label securitizations was the highest since 2007, but a small fraction of the private-label share in the

years leading up to the crisis. https://www.urban.org/sites/default/files/publication/100723/july_chartbook_2019_1.pdf.

6

Ben S. Bernanke, “Housing, Housing Finance, and Monetary Policy,” speech at the Federal Reserve Bank of Kansas City

Economic Symposium, Jackson Hole, Wyoming, August 31, 2007, https://www.federalreserve.gov/newsevents/speech/

bernanke20070831a.htm; and Marshall Lux and Robert Greene, “What’s Behind the Non-Bank Mortgage Boom?” Harvard

Kennedy School, June 2015:5, https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/working.papers/42_Nonbank_

Boom_Lux_Greene.pdf.

Introduction The mortgage market changed notably after the collapse of the U.S. housing market in

2007 and the financial crisis that followed. A substantive share of mortgage origination and

servicing, and some of the risk associated with these activities, migrated outside of the bank-

ing system. Some risk remains with banks or could be transmitted to banks through other

channels, including bank lending to nonbank mortgage lenders and servicers.

1

Changing

mortgage market dynamics and new risks and uncertainties warrant investigation of poten-

tial implications for systemic risk.

This article covers trends in the volume of 1–4 family mortgages outstanding, migration

of mortgages between market participants, and the drivers of these shifts. Next, the article

discusses trends in residential mortgage origination and servicing from 2000 to early 2019

and discusses the landscape of the mortgage industry, key characteristics of nonbank origi-

nators and servicers, and the potential risks posed by nonbanks. Last, the article contem-

plates the implications that the migration of mortgage activities to nonbanks may have for

banks and the financial system.

Trends in the Volume of and

Competition for 1–4 Family

Home Mortgage Loans

Mortgage originators and servicers have long competed for market share through innova-

tions in capital markets, customer service, and funding and business structures, and in

applying technology to make processes more efficient and cost-effective. The composition

and the concentration of the dominant market participants have varied with developments

in regulation, government intervention and guarantees, primary and secondary mortgage

markets, securitization, technological innovation, dynamics in housing markets, financial

markets, and the broader economy.

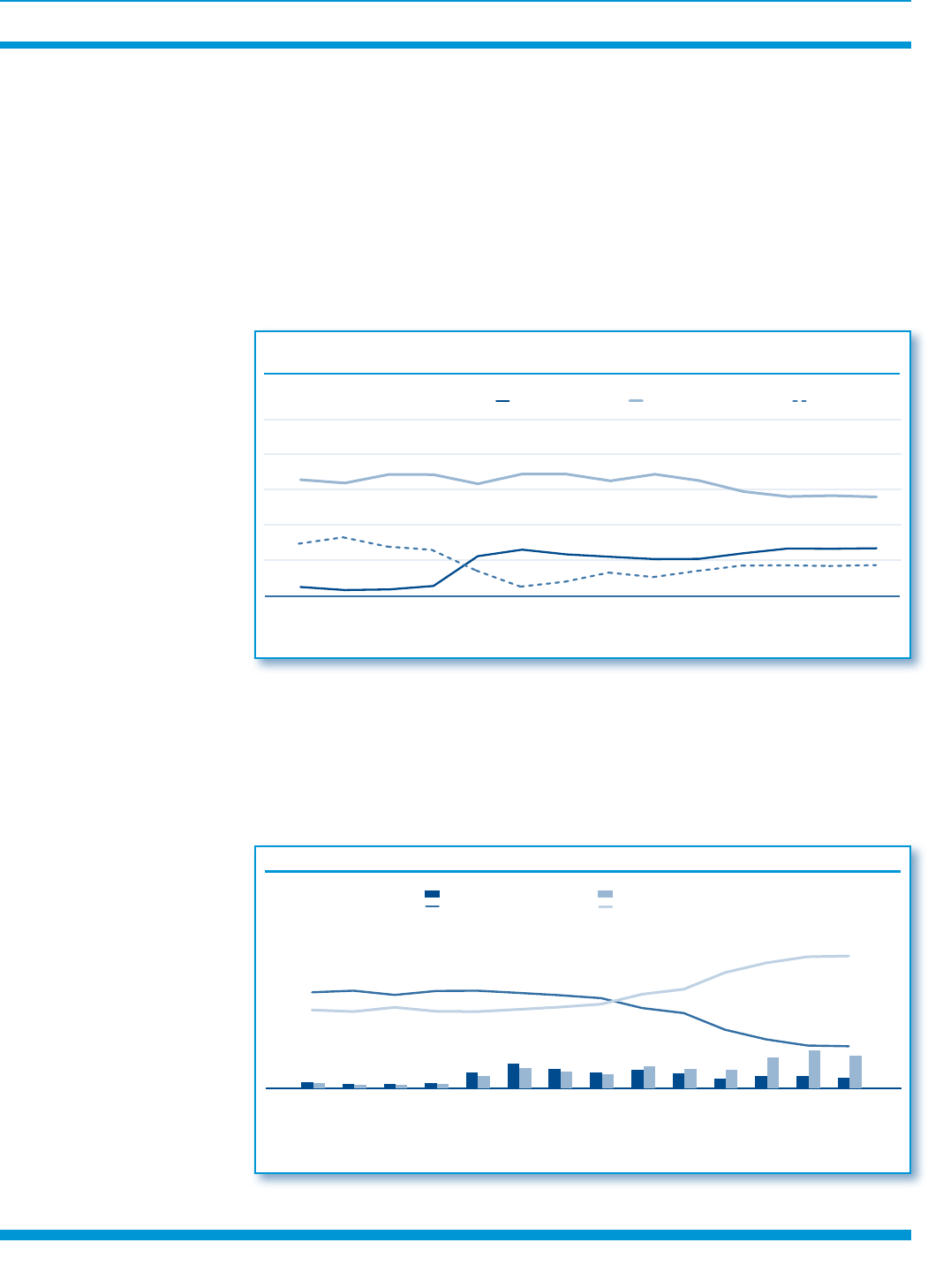

The share of 1–4 family mortgages outstanding held by banks has declined since the late

1970s as mortgages held by the government-sponsored enterprises (GSEs) and mortgages in

agency- and GSE-backed mortgage pools became an increasingly dominant part of the U.S.

mortgage market (Chart 1).

2

The share of mortgages outstanding held by banks declined

from the 1970s through the 1990s and then leveled off near 24percent in the past decade.

3

The bank share of mortgages held by non-GSE entities declined through 2007 to 46percent,

then rebounded to nearly 64percent in 2019. This decline and recovery was largely driven

by the rise and fall of private-label mortgage-backed securitization.

4

These historical shifts

in outstanding mortgage volumes were largely driven by securitization trends and a robust

secondary market for mortgages.

5

Insolvency in thrifts in the early 1980s and the savings and loan crisis of the late 1980s

contributed significantly to the decline in bank market share. These events in the 1980s

ended the dominance of deposit-taking portfolio lenders in the mortgage markets, leaving

mortgage lending largely to growing regional banks and a growing number of nonbanks.

6

2019 • Volume 1 3 • Number 4

52 FDIC QUARTERLY

e Bank Share of 1–4 Family Mortgages Outstanding Declined rough the 1980s and

Flattened in 2009

Source: Federal Reserve Flow of Funds (Haver Analytics).

Notes: Data as of June 2019. Dollar values are adjusted for ination, expressed as trillions of chained 2012 dollars.

GSEs (government-sponsored enterprises) includes mortgages held by GSEs and mortgages held by agency- and GSE-backed mortgage pools.

Mortgages Outstanding

$ Trillion 2012

Banks Credit Unions

GSEs Issuers of ABS

Other Financial

Nonnancial

Bank Share of Mortgages

Percent

2

4

6

8

10

12

14

1952 1961 1970 1979 1988 1997 2006 2015

0

Bank Share of Mortgages (Right Axis)

Bank Share of Non-GSE Mortgages (Right Axis)

0

10

20

30

40

50

60

70

80

90

Chart 1

Two types of entities originate and service mortgages: 1) banks and their affiliates and

2)nonbanks that are not part of or affiliated with depository institutions.

7

Banks have access

to deposits and other borrowings for funding while nonbanks are financed through means

other than deposits. Banks and nonbanks originate loans and either hold the loans on their

balance sheets until maturity or securitize and sell the loans on the secondary market. The

latter describes the originate-to-distribute model, which is the form of financing particu-

larly prevalent among nonbank mortgage lenders.

8

Because they rely on the originate-to-

distribute model, nonbank mortgage lenders are largely absent in measures of the holdings

of mortgages outstanding in Chart 1, though they have been originating mortgages dating

back to at least World War II.

9

The post-crisis shift in residential mortgage lending activity

from banks to nonbanks has mostly involved originations and servicing rather than holdings

of loans. In 2016, the volume of 1–4 family mortgages originated by nonbanks surpassed the

volume originated by banks (Chart 2).

7

Throughout this article, mortgage originators are generally classified as “bank” or “nonbank” using Home Mortgage Disclosure

Act (HMDA) data. “Nonbanks” include all U.S. Department of Housing and Urban Development (HUD) reporters. “Banks”

include banks, credit unions, and their affiliates. Any references to HMDA origination data includes single-family residential

originations, defined as first-lien purchase or refinance loans secured by an owner-occupied, 1–4 family unit, site-built

property. Mortgage servicers were categorized for this article using organization hierarchies published by the Federal Financial

Institutions Examination Council National Information Center. For a given year, each entity identified in the Inside Mortgage

Finance servicing rankings was located by name on the National Information Center website (https://www.ffiec.gov/npw)

and an organization hierarchy for that year for that entity or that entity’s parent holding company was searched. If the entity’s

organization hierarchy or the hierarchy of its parent holding company included a bank (depository institution), savings and

loan association, or a credit union, the entity was categorized as a bank for that year. All other entities in that ranking year were

categorized as nonbanks. Any references to Inside Mortgage Finance mortgage servicing data generally refer to the rankings of

the top 25 mortgage servicing participants by total residential mortgages serviced. The Inside Mortgage Finance ranking includes

entities that own mortgage servicing rights, but do not service loans directly, and some institutions that are subservicers only

(firms that service mortgages on a contract basis).

8

FDIC analysis of 2017 HMDA data indicates that through the first three quarters of 2017, banks sold nearly half of their

1–4 family originations in aggregate, while nonbanks sold more than 97 percent. In aggregate, nonbanks sold 34.1 percent to the

GSEs, 20.8 percent into securitizations guaranteed by Ginnie Mae, and 42.7 percent to other entities. In aggregate, banks sold

27.2percent to the GSEs, 7.2 percent into securitizations guaranteed by Ginnie Mae, and 19.0 percent to other entities. Disposition

shares are based on originations from the first three quarters of 2017, to correct for censoring. “Other” dispositions include sales

to commercial banks, mortgage banks, life insurance companies, affiliated institutions, and into private-label securities.

9

According to Bernanke’s “Housing, Housing Finance, and Monetary Policy,” following World War II, the mortgage market took

on the form that would last several decades. The market consisted of two main sectors. The first sector consisted of savings and

loan associations, mutual savings banks, and, to a lesser extent, commercial banks, primarily financed by short-term deposits.

These institutions made conventional fixed-rate long-term loans to homebuyers. Notably, federal and state regulations limited

geographical diversification for these lenders. Largely the product of New Deal programs established in the 1930s, the second

sector included private mortgage brokers and other lenders that largely originated standardized loans backed by the FHA and the

VA. These guaranteed loans could be held in portfolio or sold to institutional investors through a nationwide secondary market.

FDIC QUARTE RLY

53

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

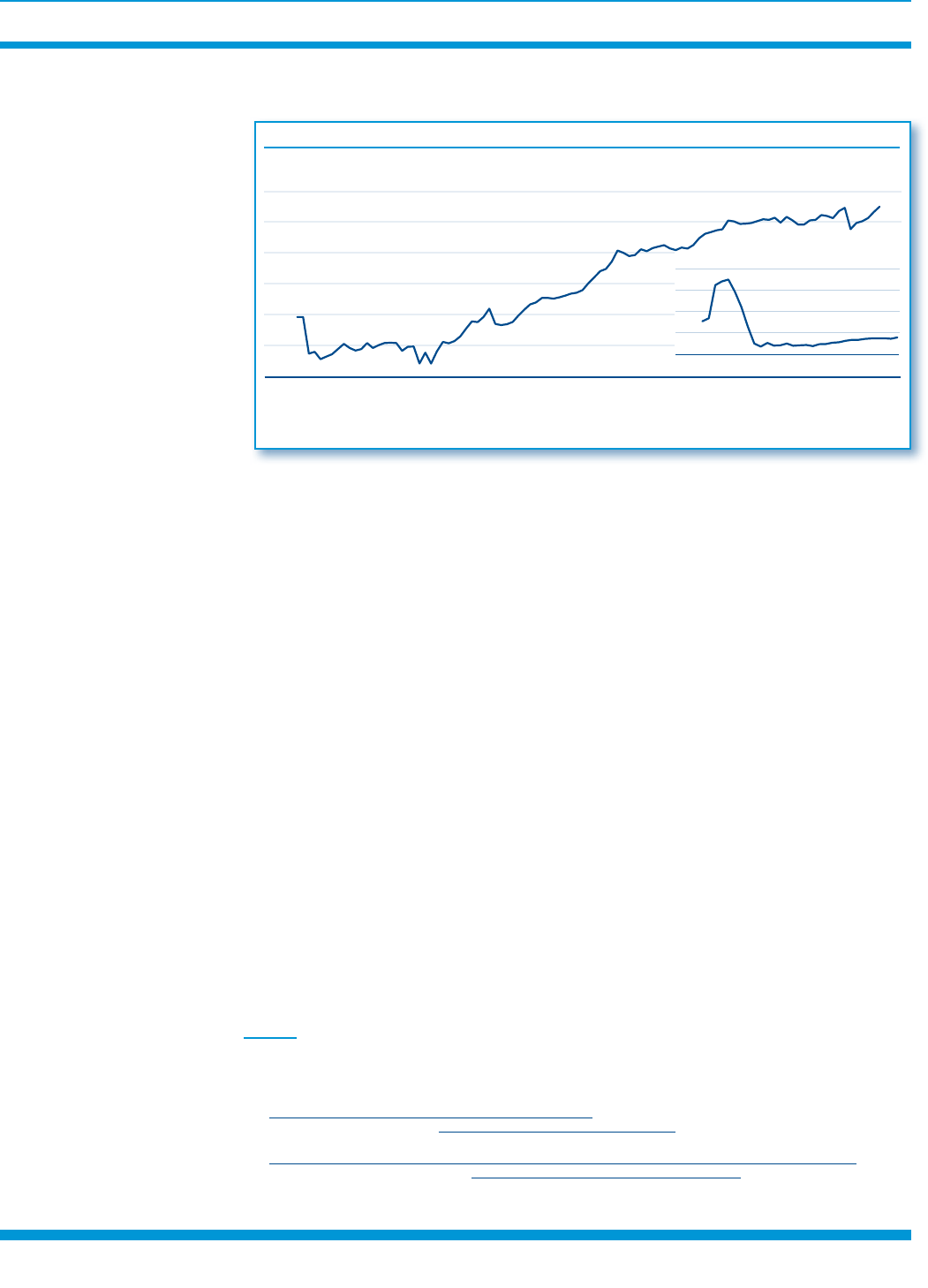

Strong Post-Crisis Growth in Nonbank Mortgage Originations Enabled Nonbanks to

Surpass the Bank Share of Originations Since 2016

Source: FDIC analysis of Home Mortgage Disclosure Act data.

Notes: Nonbanks include all Department of Housing and Urban Development reporters. Banks also include credit unions and their aliates.

Data are limited to single-family residential mortgage originations, dened as rst-lien purchase or renance loans secured by an owner-occupied,

1–4 family unit, site-built property.

Market Share

Percent

Origination Volume

$ Billions

52.5

0

20

40

60

80

100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

Bank Volume (Right Axis) Nonbank Volume (Right Axis)

Bank Share (Le Axis) Nonbank Share (Le Axis)

47.5

Chart 2

Mortgage Origination and

Servicing Trends in Banks

and Nonbanks During the

Pre- and Post-Crisis Period

The period from 2000 to 2008 was characterized by a rapid expansion followed by a sudden

contraction in mortgage origination with large shifts in the participants in and composition

of the mortgage market. In the pre-crisis period, home prices rose rapidly and the volume of

1–4 family mortgage originations grew to nearly $2.3 trillion in 2005, for which nonbanks

originated just more than one-third (Chart 2).

10

Fueled by investor demand, the share of

originations sold into private-label securitizations grew rapidly. Lenders that reached aggres-

sively for growth used less stringent lending practices and underwriting standards, causing

a rapid rise in risk.

11

These lenders increasingly offered loans with limited or no documenta-

tion of the consumer’s income or assets, negative amortization, interest-only payments, and

adjustable rates with low initial monthly payments and subsequent payment reset.

12

Nonbanks and banks, particularly the largest banks and their affiliates, grew their mort-

gage originations at an unprecedented rate through 2005 before home prices peaked and

mortgage delinquencies accelerated. With the onset of the housing crisis, nonbank origina-

tors faced funding strains. Dependence on credit to finance both mortgage origination and

the costs of mortgages in default made nonbanks particularly vulnerable as banks either

cancelled existing lines of credit or became unwilling or less willing to extend new lines. The

slowdown in securitization markets made it difficult for nonbanks to move loan origina-

tions off the warehouse lines and to obtain financing.

13

Nonbanks yielded 12.4percent of

their market share of originations to banks between 2006 and 2007 and nonbank failures

accelerated.

14

10

The pre-crisis period is defined throughout this article as 2000 through the start of the recession in December 2007, though the

onset of the housing crisis preceded the onset of the recession.

11

Urban Institute, “Housing Finance at a Glance,” July 2019:8, https://www.urban.org/sites/default/files/publication/100723/

july_chartbook_2019_1.pdf.

12

Consumer Financial Protection Bureau, “Ability-to-Repay and Qualified Mortgage Rule Assessment Report,” January 2019:9,

https://files.consumerfinance.gov/f/documents/cfpb_ability-to-repay-qualified-mortgage_assessment-report.pdf.

13

You Suk Kim, Richard Stanton, Steven M. Laufer, Nancy Wallace, and Karen Pence, “Liquidity Crises in the Mortgage

Market,” Brookings Papers on Economic Activity, March 8, 2018:348–349, 366, https://www.brookings.edu/wp-content/

uploads/2018/03/5_kimetal.pdf.

14

A number of nonbanks failed in 2007 and did not report HMDA data for 2007. Consequently, the volume of nonbank

originations for 2007 may be understated.

2019 • Volume 1 3 • Number 4

54 FDIC QUARTERLY

Through 2009, as mortgage delinquencies and defaults accelerated and securitization markets

were strained, many banks and nonbanks with mortgage businesses could not offload origi-

nations to third parties and were instead left with large quantities of relatively inferior qual-

ity mortgage loans on their books.

15

During this period, many bank and nonbank lenders

failed, faced bankruptcy, or merged with other lenders. Between 2005 and 2009, the number

of banks reporting HMDA data declined by 3.7percent while the number of nonbank report-

ers declined by 32.6percent. The volume of 1–4 family mortgage originations declined from

$1.6trillion in 2007 to $1.1 trillion in 2008, but rose to $1.6 trillion in 2009.

After the financial crisis, demand has generally outpaced supply in the housing market and

home price appreciation has exceeded income growth. An extended period of low interest

rates boosted refinancing activity, while a decline in the inventory of existing homes for sale

and moderate levels of new home construction restricted supply and increased home prices,

which tempered growth in home sales.

16

After a prolonged period of low interest rates, mort-

gage rates climbed in 2013 and again in 2016, further reducing affordability of purchase

loans and the appeal of refinancing.

17

The resulting decline in refinancing activity served

as a major impediment to the refinancing-focused business models of some lenders. Nearly

40percent of the origination activity of both banks and nonbanks is refinancing, and some

of the largest nonbanks depend particularly on revenue from refinancings.

18

Overall, origi-

nation volume post-crisis has been low compared with pre-crisis.

Nonbank originators and servicers gained significant market share post-crisis. Nonbanks

accounted for 52.5percent of the volume of 1–4 family mortgages originated in 2017, up

significantly from the financial crisis-era low of 23.5percent in 2007 (Chart 2). Nonbank

mortgage servicers also continue to gain significant market share (Chart 3). Among the top

25 servicers in 2018, nonbanks serviced 42.3percent of mortgages, up from 4.0percent in

2008. Overall servicing volume reached $10.9 trillion in 2018, down slightly from the peak of

$11.2 trillion in 2007 but more than double the $5.1 trillion reported in 2000.

19

Nonbanks Continue to Gain Market Share of Mortgage Servicing in the Post-Crisis Period

Source: FDIC analysis of Inside Mortgage Finance data.

Notes: Includes top 25 servicers by volume. Ranking includes entities that own mortgage servicing rights but do not service loans directly and some

institutions that subservice only. Bank and nonbank classications were performed using National Information Center organization hierarchies.

Nonbanks include entities that are not insured depository institutions (IDIs) and that are not aliated with IDIs (not a subsidiary or parent of an IDI

and not a subsidiary or parent of a holding company that is parent to one or more IDI subsidiaries).

Market Share

Percent

Volume of Top 25 Mortgage Servicers

$ Billions

0

20

40

60

80

100

Bank Volume (Right Axis) Nonbank Volume (Right Axis)

Bank Share (Le Axis) Nonbank Share (Le Axis)

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

57.7

42.3

Chart 3

15

Amiyatosh Purnanandam, “Originate-to-Distribute Model and the Subprime Mortgage Crisis,” FDIC, August9, 2010:2,

https://www.fdic.gov/bank/analytical/cfr/2010/wp2010/2010-08.pdf.

16

Joint Center for Housing Studies of Harvard University, “The State of the Nation’s Housing 2018,” Harvard Kennedy

School:3–12, https://www.jchs.harvard.edu/sites/default/files/Harvard_JCHS_State_of_the_Nations_Housing_2018.pdf.

17

Freddie Mac, Primary Mortgage Market Survey, http://www.freddiemac.com/pmms/.

18

According to 2017 HMDA aggregate data, both banks and nonbanks reported nearly 36 percent of origination volume in

refinance. However, the top seven nonbank lenders reported 51 percent of volume in refinance loans. The top two nonbank

lenders specialize in refinance.

19

Inside Mortgage Finance data compiled by the FDIC and servicing rankings are based on total residential mortgages serviced.

The Inside Mortgage Finance ranking includes entities that own mortgage servicing rights, but do not service loans directly, and

some institutions that subservice only. See footnote 7 for details.

FDIC QUARTE RLY

55

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

The Shift in Mortgage

Origination and Servicing

to Nonbanks

In the financial crisis, many nonbanks, especially the largest, experienced significant fund-

ing strains and scaled back origination and servicing or left the business. Nearly all of the

largest nonbank mortgage originators and servicers today were new to the market or quickly

accumulated market share post-crisis, while many banks among the largest mortgage origi-

nators and servicers today also ranked among the largest before the financial crisis.

A sizeable share of the banks most active in mortgage origination and servicing before the

financial crisis remained active in these markets after the crisis. The market share of many

of these banks has diminished marginally, yet not enough for these banks to fall from the

top rankings. Conversely, many of the nonbanks most active in the market today were inac-

tive before and during the financial crisis, or had smaller operations that they built upon

post-crisis.

The strong resurgence of nonbanks in mortgage origination and servicing post-crisis has

largely been attributed to:

• litigation on crisis-era legacy portfolios at the largest bank originators

• more aggressive expansion by nonbanks

• mortgage-focused business models and technological innovation of nonbanks

• large bank sales of crisis-era legacy servicing portfolios because of servicing deficiencies

and difficulties revealed in the financial crisis

• changes to the capital treatment of mortgage servicing assets (MSAs) applicable to banks.

Explanations for the shift in mortgage origination activity to nonbanks. Many of the

largest banks that engaged in mortgage origination pre-crisis and survived the crisis faced

post-crisis litigation for crisis-era legacy portfolios, particularly for Federal Housing Admin-

istration (FHA)-insured originations. This litigation and the associated fines and legal fees

reduced the profitability of these large banks and may have served as deterrents to post-crisis

mortgage origination, particularly of FHA-insured loans. Of particular concern to a mortgage

originator is “put-back risk”—the risk that the originator will be asked to repurchase loans.

20

As indicated by the shifts in the rankings of top originators, post-crisis nonbank mortgage

originators generally did not have the same legacy exposure as these large banks, as many of

these nonbanks were established in the post-crisis period or had limited operations leading

up to the crisis. Nonbanks have increased their market share in origination of loans with

mortgage insurance or other guarantees from federal government agencies (government

loans), and often sell these loans into mortgage-backed securities (MBS) guaranteed by

Ginnie Mae.

21

Many nonbanks expanded operations more aggressively than did banks after the crisis,

partially in response to the thriving refinancing market that resulted from low interest

rates.

22

Some of the largest nonbanks that emerged in this period focused their business

models on refinancing, which is particularly rate-sensitive, though in aggregate both banks

and nonbanks report a similar share of refinance activity.

20

Lux and Greene:17.

21

Government loans include loans with mortgage insurance or other guarantees from federal government agencies, including the

FHA, VA, and the U.S. Department of Agriculture (USDA) Farm Service Agency and Rural Housing Service.

22

“Recent Trends in the Enterprises’ Purchases of Mortgages From Smaller Lenders and Nonbank Mortgage Companies,” Office

of the Inspector General of the Federal Housing Finance Agency (FHFA), July 2014:17, https://www.fhfaoig.gov/Content/Files/

EVL-2014-010_0.pdf.

2019 • Volume 1 3 • Number 4

56 FDIC QUART ERLY

Nonbank mortgage originators have generally focused on mortgage lending, while banks

generally have multiple business lines and can shift resources in response to changes in prof-

itability and in the housing market. Most nonbanks focus on mortgage lending and generally

have fewer business lines. When faced with outsized losses, going out of business is a more

viable option for nonbanks, as demonstrated through the financial crisis.

23

Nonbank specialization in mortgage lending may also place banks at a disadvantage in the

development and application of technology to streamline, automate, and reduce the expense

of the origination process, allowing some nonbanks to reach more aggressively for market

share.

24

Explanations for the shift in mortgage servicing activity to nonbanks. The post-crisis

increase in nonbank market share of servicing has largely been attributed to large bank sales

of crisis-era legacy servicing portfolios and the increase in mortgage origination activity

among nonbanks. Nonbanks boosted their mortgage servicing market share largely through

bulk purchases of the rights to service portfolios of nonperforming loans originally held by

banks. In 2013 alone, nonbank servicers purchased from banks in bulk sales the servicing

rights to more than $500billion in mortgages.

25

The difficulties banks faced managing portfolios of nonperforming loans during the finan-

cial crisis seem to have played a key role in the growth of the post-crisis nonbank servicer

sector. Fines, legal fees, and other heightened expenses associated with litigation and with

the nonperformance of loans in crisis-era servicing portfolios negatively affected profitabil-

ity at some banks and may have deterred growth in servicing portfolios after the crisis.

26

Nonbanks have increased their servicing business, in part because many were not as active

in pre-crisis servicing and did not have large crisis-era legacy portfolios of their own to

deal with. While the cost to service performing and nonperforming loans has significantly

increased post-crisis (Chart 4), nonbanks may have cost advantages over banks in servicing

nonperforming loans, thanks to specialization and the use of technology.

27

These specialty

servicers also received support from Fannie Mae’s High-Touch Servicing Program, which

facilitated the transfer of nonperforming loans from banks to specialty servicers.

28

In 2013, the federal banking agencies issued a revised capital rule for banking institutions

that, among other things, established standards to improve the quality and increase the

quantity of regulatory capital. The revised capital rule tightened the limits on the amount of

MSAs that could be included in regulatory capital and assigned higher-risk weights to MSAs

included in regulatory capital.

29

A 2016 study by the federal banking agencies concluded that

23

Kim et al.:356.

24

Andreas Fuster, Matthew Plosser, Philipp Schnabl, and James Vickery, “The Role of Technology in Mortgage Lending,” Federal

Reserve Bank of New York Staff Report No. 836, February 2018:1, 49, https://www.newyorkfed.org/medialibrary/media/research/

staff_reports/sr836.pdf; Tom Finnegan, “The Large Bank Mortgage Banking Profitability Conundrum,” Stratmor Group, June

2019, https://www.stratmorgroup.com/insights_article/the-large-bank-mortgage-banking-profitability-conundrum/.

25

FDIC, the Federal Reserve Board (FRB), Office of the Comptroller of the Currency (OCC), National Credit Union

Administration (NCUA), “Report to the Congress on the Effect of Capital Rules on Mortgage Servicing Assets,” June 2016:23–25,

https://www.federalreserve.gov/publications/other-reports/files/effect-capital-rules-mortgage-servicing-assets-201606.pdf.

26

FDIC, FRB, OCC, NCUA:23–25.

27

Servicing costs can vary from servicer to servicer depending on the share of delinquent loans in portfolio, the share of these

loans in judicial versus non-judicial foreclosure states, the share of conventional loans versus government loans, and overall

servicer efficiency. Lux and Greene:26.

28

“Evaluation of FHFA’s Oversight of Fannie Mae’s Transfer of Mortgage Servicing Rights From Bank of America to High-Touch

Servicers,” EVL-2012-008, FHFA Office of Inspector General, 2012, https://www.fhfaoig.gov/Content/Files/EVL-2012-008.pdf.

29

While servicing is inherent in all mortgage loans, a mortgage servicing right (MSR) is created only when the act of servicing is

contractually separated from the underlying loan. MSR represents the right to service mortgage loans and receive servicing fees.

It is the present value of the net fee that servicers earn for servicing mortgages and advancing payments to investors. A firm, for

example, that originates a mortgage, sells it to a third party, and retains the servicing would report an MSA on its balance sheet, if

certain conditions are met. That MSA therefore would be subject to a capital requirement. Conversely, a firm would not report an

MSA if the firm originates a mortgage, holds the mortgage on its balance sheet, and performs the servicing.

FDIC QUARTE RLY

57

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

for larger banks, economic incentives to avoid the regulatory capital deduction is likely one

factor influencing the size and distribution of MSAs. The report said that large aggregator

banks reduced their purchases of loans and servicing rights from smaller banks after the

financial crisis, likely in part a result of the revised capital treatment of MSAs.

30

The report

also noted that most small banks either do not have MSAs or have them in small enough

amounts that they would not be subject to capital deductions.

31

Since 2008, the Cost of Servicing a Nonperforming Loan Increased More an Fivefold,

While the Cost of Servicing a Performing Loan Nearly Tripled

Source: Mortgage Bankers Association Servicing Operations Study and Forum.

Notes: 2018 data are through the rst half of the year. Figures include servicing costs associated with single-family residential mortgages.

Nonperforming loans are either delinquent or in default. Performing loans are loans for which the borrower is not behind on payments.

Average Servicing Cost per Loan

Performing Nonperforming

$482

$704

$911

$1,369

$2,304

$2,414

$2,000

$2,386

$2,113

$2,135

$2,471

$59

$77

$90

$96

$114

$156 $156

$181

$163

$158

$160

$0

$500

$1,000

$1,500

$2,000

$2,500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 H1 2018

Chart 4

Characteristics of the

Post-Crisis Generation of

Nonbank Mortgage Lenders

and Servicers

The nonbanks that top the rankings of mortgage originators and servicers post-crisis share

certain similarities with pre-crisis nonbanks, many of which faltered in the crisis. Nonbank

business models can vary significantly. Some nonbanks originate mortgages and retain the

servicing. Others originate mortgages but do not retain the servicing. The nonbanks that

originate mortgages typically obtain funding from warehouse lines of credit extended by

banks. These nonbanks typically apply the originate-to-distribute model, selling originations

into securitizations most often guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae.

Nonbanks are also increasingly funding origination through cash sales to Fannie Mae and

Freddie Mac. Other nonbanks are mortgage servicing rights (MSR) investors that purchase

MSRs and outsource the servicing to another firm, called a subservicer. Some nonbanks are

subservicers and provide servicing functions as third-party vendors.

32

Nonbank and bank risk characteristics differ markedly. Nonbanks rely on external short-

term credit and narrowly focused lines of business in mortgage origination or servicing,

which may pose risks to the banking industry and the financial system. Short-term credit

can become more expensive and less accessible when financial market conditions tighten.

Nonbank originators rely on warehouse lines of credit, which is short-term funding primar-

ily provided by banks.

33

Banks and their affiliates typically fund their mortgage origination

with deposits or other borrowings.

30

FDIC, FRB, OCC, NCUA:29–31.

31

FDIC, FRB, OCC, NCUA:2.

32

“Reengineering Nonbank Supervision,” The Conference of State Bank Supervisors, 2019, https://www.csbs.org/sites/default/

files/chapter_one_-_introduction_to_the_nonbank_industry_cover_footer_1_v2.pdf.

33

Kim et al.:357–358.

2019 • Volume 1 3 • Number 4

58 FDIC QUARTERLY

The federal government now backs a majority of new mortgages either directly at origina-

tion through the FHA, the U.S. Department of Veterans Affairs (VA), or the USDA, or

indirectly in securitization through Ginnie Mae or through the GSEs, including Fannie

Mae and Freddie Mac. Nonbanks now originate a majority of these mortgages.

The composition of 1–4 family mortgage originations shifted significantly in the financial

crisis. Government loans grew from 5.0percent of originations in 2004 to 26.9percent in

2017 (Chart 5). Jumbo loans declined from 29.5percent in 2004 to 17.4percent in 2017.

Conventional, conforming, single-family originations declined from 65.5percent to

55.8percent in the same period, but remain the dominant type of origination.

e Composition of 1–4 Family Mortgage Originations Shied Signicantly rough the Crisis,

as Government Lending Gained Market Share

Source: FDIC analysis of Home Mortgage Disclosure Act data.

Note: Data are limited to single-family residential mortgage originations, dened as rst-lien purchase or renance loans secured by an owner-occupied,

1–4 family unit, site-built property.

Origination Market Share by Loan Type

Percent

0

20

40

60

80

100

Government Loans

Conventional Conforming

Jumbo Loans

26.9

55.8

17.4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Chart 5

Nonbank market share of government lending rose from 44.9percent in 2004 to 76.1percent

in 2017 (Chart 6). Nonbank market share in the largest segment of single-family mortgage

lending—originating new conventional, conforming loans—rose from 34.7percent 2004

to 52.0percent in 2017 (Chart 7). Banks have held their ground in jumbo loans, which have

loan amounts exceeding the size limit for eligibility for purchase by the GSEs. Nonbanks

originated 17.7percent of jumbo loans in 2017, down from 27.3percent in 2004 (Chart 8).

Nonbanks Gained Signicant Market Share of Government Lending

Source: FDIC analysis of Home Mortgage Disclosure Act data.

Notes: Nonbanks include all Department of Housing and Urban Development reporters. Banks include banks, credit unions, and their aliates.

Data are limited to single-family residential mortgage originations, dened as rst-lien purchase or renance loans secured by an owner-occupied,

1–4 family unit, site-built property. Government loans consist of loans with insurance or other guarantees from the Federal Housing Administration,

the U.S. Department of Veterans Aairs, and the U.S. Department of Agriculture.

Market Share of Government Loan Originations

Percent

Government Loan Origination Volume

$ Billions

0

20

40

60

80

100

Bank Volume (Right Axis) Nonbank Volume (Right Axis)

Bank Share (Le Axis) Nonbank Share (Le Axis)

23.9

76.1

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

Chart 6

FDIC QUARTE RLY

59

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

Nonbanks Gained Market Share of Conventional Conforming Originations

Source: FDIC analysis of Home Mortgage Disclosure Act data.

Notes: Nonbanks include all Department of Housing and Urban Development reporters. Banks include banks, credit unions, and their aliates.

Data are limited to single-family residential mortgage originations, dened as rst-lien purchase or renance loans secured by an owner-occupied,

1–4 family unit, site-built property. Conventional conforming loans conform to maximum loan amounts set by the government along with other rules

and limits set by Fannie Mae or Freddie Mac.

Market Share of Conventional

Conforming Originations

Percent

Conventional Conforming

Loan Origination Volume

$ Billions

0

20

40

60

80

100

Bank Volume (Right Axis) Nonbank Volume (Right Axis)

Bank Share (Le Axis) Nonbank Share (Le Axis)

0

200

400

600

800

1,000

1,200

1,400

1,600

48.0

52.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Chart 7

Banks Retained Market Share of Jumbo Loan Originations

Source: FDIC analysis of Home Mortgage Disclosure Act data.

Notes: Nonbanks include all Department of Housing and Urban Development reporters. Banks include banks, credit unions, and their aliates.

Data are limited to single-family residential mortgage originations, dened as rst-lien purchase or renance loans secured by an owner-occupied,

1–4 family unit, site-built property. Jumbo loans have loan amounts in excess of the single-family conforming loan-size limits for eligibility for purchase

by the government-sponsored enterprises.

Market Share of Jumbo Loan Originations

Percent

Jumbo Loan Origination Volume

$ Billions

0

20

40

60

80

100

Bank Volume (Right Axis) Nonbank Volume (Right Axis)

Bank Share (Le Axis) Nonbank Share (Le Axis)

0

200

400

600

800

1,000

1,200

1,400

1,600

82.3

17.7

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Chart 8

Government loans consist of originations with mortgage insurance or other guarantees from

federal government agencies (FHA, VA, and USDA) and are generally eligible to be pooled

into MBS guaranteed by Ginnie Mae. A conventional mortgage is a loan that is not insured

by the FHA, VA, or USDA. A conforming mortgage is one that meets GSE funding criteria

and conforms to maximum loan amounts set by the government and to other rules and

limits set by Fannie Mae or Freddie Mac, and is therefore eligible for purchase and securiti-

zation by either entity. Mortgages that do not conform to the GSE standards, such as jumbo

loans, are called nonconforming loans. Other financial institutions without explicit or

implicit government support, including both banks and nonbanks, also issue MBS, known as

private-label MBS (PLMBS). Nonconforming loans often make up the majority of the pools

underlying PLMBS.

34

34

N. Eric Weiss and Katie Jones, “An Overview of the Housing Finance System in the United States,” Congressional Research

Service, January 2017:5–8, https://fas.org/sgp/crs/misc/R42995.pdf.

2019 • Volume 1 3 • Number 4

60 FDIC QUARTERLY

Nearly all securitization now occurs through entities with government support, like the

GSEs and Ginnie Mae. The private-label market that surged before the financial crisis has

yet to regain much volume. Of all first-lien originations in first quarter 2019, 37.3percent

were portfolio originations (not securitized), 39.6percent were securitized by the GSEs,

20.2percent were sold into securitizations guaranteed by Ginnie Mae, and 2.9percent were

PLMBS (the highest since 2007, yet a small fraction of the private-label share in the years

leading to the crisis).

35

In the post-crisis period, most loans that are securitized through the

GSEs or pooled into securitizations guaranteed by Ginnie Mae are originated by nonbanks.

As of June 2019, nonbanks originated 85percent of all loans sold into securitizations guaran-

teed by Ginnie Mae, 53percent of loans sold to Freddie Mac, and 60percent of loans sold to

Fannie Mae. In 2013, the nonbank share for each was below 40percent.

36

Nonbanks facilitate access to mortgage credit for a broad range of borrowers and have

played a key role in opening up access to credit. As banks, particularly the largest banks,

have largely pulled back from government lending, and to a lesser extent, conventional

conforming lending, nonbanks have stepped up originations in the FHA market, especially

where the borrowers are disproportionately either first-time borrowers or borrowers with

lower credit scores and higher debt-to-income (DTI) ratios.

Banks generally have more conservative mortgage underwriting practices than

nonbanks, as nonbanks gain market share in government and conventional conforming

lending. As of June 2019, the median credit score was roughly 25 points lower on nonbank

loans than bank loans in securitizations guaranteed by Ginnie Mae and 4 points lower

on nonbank loans than bank loans sold to the GSEs. The median loan-to-value (LTV) for

nonbank and bank originations are comparable, while the median DTI for nonbank loans is

higher, indicating that nonbanks are more accommodating in DTIs and with credit scores.

DTIs rose across the board in 2017 given rising interest rates, as borrower payments were

driven up relative to incomes. The reduction in refinance volumes in the rising rate environ-

ment made lenders more competitive for loans to purchase homes and, therefore, apt to work

hard to secure a loan approval for a wide range of borrowers, another factor that contributed

to the rise in DTIs. However, with the decline in interest rates in 2019, DTIs have come down

measurably, more so for banks.

37

The Federal Housing Finance Agency (FHFA) and the GSEs have relaxed several under-

writing standards for conforming loans since late 2014. Fannie Mae began accepting

mortgages with LTV ratios of up to 97percent in 2014 and Freddie Mac followed in 2015.

Fannie Mae raised its DTI limit from 45 to 50percent in 2017 and replaced a requirement

for compensating factors with standards to reduce risk layering.

38

The GSEs also eliminated

first-time homebuyer requirements for certain mortgage programs, removed income and

geographic limitations, allowed non-borrower income to be included in the DTI calcula-

tion, and extended flexibility in evaluating borrowers with student debt.

39

This relaxation in

underwriting standards for conforming loans affects credit risk in mortgage markets. And

more risk layering has been noted, particularly in government loans and for first-time home

purchase mortgages.

40

35

Urban Institute:8.

36

Urban Institute:11.

37

Urban Institute:17–18.

38

Archana Pradhan, “Underwriting Loosening for Conventional Conforming Loans,” CoreLogic Insights Blog, June 4, 2018,

https://www.corelogic.com/blog/2018/06/underwriting-loosening-for-conventional-conforming-loans.aspx.

39

Select standards apply to certain lending programs offered by Fannie Mae and Freddie Mac post-crisis, including Home Possible

Mortgage and HomeOne from Freddie Mac and HomeReady from Fannie Mae.

40

Risk layering refers to loans with some combination of multiple risk characteristics such as low credit scores, high DTIs, and

high LTVs.

FDIC QUARTE RLY

61

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

Some post-crisis nonbanks rely on technological innovation to improve efficiency. Tech-

nology plays an increasingly prominent role in facilitating access to mortgage credit, and

some of the largest nonbank mortgage lenders are at the forefront in applying technology to

streamline and automate the mortgage origination process. Nonbank mortgage servicers are

also more technologically advanced than most bank competitors.

41

Large banks have a significant disadvantage in mortgage origination expenses. Costs for

corporate administration are on average three times higher for large banks than for large

nonbanks because of 1) overhead administrative expenses that generally do not affect

nonbanks and 2) the difficulty large banks reportedly face in providing efficient technology

support for the mortgage origination business. Higher expenses and lower revenues meant

large banks significantly lagged nonbank competitors in profitability on retail residential

mortgages. According to the review by the Stratmore Group (see note 24), large banks lost

$4,803 per retail mortgage loan originated in 2018 compared to large nonbank lenders,

which earned $376 per loan, on average.

42

The technical expertise and innovation of many nonbank servicers is said to have helped

them to be leaders in customer experience and process efficiency. And nonbanks report-

edly have lowered delinquency and default rates by using technology to educate borrowers,

streamline processes, and make loan modification processes efficient and effective.

43

Risks Posed by Post-Crisis

Generation of Nonbank

Originators and Servicers

While post-crisis nonbank originators and servicers have gained market share over banks

in mortgage origination and servicing, competitive pressures have increased a number of

risks. The sections that follow summarize the key risks posed by nonbank originators and

servicers.

The nonbank structure is vulnerable to liquidity and funding risks. The new post-

crisis generation of nonbanks seem vulnerable to liquidity pressures similar to those that

nonbanks were subjected to during the financial crisis. Nonbanks depend on short-term

credit, particularly warehouse lines of credit provided by banks.

44

This funding can become

more expensive and less accessible when financial market conditions tighten, and this tight-

ening alone can cause the nonbank to go out of business. In times of stress, warehouse lend-

ers face strong incentives to cancel lines of credit and seize collateral as quickly as possible.

45

When a nonbank draws on a line of credit to fund a mortgage, the nonbank transfers the

mortgage to the bank warehouse lender to collateralize this draw on the line. The nonbank

then finds investors for the mortgage, typically either the GSEs or Ginnie Mae investors,

though investors in PLMBS made up a large part of the market pre-crisis. Once the mortgage

is sold, the proceeds are paid to the bank, the bank releases the mortgage to the securitiza-

tion vehicle, and the warehouse lender then pays down the dollar value of the draw to the

nonbank’s line of credit.

46

41

Lux and Greene:27–28.

42

Finnegan, June 2019. The review also found that large bank revenue per loan was on average $1,712 lower than at large

nonbanks, reflecting the lack of a robust secondary market and a competitive pricing environment for jumbo loans. The review

noted that the servicing function, which produced modest profits for most of the large banks in 2018, offset origination losses to

some extent. The report was based on a review of more than 100 lenders.

43

Lux and Greene:28, and Fuster et al.:2, 15–16.

44

According to Kim et al., (2018), while banks may allow nonbanks to finance servicing advances as part of the warehouse lines

of credit primarily used for funding loan originations, nonbank mortgage servicers have other options for funding servicing

advances, including securitization, cash from operations, unsecured loans, or credit lines collateralized by other assets, such

as MSRs. Ginnie Mae recently released a “Report on Issuer Liquidity Meeting Series,” https://www.ginniemae.gov/newsroom/

publications/Documents/issuer_liquidity_meeting_series_report.pdf, which indicated that much of the shift in mortgage

origination and servicing activity to the largest nonbanks was financed by private equity or other types of investment funds,

which infused billions of dollars of capital either through direct ownership in the operating companies of nonbanks or the

financing and ownership of mortgage servicing rights. The report also confirms that as the nonbank share of mortgage

origination and servicing has risen, so has the sum of warehouse lines and servicing advance facilities largely provided by banks.

45

Kim et al.:347-350.

46

Kim et al.:361–362.

2019 • Volume 1 3 • Number 4

62 FDIC QUARTERLY

Kim et al. (2018) cite “vulnerabilities associated with the warehouse funding of nonbanks:

(i)margin calls due to aging risk (that is, the time it takes the nonbank to sell the loans

to amortgage investor and repurchase the collateral), (ii) mark-to-market devaluations,

(iii)rollover risk, (iv) cancellation of a line for covenant violations, and (v) changes in ware-

house lender risk appetite.”

47

In addition, the put-back risk for mortgages funded with

warehouse lines remains with the nonbank originator, since the originator underwrote and

funded the loan in its own name.

48

Nonbank mortgage servicers face both liquidity and capital concerns because servicers of

mortgages in securitized pools must make payments to investors, tax authorities, and insur-

ers when mortgage borrowers skip their payments. While many servicers are eventually

reimbursed for most of these advances, they need to finance them in the interim and obtain-

ing such financing can be difficult in times of strain. Servicers can incur large costs servicing

delinquent loans, especially those that end in foreclosure.

49

Nonbank originations are 85percent of all loans sold into securitizations guaranteed

by Ginnie Mae and more than half of all loans sold to the GSEs, so there is a risk that if

nonbanks have liquidity or solvency issues, nonbank servicers may not have cash on hand

to fulfill advances to Ginnie Mae and GSE bondholders, particularly if delinquencies rise.

50

Credit risk and liquidity concerns can be more pronounced for Ginnie Mae servicers, which

may need to advance more types of payments for much longer than GSE servicers when

mortgage borrowers become delinquent, or default. Ginnie Mae-guaranteed pools are not

limited in the time they must advance principal and interest on delinquent loans, and they

may be required to absorb losses not covered by the FHA or VA, including property repair

costs.

51

Chart 9 illustrates Ginnie Mae’s relative loss position as guarantor of the servicing

performance of the issuer. In general, by the time risk is passed on to Ginnie Mae, Ginnie

Mae has no recourse against an issuer.

Credit Loss Priorities for a Defaulted Mortgage in a Pool Guaranteed by Ginnie Mae

Source: Ginnie Mae, 2016.

First Dollar Loss

Last Dollar Loss

LOSSES

Government

Agency Insurance

Corporate

Resources of

Issuer/Servicer

Ginnie Mae

Relative Loss Position

$

Homeowner

Equity

Chart 9

47

Kim et al.:362.

48

David Echeverry, Richard Stanton, and Nancy Wallace, “Funding Fragility in the Residential Mortgage Market,” Berkeley Haas

School of Business, December 31, 2016:7, https://www.aeaweb.org/conference/2017/preliminary/paper/zKz3shzZ.

49

Kim et al.:376.

50

Urban Institute:11.

51

Kim et al.:376.

FDIC QUARTE RLY

63

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

The liquidity issues associated with both nonbank origination and servicing have become

more pressing because the nonbank sector is a larger part of the market than it was before

the financial crisis. And because many nonbanks share similar business models, contagion is

a concern as strains in one nonbank could cause creditors to question the viability of others.

Given the outsized share of nonbank origination and servicing of government mortgages,

including FHA-guaranteed loans to borrowers with higher risk of default, the government

may incur insurance losses on the mortgages and on the securities that fund them. Govern-

ment guarantees are conditional and somewhat limited, and a rise in defaults could expose

nonbanks to insolvency.

52

The refinancing-focused business models of some lenders, including some of the largest

nonbanks, are vulnerable to changes in interest rates. Many lenders, including some of

the largest nonbanks that emerged in the post-crisis period, benefited from the prolonged

period of low interest rates and focused their business models on refinancing mortgages.

53

The demand for refinancing depends highly on interest rates. When rates rise and remain

elevated, refinancing activity and the associated revenue declines.

54

Refinancing activ-

ity slowed with the increases in interest rates that started in 2013 and again in 2016, and

both banks and nonbanks engaged in refinancing have attempted to shift their focus to the

competitive market for purchase loans. Those that struggle to remain competitive may face

acquisition by stronger peers, a trend increasingly prevalent among nonbanks in 2018 and

that some analysts expect to continue in 2019.

55

Access to mortgage credit could be more restricted if nonbanks experience difficulties.

Banks have pulled back on government lending while nonbanks have stepped in to fill this

void. Nonbanks have become the primary providers of credit in the FHA market in particu-

lar, where the borrowers are disproportionately either first-time buyers or borrowers with

lower credit scores and higher DTIs. A large-scale failure or widespread consolidation of

nonbanks could lead to significant contraction in mortgage origination capacity, since it is

unclear to what extent banks would return to the FHA market.

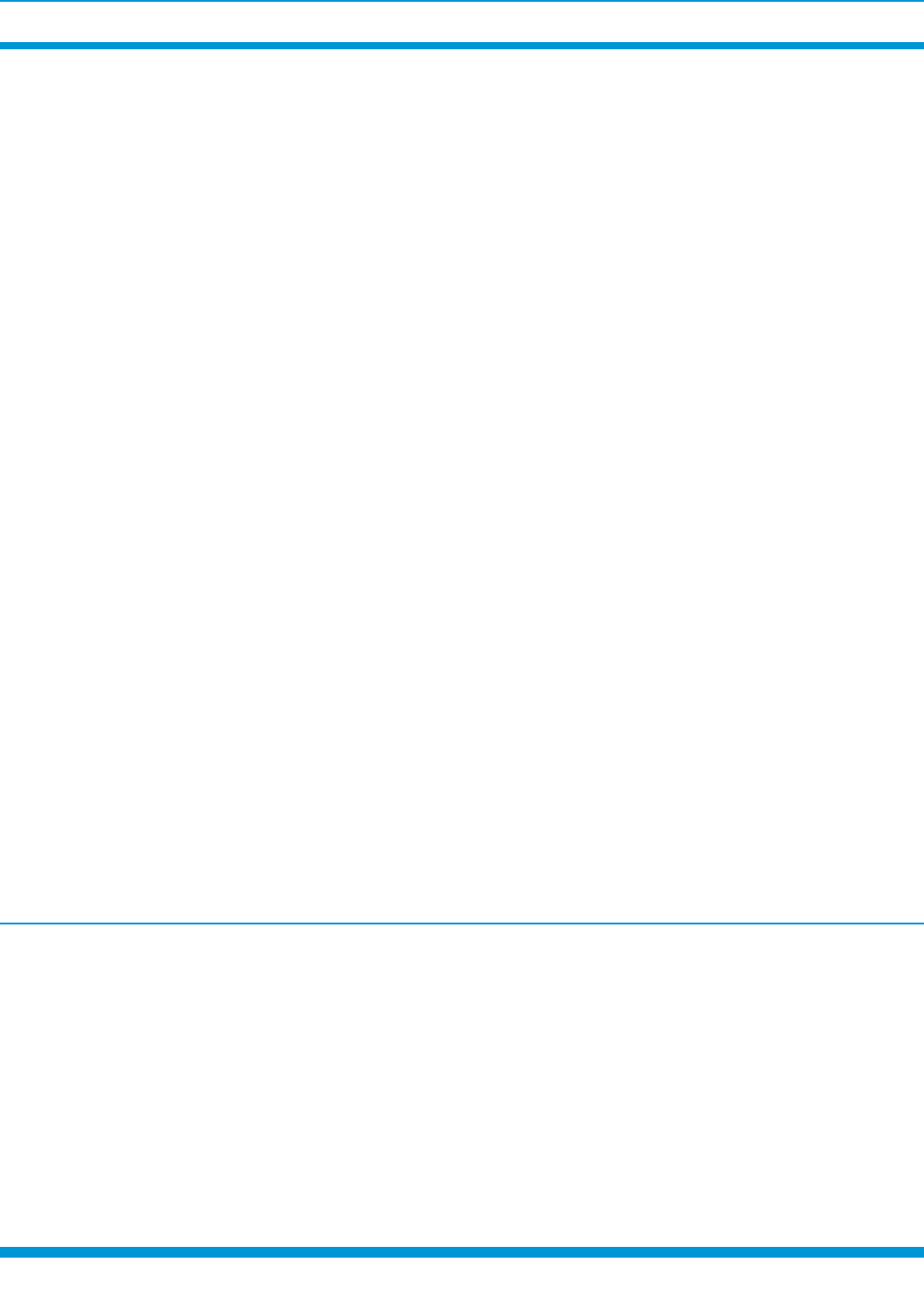

Driven in part by nonbanks, the competitive lending environment is increasing credit

risk. After a prolonged post-crisis period of tightened underwriting standards bolstered by

post-crisis reforms aiming to improve mortgage credit quality and consumer protection, and

the risk-aversion that mortgage lenders exhibited in the aftermath of the crisis, early signs of

marginal deterioration in underwriting standards have emerged. This marginal loosening is

largely in response to heightened competition among bank and nonbank mortgage origina-

tors as they compete for refinancing and purchase loan activity against the headwinds of

higher interest rates, low inventory, and elevated home prices.

GSEs purchase a large share of new originations for securitization, and their recent relax-

ation of requirements for eligibility for purchase put competitive pressures on other entities

that purchase and securitize mortgage loans. Partly in response to relaxed GSE underwrit-

ing standards and to competition, banks and nonbanks are exhibiting incremental easing of

historically tight underwriting standards as they reach for growth in their lending portfolios,

as indicated by continued increases in the Mortgage Credit Availability Index (Chart 10).

Although performance of recent mortgage origination vintages has remained strong, perfor-

mance may worsen if lenders’ appetite for risk continues to increase, especially if macro-

economic conditions deteriorate.

52

Kim et al.:349.

53

According to 2017 HMDA data, in aggregate, both banks and nonbanks reported nearly 36 percent of origination volume in

refinance. However, the top seven nonbank lenders reported 51 percent of volume in refinance loans, driven in part by the two

largest nonbank lenders that specialize in refinance.

54

Kim et al.:387–390.

55

“Mortgage M&As This Year Likely to Top 2018 Tally,” Inside Mortgage Finance, January 3, 2019,

https://www.insidemortgagefinance.com/articles/213439-mortgage-m-as-this-year-likely-to-top-2018-tally?v=preview.”

2019 • Volume 1 3 • Number 4

64 FDIC QUART ERLY

Mortgage Credit Availability Is Trending Higher, Indicating Loosening Credit

Source: Mortgage Bankers Association (Haver Analytics).

Note: Data as of May 2019. e MCAI is calculated using several factors related to borrower eligibility, such as credit score, loan type, and

loan-to-value ratio. ese metrics and underwriting criteria for more than 95 lenders and investors are combined by the Mortgage Bankers Association

(MBA) using data made available via the AllRegMarket Clarityproduct and a proprietary formula derived by MBA to calculate the MCAI.

Mortgage Credit Availability Index (MCAI)

Not seasonally adjusted. March 2012=100

189.5

80

100

120

140

160

180

200

2011 2012 2013 2014 2015 2016 2017 2018 2019

Mortgage Credit Availability Index,

2004–2019

0

250

500

750

1000

2004 2006 2008 2010 2012 2014 2016 2018

Chart 10

Nonbank mortgage lenders predominantly use an originate-to-distribute model, while in

aggregate, banks keep nearly half of their single-family mortgage originations on balance

sheet, according to FDIC analysis of HMDA data.

56

This practice may provide a stronger

incentive for banks to underwrite more carefully and to invest in gathering information

about borrowers and communities.

57

However, competition from nonbanks and slowing of

the housing market could induce banks to ease historically tight underwriting standards.

The Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices

reported incremental easing in underwriting standards for residential real estate lending

from late 2017 through third quarter 2018 and weaker demand for residential mortgages.

58

Technological innovation led by nonbanks has resulted in efficiencies but may increase

business model disruption, heighten risk of consolidation, amplify cybersecurity risks,

and exacerbate operational risks. The competition for mortgage origination and servicing

market share has helped to spur technological innovation beneficial to lenders, servicers,

and consumers. Most nonbanks were new to mortgage origination and servicing and built

their processes and platforms from the ground up using many technological innovations.

Banks with long-established origination and servicing businesses must work to change exist-

ing processes and platforms to incorporate innovation. According to some observers, it is

unclear whether traditional lenders or small institutions can adopt technological advances

that require significant reorganization and investment. A more concentrated mortgage

market dominated by innovative firms may result.

59

While there are benefits to technological innovation, there are also potential risks. While

replacing legacy systems may reduce cyber risks in some areas, cyber risks could be height-

ened in others, highlighting the importance of cybersecurity implementation, technological

literacy, and risk awareness more broadly.

60

56

The share of originations that banks keep their on balance sheets varies greatly by type of origination. Most jumbo loans that

banks originate are kept in portfolio, while a greater share of conforming and government loans are sold into securitizations

guaranteed by the GSEs or Ginnie Mae.

57

Lux and Greene:6.

58

“Senior Loan Officer Opinion Survey on Bank Lending Practices,” Board of Governors of the Federal Reserve System,

January 2017 through January 2019, https://www.federalreserve.gov/data/sloos.htm.

59

Fuster et al.:6, 37.

60

“Financial Stability Implications From FinTech: Supervisory and Regulatory Issues That Merit Authorities’ Attention,”

Financial Stability Board, June 27, 2017:30, http://www.fsb.org/wp-content/uploads/R270617.pdf.

FDIC QUARTE RLY

65

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

Many bank and nonbank originators and servicers increasingly rely on third-party service

providers, many of which are nonbanks and are subject to some federal and state oversight,

yet are generally not federally regulated for safety and soundness. Banks and nonbanks that

rely on third-party service providers are generally subject to operational risk management

policies, including third-party or vendor management guidance. The subservicing sector

allows firms to hold mortgage servicing rights without building and maintaining a servicing

infrastructure. If a subservicer fails, a bank or nonbank relying on that subservicer may have

difficulty finding another subservicer to pick up the portfolio and may not have the capacity

to service the loans itself.

61

In addition, aggressive growth of nonbank mortgage servicers in the post-crisis period may

pose operational challenges, particularly in cases where support infrastructure is insuffi-

cient, and may result in harm to consumers, expose counterparties to operational and repu-

tational risks, and complicate servicing transfers between institutions.

62

Residential mortgage regulation was strengthened post-crisis, and nonbanks are subject

to some federal and state oversight, but, unlike banks, nonbanks are not federally regu-

lated for safety and soundness. A 2019 report from the U.S. Government Accountability

Office (GAO) states that the lack of federal safety and soundness oversight of nonbank lend-

ers and servicers may pose risks, particularly for the GSEs and federal housing finance enti-

ties.

63

The FHFA Office of Inspector General also found in 2014 that nonbank lenders may

have limited financial capacity, are not subject to federal safety and soundness oversight, and

are subject to rapid business growth that could place stress on their operational capacity or

overrun their quality control procedures.

64

Several oversight mechanisms in place or under development help to mitigate these risks.

The Conference of State Bank Supervisors (CSBS) proposed nonbank mortgage servicer

standards covering capital, liquidity, risk management, data standards, data protection

(including cyber risk), corporate governance, servicing transfer requirements, and change of

control.

65

Enhanced standards for more complex nonbanks would focus on capital, liquidity,

stress testing, living wills, and recovery and resolution plans. The CSBS has also undertaken

a comprehensive data collection effort aimed at enhancing a state regulator’s ability to effec-

tively supervise licensees. All state-licensed and state-registered companies must complete the

CSBS Nationwide Multistate Licensing System Mortgage Call Report with information on the

financial condition of licensed mortgage companies, their loan activities, and their mortgage

loan originators.

66

The Consumer Financial Protection Bureau oversees nonbank issuers for

compliance with consumer financial protection laws, and the GSEs apply FHFA standards

in financial and operational reviews of counterparties, including nonbanks. The Consumer

Financial Protection Bureau does not evaluate nonbanks for safety and soundness.

67

However,

safety and soundness evaluations of nonbanks are conducted by state mortgage regulators.

Note: The text on this page has been slightly modified from the version published online on

November14, 2019, to clarify the role of state mortgage regulators with regard to nonbank safety

and soundness examinations.

61

Kim et al.:399.

62

“Nonbank Mortgage Servicers: Existing Regulatory Oversight Could be Strengthened,” U.S. Government Accountability Office,

March 2016:25, https://www.gao.gov/assets/680/675747.pdf.

63

“Prolonged Conservatorships of Fannie Mae and Freddie Mac Prompt Need for Reform,” U.S. Government Accountability

Office, January 2019:27, https://www.gao.gov/products/GAO-19-239.

64

“Recent Trends in the Enterprises’ Purchases of Mortgages from Smaller Lenders and Nonbank Mortgage Companies,” Federal

Housing Finance Agency, Office of Inspector General, July 17, 2014, https://www.fhfaoig.gov/Content/Files/EVL-2014-010_0.pdf.

65

The CSBS represents financial regulators in 50 states, the District of Columbia, Guam, Puerto Rico, American Samoa, and the

U.S. Virgin Islands.

66

“Proposed Regulatory Prudential Standards for Nonbank Mortgage Servicers,” CSBS, 2015, https://www.csbs.org/sites/default/

files/2017-11/MSR-ProposedRegulatoryPrudentialStandardsforNon-BankMortgageServicers.pdf. The Nationwide Multistate

Licensing System registers and collects data from nonbank financial service providers: mortgage providers, money services

businesses, and consumer finance companies.

67

“Prolonged Conservatorships:” 27–28.

2019 • Volume 1 3 • Number 4

66 FDIC QUART ERLY

Implications of the Post-

Crisis Migration for the

Banking Industry and the

Financial System

While a substantive share of mortgage origination and servicing activity has migrated to

nonbanks and transferred some of the risk outside of the banking system, a portion of the

risk remains with banks or could be transmitted back to banks through other channels.

Banks generally have more conservative underwriting practices than do nonbanks, and

while there are indications that banks have been easing standards and increasing risk, a

corresponding deterioration in loan performance has not yet occurred; however, the housing

and mortgage market should continue to be monitored carefully.

Banks retain direct exposure to the mortgage markets through their origination and servic-

ing activities and through the portfolios they keep on their balance sheets, whether they have

scaled back or increased production. From 2004 to 2017, the market share of the top seven

bank originators of 1–4 family mortgages declined 13.6percent, while the market share of all

other banks declined 5.8percent.

The composition of new bank single-family mortgage originations has shifted. In 2004,

63.9percent were conventional conforming, 32.0percent were jumbo loans, and 4.1percent

were government loans. In 2017, 56.4percent were conventional conforming, 30.1percent

were jumbo loans, and 13.5percent were government loans. Banks retain many of the

new jumbo loans originated on their balance sheets, while they sell a larger share of new

conforming and government loans.

In the post-crisis period, banks are directly exposed to nonbanks and the activities in which

they engage through their extension of warehouse lines of credit to nonbank mortgage lend-

ers and other types of financing to nonbank servicers to fund servicing advances. Bank lend-

ing to nonbanks includes loans to nonbank mortgage lenders yet also includes loans to other

nonbanks that do not primarily make loans, including open- and closed-end investment

funds, mutual funds, special purpose vehicles, other vehicles, and real estate investment

trusts.

68

Outside of the loans extended by the four largest banks, supervisory experience

indicates that some loans to nonbank financial institutions are to nonbank mortgage lend-

ers or MBS warehouse lines. Overall, as illustrated in Chart 11, bank lending to nonbanks

has expanded seven-fold since 2010 and exceeds $440billion. While these loans have grown

steadily since 2010, they account for less than 5percent of total loans and leases reported by

banks, and less than 11percent of all banks are engaged in this type of lending.

During Second Quarter 2019, Loans to Nonbanks Held by FDIC-Insured Institutions

Totaled $442 Billion

Source: FDIC.

Note: Quarterly data through second quarter 2019.

Loans to Nonbank Financial Institutions

$ Billions

Share of Banks With Loans to Nonbanks

Percent

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

0

2

4

6

8

10

12

Community Bank Loans to Nonbanks (Le Axis)

Noncommunity Bank Loans to Nonbanks (Le Axis)

Percent Share of Banks With Loans to Nonbanks (Right Axis)

Chart 11

68

Board of Governors of the Federal Reserve System, “Financial Stability Report,” November 2018:29, https://www.federalreserve.

gov/publications/files/financial-stability-report-201811.pdf.

FDIC QUARTE RLY

67

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

Much of the funding that has supported increased nonbank engagement in mortgage origi-

nation and servicing activities is provided by banks through warehouse lines of credit. While

in times of acute strain these lines of credit can be a source of significant losses to banks, as

they were during the financial crisis, they generally are considered relatively low risk because

they are typically overcollateralized and subject to frequent monitoring.

The lines of credit banks extend to nonbanks generally contain multiple protections for

creditors, including personal guarantees, collateral beside the loan originations, and provi-

sions that allow for the changing of the pricing on, or cancellation of, the warehouse line in

the event that the nonbank violates any of its covenants.

69

And banks that extend warehouse

lines are not subject to put-back risk for mortgages funded with these lines, as the put-back

risk remains with the nonbank originator.

70

The lines of credit are generally open for only a limited time and are collateralized by the

loan origination until the nonbank can sell the origination to an investor or into a securi-

tization. When the secondary market is liquid and is functioning normally, nonbanks can

generally sell loans into securitization vehicles relatively quickly and then reimburse the

bank for their draw on the line of credit. However, in the crisis, there were slowdowns in

the securitization of mortgages in both the GSE and PLMBS markets. These slowdowns

contributed to the cancellation ofbillions of dollars in lines of credit to nonbank mortgage

originators, leaving the bank warehouse lender with few options but to seize the mortgage

as collateral.

71

Ultimately, the extension of warehouse lines of credit to nonbank mort-

gage originators and servicers directly exposes banks to the liquidity and funding risks

ofnonbanks.

The extension of credit has important implications for the health of the economy. Unsus-

tainable growth in credit can lead to risk for originators, servicers, and borrowers that face

financial distress. If originators fund loans, particularly loans to borrowers with higher risk

factors and insufficient resources to withstand resulting losses, the financial sector becomes

more vulnerable to adverse shocks. Nonbanks rely primarily on warehouse lines of credit

from banks and other financing firms to fund their operations, a source of funding that

would become more expensive and less accessible in adverse market conditions. To the extent

servicers fund their operations with short-term funding, if adverse market conditions make

that credit less accessible and servicers ultimately yield to liquidity and funding concerns,

borrowers may be at heightened risk of processing errors related to transfer of servicing

rights or other servicing deficiencies, particularly if delinquencies rise.

As nonbanks continue to grow their market share of mortgage origination and servicing, the

associated risk is increasingly shifting from banks to nonbanks and ultimately to the entities

that guarantee payment on securities made up of these loans, namely Ginnie Mae, the GSEs

and, to some extent, other investors.

69

Kim et al.:357–369, 382, 398.

70

Echeverry at al.:7.

71

Kim et al.:357–369, 375, 398.

2019 • Volume 1 3 • Number 4

68 FDIC QUART ERLY

Conclusion A review of the history of the U.S. mortgage market reveals that mortgage originators and

servicers have adapted to changes in the regulatory landscape and evolution in the structure

of the primary and secondary mortgage markets. Over time, competition for mortgage origi-

nation and servicing market share has helped to spur innovation that has enabled market

participants to effectively and efficiently extend credit to borrowers. Risks have been redis-

tributed in the system as a result and have increased in ways described in this article.

After many nonbank mortgage originators and servicers faced liquidity and funding strains

and the threat of failure during the crisis, nonbanks have gained significant market share

since the crisis.

The growth of nonbanks in mortgage origination and servicing after the crisis has largely

been attributed to a handful of factors: litigation on crisis-era legacy portfolios at the largest

bank originators, more aggressive post-crisis expansion by nonbanks, mortgage-focused busi-

ness models and technological innovation at nonbanks, large bank sales of crisis-era legacy

servicing portfolios because of servicing deficiencies and difficulties revealed in the crisis,

and, possibly, large banks’ responses to the capital treatment of mortgage servicing assets.

The characteristics of nonbanks that have, in part, enabled them to gain a competitive edge

in mortgage origination and servicing include continued reliance on short-term credit, a

focus in conventional conforming and government (FHA in particular) loan origination,

origination of loans exhibiting incrementally eased underwriting standards, application of

technological innovation to improve efficiency and origination profits, and less comprehen-

sive regulatory oversight relative to banks.

Many nonbank characteristics subject these entities to several risks, and the new competitive

pressures facilitated by nonbanks have increased several risks in the financial system. These

risks include:

• liquidity and funding risks of the nonbank structure

• interest rate risk inherent in refinancing-focused lending

• risk of reduced availability of FHA-insured and other government loans in the case of

widespread nonbank failures

• moderate growth in credit risk caused by heightened competition in the market driving

incremental easing in historically tight credit standards

• cybersecurity and other risks related to increased reliance on technology

• risks posed by the less stringent and more fragmented regulation of nonbanks relative

tobanks

The funding structure of post-crisis nonbank mortgage originators and servicers appears

similar to that of pre-crisis nonbanks, a generation of lenders and servicers that largely

faltered during the crisis because of funding and liquidity strains. Many of the largest

nonbank originators and servicers today are new to the market or were operating on a

much smaller scale pre-crisis, and have not weathered a crisis or a stressed economy. Given

their similar funding structures, in an episode of pronounced housing-market stress, these

nonbanks could exhibit vulnerabilities similar to those of their predecessors.

FDIC QUARTE RLY

69

TRENDS IN MORTGAGE ORIGINATION AND SERVICING: NONBANKS IN THE POST-CRISIS PERIOD

Nonbanks have so far been well-positioned to compete for growth in the post-crisis mort-

gage market. While the post-crisis recovery in the housing market has been gradual, interest

rates have been low, which boosted the market for both refinance and purchase loans. The

securitization market for those loans has so far been functioning well, despite the collapse

of private-label securitization markets after the crisis. Following several years of more strin-

gent underwriting standards, delinquency rates have been low and nonbank servicers have